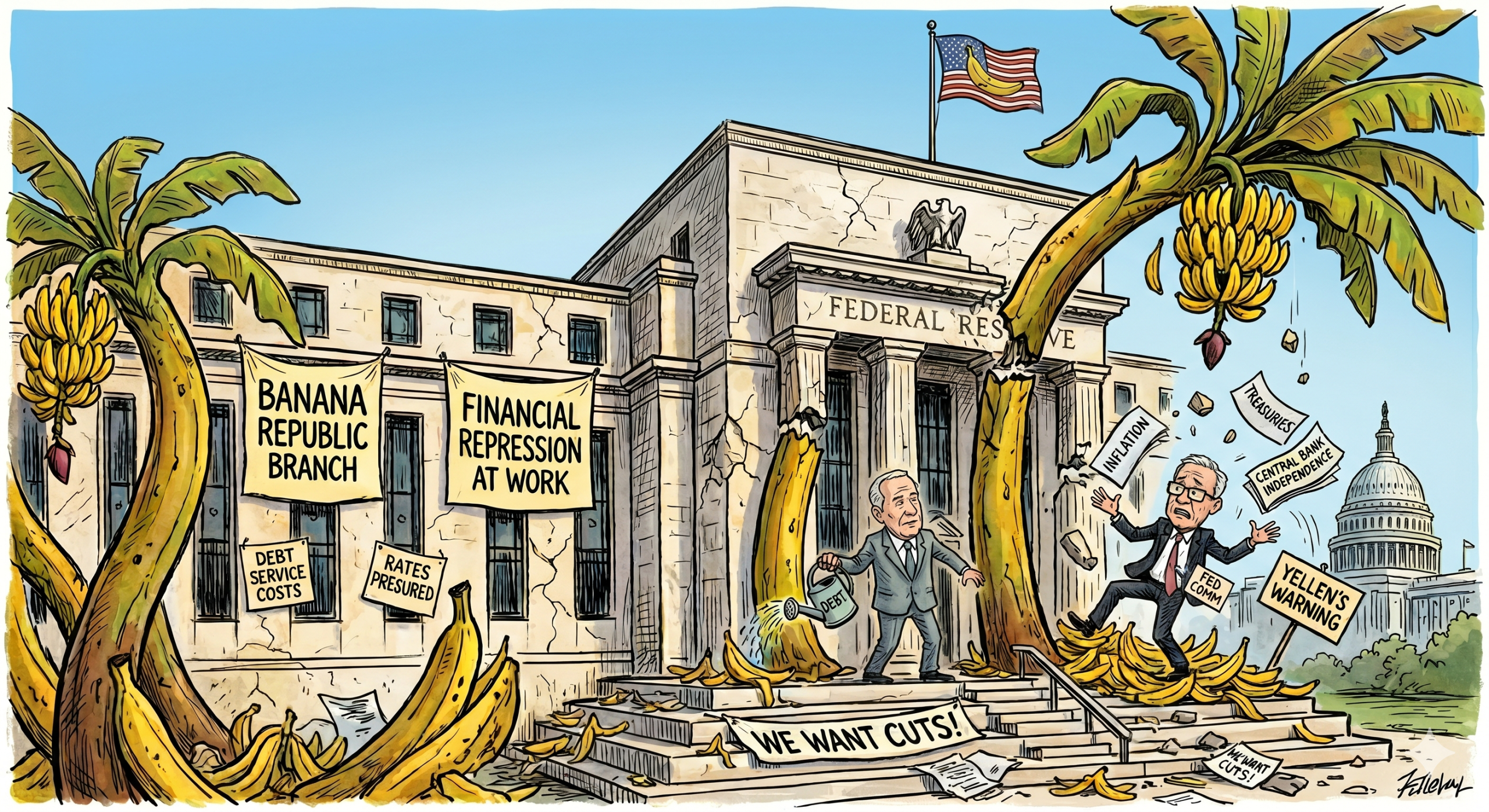

Welcome to the Banana Republic

Welcome to the Banana Republic

Once in a while, a thesis you’ve been quietly writing for years lands on the front page via someone the market cannot ignore. Last week, that was Janet Yellen.

Speaking at the HSBC Global Investment Summit in Hong Kong on April 15, the former U.S. Treasury Secretary, and before that former Fed Chair, was asked about the Trump administration’s campaign to pressure the Federal Reserve into cutting rates to reduce the government’s debt service costs. Her answer was not diplomatic:

“How often does the president of a developed country express the view that the interest rate should be set to reduce the debt service cost?

This is what you hear in a banana republic.”

– Janet Yellen, Hong Kong, 15 April 2026

Source: South China Morning Post

She added that she had “never seen a threat of this level to the Fed before,” and called the White House’s floated threats of criminal charges against Chair Jerome Powell “the ultimate step,” an “unprecedented” way of interfering with central bank independence.

We have been writing about this dynamic since 2018. Not this specific headline, but this specificargument. In our quarterly reports, our special report Gold: The Return of Real Money, and as recently as our April 3 blog The 1974 Illusion, we have argued the same thing: when a government carries a structurally unsustainable debt load, the arithmetic leaves only one viable exit. What is new is that it is now being proposed openly, from the White House, with a straight face.

The Playbook Of An Indebted Government

When a government carries a debt load it cannot grow or tax its way out of, it reaches for the same playbook every time. The playbook has a name, financial repression, and the mechanics are simple:

- Cap nominal rates below inflation. Pressure the central bank, directly or via appointments, to keep policy rates low even as prices rise.

- Let inflation run hot. Don’t fight it. Let it erode the real value of the outstanding debt stock.

- Create captive buyers. Force pension funds, banks, and insurers to hold low-yielding sovereign paper by regulation, tax incentive, or outright mandate.

- Wait. Over a decade or two, the real burden of the debt silently melts. The holders of the bonds, usually savers and retirees, pay the bill through lost purchasing power.

Source: Heyokha Research

Source: Heyokha Research

This is not theoretical. The United States ran this exact playbook from 1946 to 1951 to work off the WWII debt stock. The UK did the same across the post-war decades, Japan has run a variant for thirty years, and every emerging market that has ever been in fiscal trouble has arrived at the same door. There is no clever third option. The arithmetic always wins.

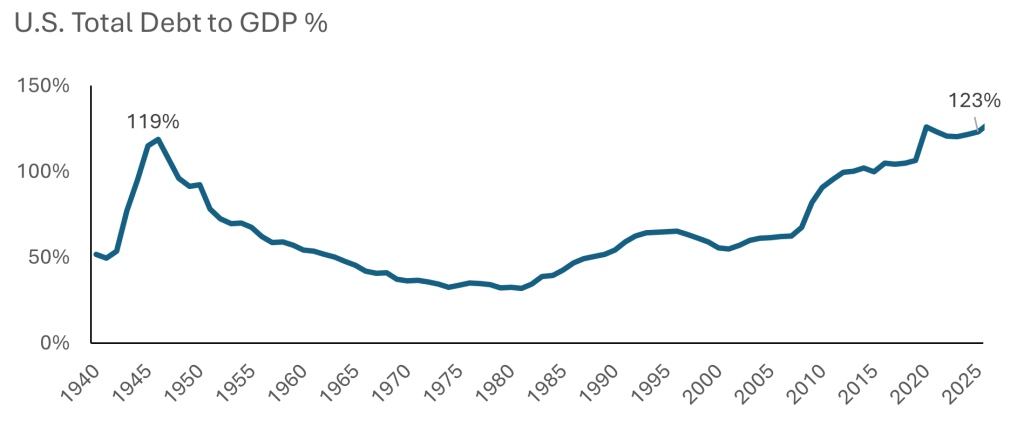

Now it’s higher than WW2!

Now it’s higher than WW2!

Source: Bloomberg

The Arithmetic That Forces It

We laid the numbers out in The 1974 Illusion. They are worth repeating, because the gap between what the math says and what markets are pricing is where the opportunity lives.

- U.S. federal debt: ~$39 trillion. Debt-to-GDP now above 120%, higher than the post-WWII peak that triggered the last formal repression episode.

- Interest expense + mandatory outlays: ~92% of federal tax revenue. That leaves almost nothing left over to run the country, never mind rebuilding infrastructure or funding a great-power rivalry.

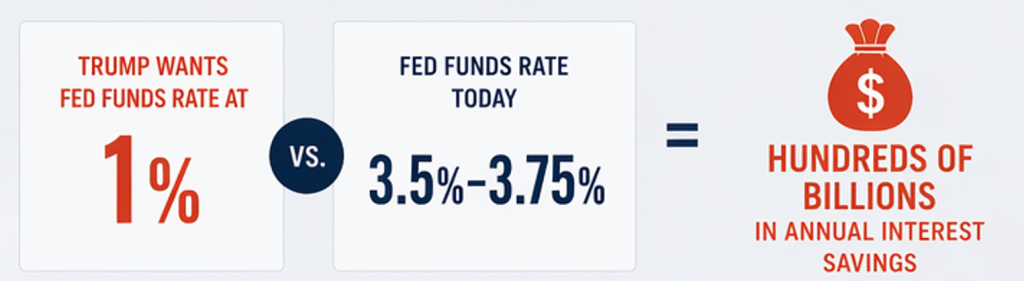

- The gap Trump wants closed: 250 basis points. Fed funds sits at 3.50–3.75%; the White House wants 1%. Not all of it flows through overnight: long rates don’t follow Fed funds one-for-one, and only maturing debt reprices. But about $7–9 trillion of Treasury paper rolls every year, so even a partial pass-through compounds into hundreds of billions over a few cycles. That is the prize.

Paul Volcker could hike to 17% in 1980 because debt-to-GDP was 33% and the sovereign could absorb the medicine. In 2026, with the structural inflation now building on the back of the Iran energy shock, the same medicine kills the patient. The Volcker playbook is dead, and everyone who runs the numbers knows it.

Source: Heyokha Research

Source: Heyokha Research

So the choice is not between hawkish discipline and dovish indulgence. The choice is between an explicit repression regime, run openly, and a quiet one, run by nods and winks. Yellen’s point is that Trump is picking the former. That is what makes it a banana republic: not the arithmetic, but the willingness to stop pretending.

Three Red Lines in Just Two Working Days

If this were only an American story, one could call it a political aberration that corrects when administrations change. It isn’t. In five working days in April, three supposedly-inviolable lines got walked past in public.

- April 15, Hormuz. The U.S. turned back the Rich Starry, a sanctioned tanker attempting to break the American blockade at the entrance to the Strait. Washington is now actively interdicting the flow of energy to China. The mechanism is explicit.

- April 16, London. The House of Commons passed the first leg of a bill letting a government minister mandate the asset allocation of UK pension funds. This is literal financial repression, legislated, at a moment when most of the market is busy looking at equities making new highs.

- April 16, Bloomberg TV. Former U.S. Treasury Secretary Hank Paulson, the man who effectively nationalised much of the American financial system in 2008, admitted on air that there is a “break the glass” plan for the moment the U.S. government cannot sell Treasuries at a yield it can afford. One man saying that in public at that moment is not an accident. That is a former Treasury Secretary pre-positioning the idea in the discourse.

These are not three stories. They are one story: governments reaching, in public, for coercive tools the post-1980 consensus promised would stay on the shelf. Control of commodity flows. Control of where private savings clear. Control of the price a Treasury pays for its own debt. Three levers. One direction of travel. All of it inside two working days.

What To Do When The Playbook Is Public

The uncomfortable truth about financial repression is that it is engineered to punish the people who did exactly what they were told to do: save responsibly in sovereign bonds and hold cash in the local currency. It has to work that way for the arithmetic to resolve. A few things follow:

- Gold is insurance, not speculation. We argued in Gold: The Return of Real Money that a reversion to historical gold-to-monetary-base ratios implies fair value well north of where we are today. Yellen’s quote didn’t change our view. It shortened the distance between our view and the consensus one.

- Own real assets with genuine pricing power. Commodity producers outside the repression geography, food-chain businesses whose margins flex with input costs, and equities with monopolistic or near-monopolistic pricing. Bonds are not shelters in this regime.

- Treat inflation expectations as the variable, not the constant. The entire developed-world pricing complex is currently behaving as if inflation expectations are anchored. Yellen’s warning and the UK pension bill say the same thing: that assumption is on borrowed time.

The Arithmetic Doesn’t Wait

This isn’t a prediction. The playbook is already running, in public, with fingerprints on it. Yellen put a name on it this week. Paulson rehearsed its next move on Bloomberg. Westminster started legislating the machinery on the 16th. The only part still pending is the part where markets stop discounting it.

For our readers, none of this is new. We’ve argued the structure, written about gold as insurance rather than speculation, and laid out the arithmetic in blog after blog. What is new this week is that the argument no longer requires a footnote.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share

Once in a while, a thesis you’ve been quietly writing for years lands on the front page via someone the market cannot ignore. Last week, that was Janet Yellen.

Speaking at the HSBC Global Investment Summit in Hong Kong on April 15, the former U.S. Treasury Secretary, and before that former Fed Chair, was asked about the Trump administration’s campaign to pressure the Federal Reserve into cutting rates to reduce the government’s debt service costs. Her answer was not diplomatic:

“How often does the president of a developed country express the view that the interest rate should be set to reduce the debt service cost?

This is what you hear in a banana republic.”

– Janet Yellen, Hong Kong, 15 April 2026

Source: South China Morning Post

She added that she had “never seen a threat of this level to the Fed before,” and called the White House’s floated threats of criminal charges against Chair Jerome Powell “the ultimate step,” an “unprecedented” way of interfering with central bank independence.

We have been writing about this dynamic since 2018. Not this specific headline, but this specificargument. In our quarterly reports, our special report Gold: The Return of Real Money, and as recently as our April 3 blog The 1974 Illusion, we have argued the same thing: when a government carries a structurally unsustainable debt load, the arithmetic leaves only one viable exit. What is new is that it is now being proposed openly, from the White House, with a straight face.

The Playbook Of An Indebted Government

When a government carries a debt load it cannot grow or tax its way out of, it reaches for the same playbook every time. The playbook has a name, financial repression, and the mechanics are simple:

- Cap nominal rates below inflation. Pressure the central bank, directly or via appointments, to keep policy rates low even as prices rise.

- Let inflation run hot. Don’t fight it. Let it erode the real value of the outstanding debt stock.

- Create captive buyers. Force pension funds, banks, and insurers to hold low-yielding sovereign paper by regulation, tax incentive, or outright mandate.

- Wait. Over a decade or two, the real burden of the debt silently melts. The holders of the bonds, usually savers and retirees, pay the bill through lost purchasing power.

Source: Heyokha Research

This is not theoretical. The United States ran this exact playbook from 1946 to 1951 to work off the WWII debt stock. The UK did the same across the post-war decades, Japan has run a variant for thirty years, and every emerging market that has ever been in fiscal trouble has arrived at the same door. There is no clever third option. The arithmetic always wins.

Now it’s higher than WW2!

Source: Bloomberg

The Arithmetic That Forces It

We laid the numbers out in The 1974 Illusion. They are worth repeating, because the gap between what the math says and what markets are pricing is where the opportunity lives.

- U.S. federal debt: ~$39 trillion. Debt-to-GDP now above 120%, higher than the post-WWII peak that triggered the last formal repression episode.

- Interest expense + mandatory outlays: ~92% of federal tax revenue. That leaves almost nothing left over to run the country, never mind rebuilding infrastructure or funding a great-power rivalry.

- The gap Trump wants closed: 250 basis points. Fed funds sits at 3.50–3.75%; the White House wants 1%. Not all of it flows through overnight: long rates don’t follow Fed funds one-for-one, and only maturing debt reprices. But about $7–9 trillion of Treasury paper rolls every year, so even a partial pass-through compounds into hundreds of billions over a few cycles. That is the prize.

Paul Volcker could hike to 17% in 1980 because debt-to-GDP was 33% and the sovereign could absorb the medicine. In 2026, with the structural inflation now building on the back of the Iran energy shock, the same medicine kills the patient. The Volcker playbook is dead, and everyone who runs the numbers knows it.

Source: Heyokha Research

So the choice is not between hawkish discipline and dovish indulgence. The choice is between an explicit repression regime, run openly, and a quiet one, run by nods and winks. Yellen’s point is that Trump is picking the former. That is what makes it a banana republic: not the arithmetic, but the willingness to stop pretending.

Three Red Lines in Just Two Working Days

If this were only an American story, one could call it a political aberration that corrects when administrations change. It isn’t. In five working days in April, three supposedly-inviolable lines got walked past in public.

- April 15, Hormuz. The U.S. turned back the Rich Starry, a sanctioned tanker attempting to break the American blockade at the entrance to the Strait. Washington is now actively interdicting the flow of energy to China. The mechanism is explicit.

- April 16, London. The House of Commons passed the first leg of a bill letting a government minister mandate the asset allocation of UK pension funds. This is literal financial repression, legislated, at a moment when most of the market is busy looking at equities making new highs.

- April 16, Bloomberg TV. Former U.S. Treasury Secretary Hank Paulson, the man who effectively nationalised much of the American financial system in 2008, admitted on air that there is a “break the glass” plan for the moment the U.S. government cannot sell Treasuries at a yield it can afford. One man saying that in public at that moment is not an accident. That is a former Treasury Secretary pre-positioning the idea in the discourse.

These are not three stories. They are one story: governments reaching, in public, for coercive tools the post-1980 consensus promised would stay on the shelf. Control of commodity flows. Control of where private savings clear. Control of the price a Treasury pays for its own debt. Three levers. One direction of travel. All of it inside two working days.

What To Do When The Playbook Is Public

The uncomfortable truth about financial repression is that it is engineered to punish the people who did exactly what they were told to do: save responsibly in sovereign bonds and hold cash in the local currency. It has to work that way for the arithmetic to resolve. A few things follow:

- Gold is insurance, not speculation. We argued in Gold: The Return of Real Money that a reversion to historical gold-to-monetary-base ratios implies fair value well north of where we are today. Yellen’s quote didn’t change our view. It shortened the distance between our view and the consensus one.

- Own real assets with genuine pricing power. Commodity producers outside the repression geography, food-chain businesses whose margins flex with input costs, and equities with monopolistic or near-monopolistic pricing. Bonds are not shelters in this regime.

- Treat inflation expectations as the variable, not the constant. The entire developed-world pricing complex is currently behaving as if inflation expectations are anchored. Yellen’s warning and the UK pension bill say the same thing: that assumption is on borrowed time.

The Arithmetic Doesn’t Wait

This isn’t a prediction. The playbook is already running, in public, with fingerprints on it. Yellen put a name on it this week. Paulson rehearsed its next move on Bloomberg. Westminster started legislating the machinery on the 16th. The only part still pending is the part where markets stop discounting it.

For our readers, none of this is new. We’ve argued the structure, written about gold as insurance rather than speculation, and laid out the arithmetic in blog after blog. What is new this week is that the argument no longer requires a footnote.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share