Birth Rates Rises When Stock Markets Boom. Coincidence? We Think Not

Birth Rates Rises When Stock Markets Boom. Coincidence? We Think Not

On Karrot, Korea’s neighborhood flea market app, someone recently listed a plain grey SK Hynix work jacket for 40,000 won, about 28 dollars. The selling point was not the fabric. The listing called it “the ultimate blind date outfit.”

![]()

Karrot a second hand clothing app listing (translated to English)

The meme has already earned its own SNL Korea sketch: a luxury store clerk ignores a scruffy customer until she spots the Hynix logo inside his collar, then snaps into a deep bow.

Korean matchmaking agencies now rank chip workers alongside doctors and lawyers.

And the best joke belongs to a netizen: Hynix employees on blind dates apparently say they work at Samsung first, and only reveal the truth once the match proves worthy.

Korean comedy program “Saturday Night Live” parodying a store saleswoman treating a customer way better after finding out he works at SK Hynix

Why a Work Jacket Beats a Tuxedo

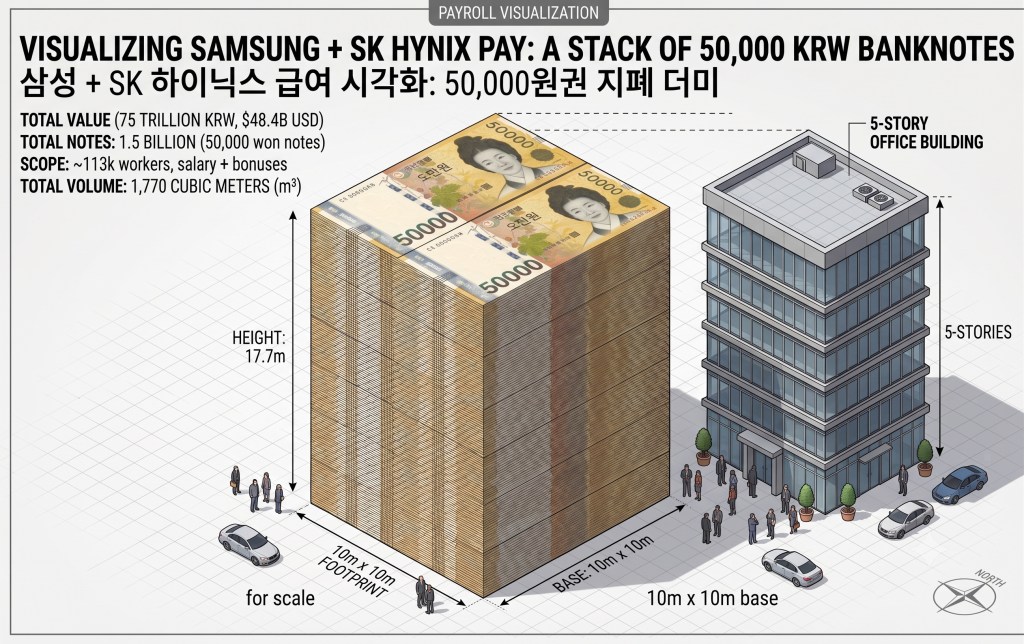

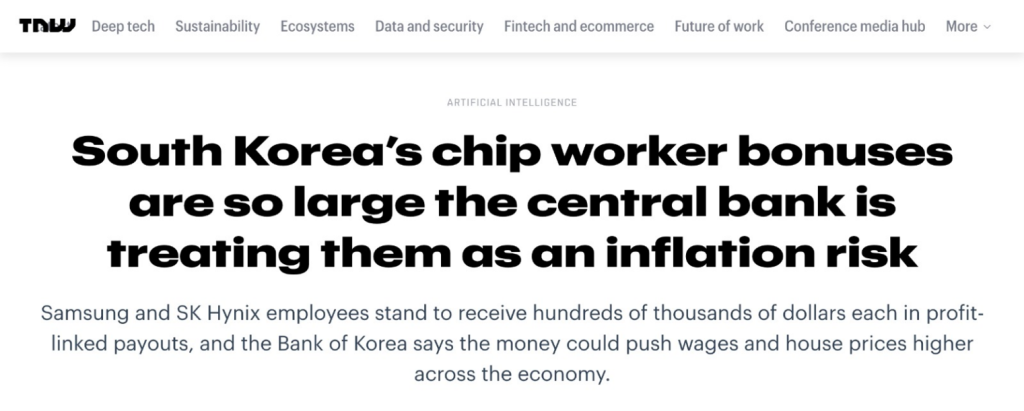

The reason is not subtle. SK Hynix employees are projected to receive bonuses averaging around 454,000 dollars this year. At Samsung, a memory chip worker on a 52,000 dollar base salary stands to collect roughly 410,000 dollars in bonus.

If we total Samsung and SK Hynix pay (salary + bonus), it’s a 5 story building worth of cash!

The AI boom needs high-bandwidth memory, Korea makes most of it, and the unions negotiated a fixed slice of operating profit right before that profit went vertical. The receipt for what we wrote in our blog “AI Arms Race” has arrived, and it is being spent: luxury jewelry sales near the fabs are up 146% year on year, watches up 85%.

The Bank of Korea is so alarmed it did something we cannot recall any central bank doing before: it flagged the paychecks of two companies as a national inflation risk. Somewhere in Seoul, a very serious institution is effectively hiking rates against romance.

source: The Next Web

The Statistic Nobody Puts in the Same Headline

Here is the part that deserves a slow clap. Korea’s birthrate, the most famously doomed number in all of economics, just rose for the second year running.

source: The Guardian

Demographers credit the echo boomers, the 3.6 million Koreans born in the early 1990s who are now reaching parenthood. Fair enough. But squint at the full picture: a generation hitting family age at the exact moment the economy starts paying young engineers like founders and handing the rest of the country a doubling stock market. Blind dates are booking out, department stores are heaving, and the babies are arriving.

Korea has spent two decades and hundreds of trillions of won trying to engineer this outcome. Subsidies, campaigns, committees, slogans. The results were famously nothing.

Then the chip cycle handed young workers actual money, and suddenly the marriage market is the hottest market in the country. Surprise, surprise: people never needed to be persuaded to build families. They needed to be able to afford them.

And the affording is not only about bonus checks. The deeper shift is that a generation that felt locked out of wealth suddenly has a stake in it, whether through a payslip or a portfolio.

Prosperity Goes Public

Here is why this is bigger than 113,000 lucky employees. A wealth effect from corporate profits is nothing new; what makes Korea’s moment different is that the prosperity is being felt far beyond the fab gates, because it found a transmission mechanism: the stock market.

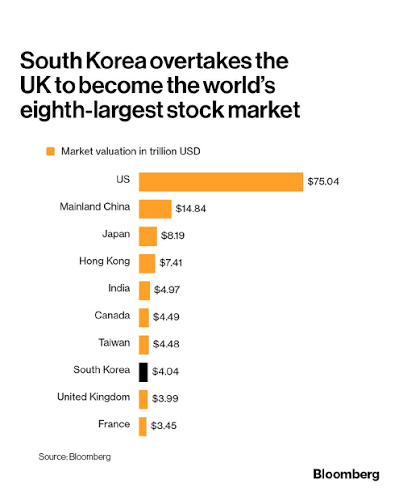

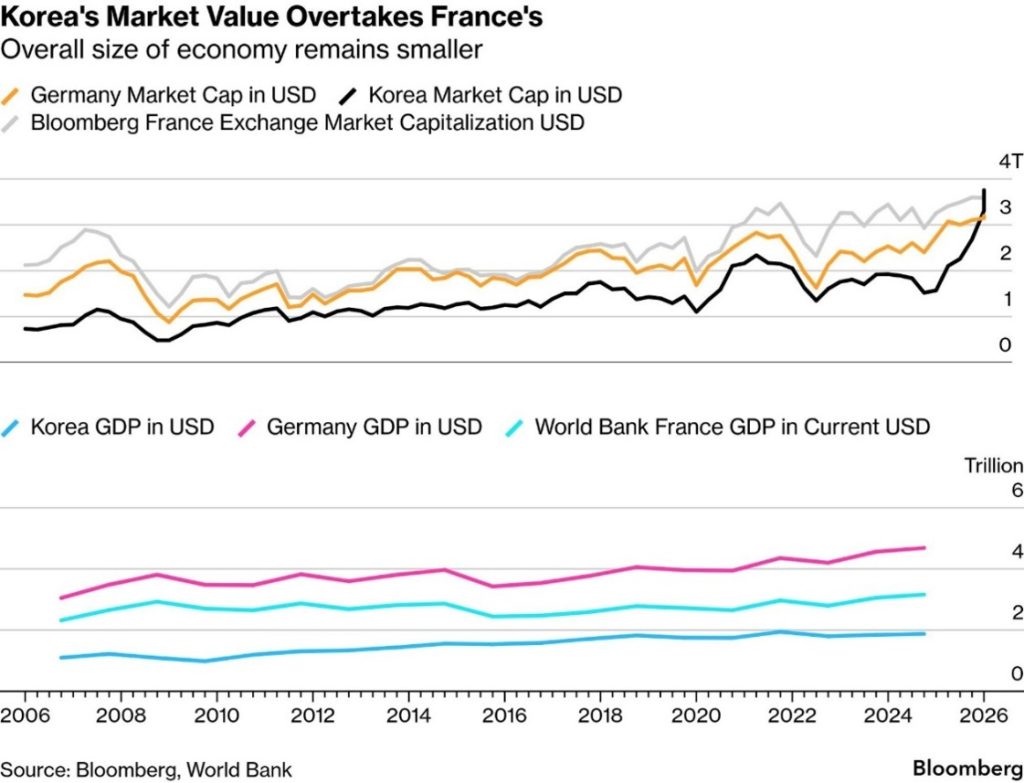

The KOSPI doubled in the first half of 2026, up 101% and closing at record highs above 7,300, with Samsung up 149% and SK Hynix up 215%. Along the way, Korea’s market did something nobody had on their bingo card: at $4.04 trillion in market value it overtook the United Kingdom ($3.99 trillion) to become the world’s eighth largest stock market, having already left France behind.

Read that against the GDP tables and it gets better: Korea’s economy is roughly a third the size of Germany’s, yet its stock market now trades in the same league.

How the tables have turned

source: Bloomberg

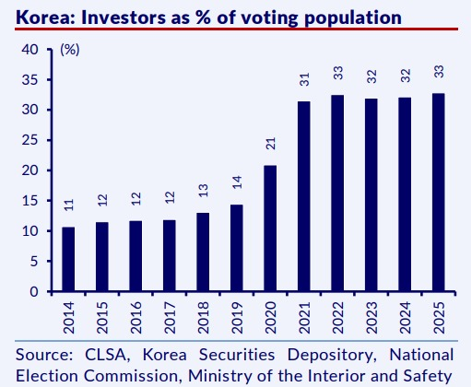

And here is the detail that makes it a prosperity story rather than a hot-money story: foreigners were not the buyers. Foreign funds sold a record $107 billion of Korean shares in the first half, taking profits.

The bid came from home. Korean retail investors poured in roughly $71 billion, and one in three Korean voters now owns stocks, up from one in nine a decade ago.

Zoom in and the numbers get even more striking:

- Korea now counts roughly 14 million retail investors, about 27% of its 51.6 million people

- Narrow it to working-age adults and 44% actively invest in stocks, funds, or ETFs

- One of the highest participation rates in the world and well over twice the roughly 17% seen in the United States or the United Kingdom.

When this market doubles, nearly half the adult population feels it directly.

That is not a niche hobby anymore. That is a constituency, which is why politicians of every stripe suddenly compete on shareholder-friendly reforms. Koreans are buying Korea, and Korea is legislating for Koreans who buy Korea.

More skin in the game now. Retail investors also make up more than half of Korea’s market turnover

source: CLSA

That is the part worth underlining. A bonus enriches an employee. A doubling stock market enriches everyone holding a pension, a retirement account, or a teenage trading-app habit.

The rally has added well over a quadrillion won of market value, a number so large Korean media had to dust off a unit nobody normally uses. This is how a windfall in one industry becomes prosperity an entire country can feel.

Run the comparison honestly and the market wins on almost every axis.

The bonuses, however spectacular, land on about 113,000 badge holders at two companies. The rally lands on everyone: 14 million direct retail accounts, every pension fund, every savings product with equity exposure.

One honest caveat for the economists in the room: per won, bonus cash is probably more spendable. A bonus hits the checking account and feels like income, while stock gains sit unrealized, guarded by loss aversion.

So the consumption punch per won may still favor the paycheck. But the perceived wealth effect, the thing that changes how an entire country feels about its future, belongs overwhelmingly to the market.

A Prescription for the Patient Across the Sea

Which brings us to China, fighting the opposite disease: deflation, price wars, and involution, its own companies competing each other to death while consumers wait for tomorrow’s discount.

Beijing’s prescription so far has been administrative. Anti-involution campaigns, capacity cuts, stern words.

But let us be honest about the mechanism, because the naive reading of Korea would be that the answer is bonus checks. It is not.

You cannot pay 1.4 billion people like memory engineers, and even Korea’s own bonanza directly touches only 113,000 badge holders.

The bonus checks were the spark. The engine is the stock market.

What actually changed the national mood is that one industry’s windfall got amplified through a market that nearly half the adult population owns, so the prosperity arrived in millions of brokerage accounts that never saw a chip bonus.

If you think about it, this is the playbook the United States has run for decades: let the index grind higher, let households feel wealthier, and watch the confidence show up in spending long before any paycheck moves. Korea just joined that club in a single year.

When China Takes the Medicine

We like to think of economies as impossibly complex machines, and mostly they are. But underneath the models sits a very short circuit: people who feel rich spend, marry, and multiply. Korea flipped the switch by accident, and every dial moved at once, from jewelry counters to maternity wards.

Now consider who else is watching this experiment. Beijing has spent years trying to cure deflation with capacity cuts and stern memos, treating the symptom while households stay cautious.

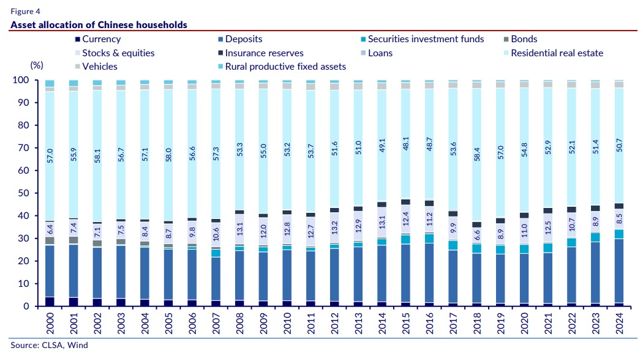

Here is China’s complication: its old prosperity machine is broken. For a generation, Chinese households stored their optimism in apartments. Housing still makes up roughly half of household assets, with only 11% in equities, and after five years of falling prices the property engine now runs in reverse.

Every yuan parked in real estate has been quietly shrinking, which is exactly why consumers hoard cash and wait for tomorrow’s discount. Handing people money is only half the cure. They also need somewhere for that money to grow.

Imagine the impact when the switch up to stocks happens

source: CLSA

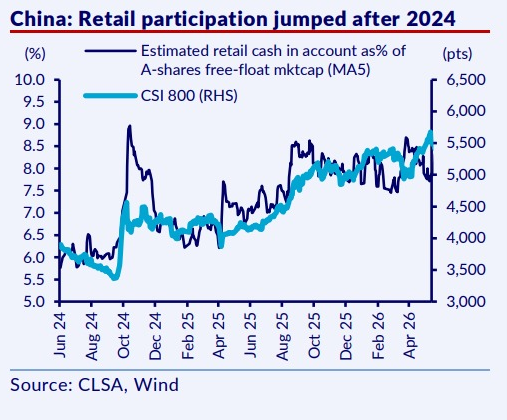

Beijing appears to have noticed, and picked its next instrument: the stock market.

Policymakers are openly steering household savings out of deposits and property and into equities, and the early data says it is catching: retail participation in A-shares has been climbing steadily since late 2024, household cash moving into the market in step with the index itself.

The arithmetic leaves plenty of room to run, with Goldman estimating more than 14 trillion yuan of new household money looking for a home every single year. Korea found its prosperity in a paycheck, and the stock market multiplied it.

China may be attempting the reverse: start with the stock market, and hope the confidence follows.

Which leaves the question we will be watching for the rest of this decade: if a doubling index can change the mood of 51 million people in Korea, imagine what it can do to the mood of 1.4 billion in China?

Tara Mulia and Nicholas

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share

On Karrot, Korea’s neighborhood flea market app, someone recently listed a plain grey SK Hynix work jacket for 40,000 won, about 28 dollars. The selling point was not the fabric. The listing called it “the ultimate blind date outfit.”

![]()

Karrot a second hand clothing app listing (translated to English)

The meme has already earned its own SNL Korea sketch: a luxury store clerk ignores a scruffy customer until she spots the Hynix logo inside his collar, then snaps into a deep bow.

Korean matchmaking agencies now rank chip workers alongside doctors and lawyers.

And the best joke belongs to a netizen: Hynix employees on blind dates apparently say they work at Samsung first, and only reveal the truth once the match proves worthy.

Korean comedy program “Saturday Night Live” parodying a store saleswoman treating a customer way better after finding out he works at SK Hynix

Why a Work Jacket Beats a Tuxedo

The reason is not subtle. SK Hynix employees are projected to receive bonuses averaging around 454,000 dollars this year. At Samsung, a memory chip worker on a 52,000 dollar base salary stands to collect roughly 410,000 dollars in bonus.

If we total Samsung and SK Hynix pay (salary + bonus), it’s a 5 story building worth of cash!

The AI boom needs high-bandwidth memory, Korea makes most of it, and the unions negotiated a fixed slice of operating profit right before that profit went vertical. The receipt for what we wrote in our blog “AI Arms Race” has arrived, and it is being spent: luxury jewelry sales near the fabs are up 146% year on year, watches up 85%.

The Bank of Korea is so alarmed it did something we cannot recall any central bank doing before: it flagged the paychecks of two companies as a national inflation risk. Somewhere in Seoul, a very serious institution is effectively hiking rates against romance.

source: The Next Web

The Statistic Nobody Puts in the Same Headline

Here is the part that deserves a slow clap. Korea’s birthrate, the most famously doomed number in all of economics, just rose for the second year running.

source: The Guardian

Demographers credit the echo boomers, the 3.6 million Koreans born in the early 1990s who are now reaching parenthood. Fair enough. But squint at the full picture: a generation hitting family age at the exact moment the economy starts paying young engineers like founders and handing the rest of the country a doubling stock market. Blind dates are booking out, department stores are heaving, and the babies are arriving.

Korea has spent two decades and hundreds of trillions of won trying to engineer this outcome. Subsidies, campaigns, committees, slogans. The results were famously nothing.

Then the chip cycle handed young workers actual money, and suddenly the marriage market is the hottest market in the country. Surprise, surprise: people never needed to be persuaded to build families. They needed to be able to afford them.

And the affording is not only about bonus checks. The deeper shift is that a generation that felt locked out of wealth suddenly has a stake in it, whether through a payslip or a portfolio.

Prosperity Goes Public

Here is why this is bigger than 113,000 lucky employees. A wealth effect from corporate profits is nothing new; what makes Korea’s moment different is that the prosperity is being felt far beyond the fab gates, because it found a transmission mechanism: the stock market.

The KOSPI doubled in the first half of 2026, up 101% and closing at record highs above 7,300, with Samsung up 149% and SK Hynix up 215%. Along the way, Korea’s market did something nobody had on their bingo card: at $4.04 trillion in market value it overtook the United Kingdom ($3.99 trillion) to become the world’s eighth largest stock market, having already left France behind.

Read that against the GDP tables and it gets better: Korea’s economy is roughly a third the size of Germany’s, yet its stock market now trades in the same league.

How the tables have turned

source: Bloomberg

And here is the detail that makes it a prosperity story rather than a hot-money story: foreigners were not the buyers. Foreign funds sold a record $107 billion of Korean shares in the first half, taking profits.

The bid came from home. Korean retail investors poured in roughly $71 billion, and one in three Korean voters now owns stocks, up from one in nine a decade ago.

Zoom in and the numbers get even more striking:

- Korea now counts roughly 14 million retail investors, about 27% of its 51.6 million people

- Narrow it to working-age adults and 44% actively invest in stocks, funds, or ETFs

- One of the highest participation rates in the world and well over twice the roughly 17% seen in the United States or the United Kingdom.

When this market doubles, nearly half the adult population feels it directly.

That is not a niche hobby anymore. That is a constituency, which is why politicians of every stripe suddenly compete on shareholder-friendly reforms. Koreans are buying Korea, and Korea is legislating for Koreans who buy Korea.

More skin in the game now. Retail investors also make up more than half of Korea’s market turnover

source: CLSA

That is the part worth underlining. A bonus enriches an employee. A doubling stock market enriches everyone holding a pension, a retirement account, or a teenage trading-app habit.

The rally has added well over a quadrillion won of market value, a number so large Korean media had to dust off a unit nobody normally uses. This is how a windfall in one industry becomes prosperity an entire country can feel.

Run the comparison honestly and the market wins on almost every axis.

The bonuses, however spectacular, land on about 113,000 badge holders at two companies. The rally lands on everyone: 14 million direct retail accounts, every pension fund, every savings product with equity exposure.

One honest caveat for the economists in the room: per won, bonus cash is probably more spendable. A bonus hits the checking account and feels like income, while stock gains sit unrealized, guarded by loss aversion.

So the consumption punch per won may still favor the paycheck. But the perceived wealth effect, the thing that changes how an entire country feels about its future, belongs overwhelmingly to the market.

A Prescription for the Patient Across the Sea

Which brings us to China, fighting the opposite disease: deflation, price wars, and involution, its own companies competing each other to death while consumers wait for tomorrow’s discount.

Beijing’s prescription so far has been administrative. Anti-involution campaigns, capacity cuts, stern words.

But let us be honest about the mechanism, because the naive reading of Korea would be that the answer is bonus checks. It is not.

You cannot pay 1.4 billion people like memory engineers, and even Korea’s own bonanza directly touches only 113,000 badge holders.

The bonus checks were the spark. The engine is the stock market.

What actually changed the national mood is that one industry’s windfall got amplified through a market that nearly half the adult population owns, so the prosperity arrived in millions of brokerage accounts that never saw a chip bonus.

If you think about it, this is the playbook the United States has run for decades: let the index grind higher, let households feel wealthier, and watch the confidence show up in spending long before any paycheck moves. Korea just joined that club in a single year.

When China Takes the Medicine

We like to think of economies as impossibly complex machines, and mostly they are. But underneath the models sits a very short circuit: people who feel rich spend, marry, and multiply. Korea flipped the switch by accident, and every dial moved at once, from jewelry counters to maternity wards.

Now consider who else is watching this experiment. Beijing has spent years trying to cure deflation with capacity cuts and stern memos, treating the symptom while households stay cautious.

Here is China’s complication: its old prosperity machine is broken. For a generation, Chinese households stored their optimism in apartments. Housing still makes up roughly half of household assets, with only 11% in equities, and after five years of falling prices the property engine now runs in reverse.

Every yuan parked in real estate has been quietly shrinking, which is exactly why consumers hoard cash and wait for tomorrow’s discount. Handing people money is only half the cure. They also need somewhere for that money to grow.

Imagine the impact when the switch up to stocks happens

source: CLSA

Beijing appears to have noticed, and picked its next instrument: the stock market.

Policymakers are openly steering household savings out of deposits and property and into equities, and the early data says it is catching: retail participation in A-shares has been climbing steadily since late 2024, household cash moving into the market in step with the index itself.

The arithmetic leaves plenty of room to run, with Goldman estimating more than 14 trillion yuan of new household money looking for a home every single year. Korea found its prosperity in a paycheck, and the stock market multiplied it.

China may be attempting the reverse: start with the stock market, and hope the confidence follows.

Which leaves the question we will be watching for the rest of this decade: if a doubling index can change the mood of 51 million people in Korea, imagine what it can do to the mood of 1.4 billion in China?

Tara Mulia and Nicholas

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share