AI Agents Don’t Need Dashboards: The Trillion-Dollar Repricing of Software Debt

AI Agents Don’t Need Dashboards: The Trillion-Dollar Repricing of Software Debt

In November 2025, we warned you about the invisible engine funding the artificial intelligence boom in our piece, When AI Meets Private Credit: The Vessel, Not the Flaw. We noted that an opaque constellation of non-bank lenders was quietly fronting massive chunks of the $6.7 trillion needed for global AI infrastructure.

Six months prior, in AI Just Ate Your CRM. Now What?, we mapped out the existential threat facing traditional software, arguing that AI models would soon bypass clunky user dashboards entirely.

Today, those two distinct tectonic plates—shadow finance and AI software disruption are violently colliding. And the tremors are starting to crack the foundation of Wall Street.

Is This The Canary in the Coal Mine?

The shaking started a few weeks ago with Blue Owl Capital.

Blue Owl is a titan in the private credit space, managing nearly $300 billion in investor cash. But recently, their stock plunged as much as 10% in a single day. Why? They abruptly changed the rules on how investors can pull their money out of a major fund, shifting from a guaranteed 5% quarterly redemption to a discretionary payout model.

For perspective, Blue Owl is the second largest behind Blackstone on controlling almost half of BDC assets

Source: Financial Times, Pitchbook

Wall Street veterans immediately flashed back to August 2007. When a massive shadow lender suddenly throws up the gates to stop cash from leaving, it begs the ultimate question: What are they afraid of?

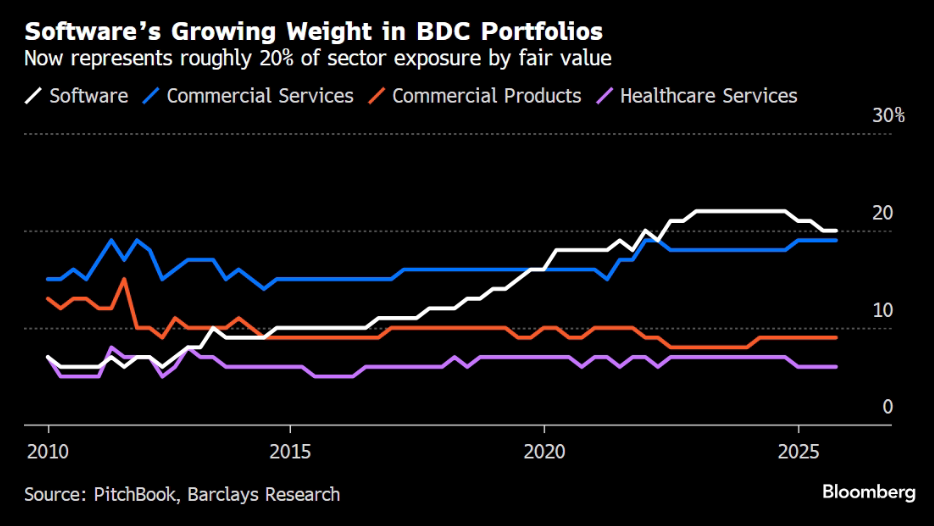

The answer lies in their loan books. In recent years, private credit has extended trillions of dollars in loans to businesses. And their absolute favorite borrower? Software companies.

By industry estimates, at least 20% of all loans extended by private credit funds—and heavily concentrated within Business Development Companies (BDCs)—have gone to software firms. But the true number is likely much higher. A recent Bloomberg analysis found at least 250 investments, worth over $9 billion, that were quietly categorized by lenders as “business services” or “specialty retail” instead of software.

Source: Bloomberg, Barclays, Bloomberg

Private credit lenders loved software for one reason: predictable, recurring revenue. A company with 5,000 employees pays for 5,000 software “seats” every single month. That steady cash flow made it incredibly easy to underwrite massive loans.

But what happens to those loans when AI obliterates the “per-seat” business model?

The “SaaSpocalypse” and the Agentic Future

Let’s add some nuance to the “AI eats software” narrative.

People are panicked that AI will simply delete software companies from existence. That is not entirely true. Software isn’t dying; it is going headless.

To understand this, we need to look at the shift from basic AI Chatbots to AI Agents. A chatbot answers your questions. An AI Agent actually executes multi-step tasks for you across the internet. But an AI Agent does not have eyes. It doesn’t care about pretty dashboards, drop-down menus, or human-friendly interfaces.

It talks to software through an API (Application Programming Interface).

Think of an API as a “Digital Drive-Thru.” If you want food, you don’t have to park, walk inside the restaurant, read the menu, and sit at a table (the old software UI). Instead, you pull your car up to the drive-thru window, hand them a specific, structured order, and they hand you the food. An API allows an AI Agent to pull up to a software company, hand it code, and get the data back instantly without ever “looking” at the website.

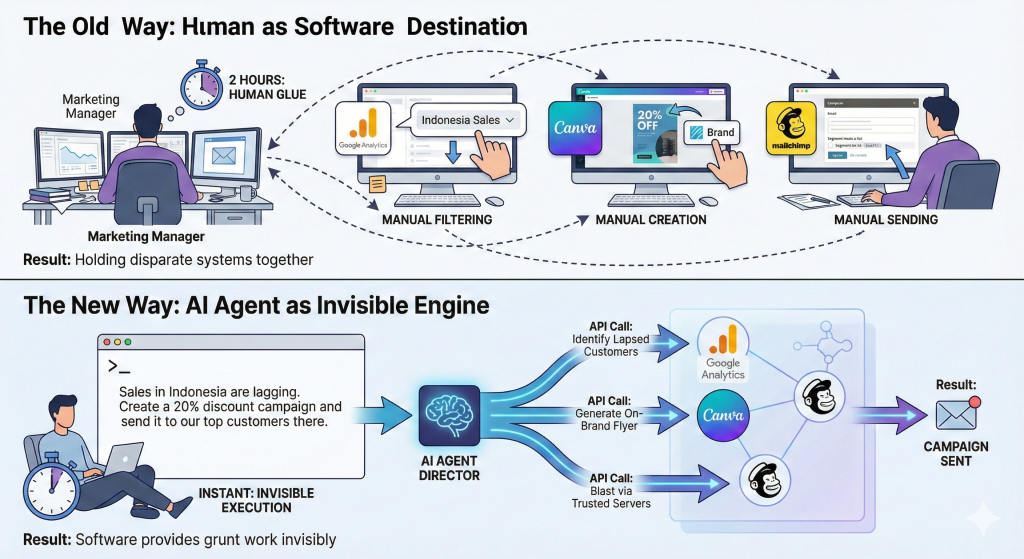

A Day in the Life: The Agentic Shift

Let’s look at how this destroys the traditional software workflow. Compare a Marketing Manager’s job today versus the Agentic reality of 2027:

The Old Way (Software as a Destination):

- You log into Google Analytics, manually clicking through filters to discover sales are down in Indonesia.

- You log into Canva, picking a template and manually dragging your brand logo to create a “20% Off” flyer.

- You log into Mailchimp, uploading the flyer, typing the copy, and manually segmenting your Indonesian VIP email list to hit send.

Result: You spent two hours acting as the “Human Glue” holding three different websites together.

The New Way (Software as an Invisible Engine): You open one command window—your AI Agent—and simply say: “Sales in Indonesia are lagging. Create a 20% discount campaign and send it to our top customers there.”

The Agent acts as the Director:

- It calls Google Analytics via API to instantly identify the lapsed customers.

- It calls Canva via API to automatically generate a perfectly on-brand flyer.

- It calls Mailchimp via API to blast the email through their trusted servers.

Result: You never looked at a single website. The software companies provided the grunt work invisibly in the background.

The Infrastructural Moats: Why Software Survives

So, why doesn’t the AI just build its own Mailchimp or Canva? Because traditional software companies own the physical and digital infrastructure.

- The Pipe Moat (Mailchimp): An AI can write a brilliant email, but if it sends 10,000 messages from an unknown server, Gmail will instantly block it as spam. Mailchimp owns the “Trusted Pipes” that the internet respects.

- The Sensor Moat (Google Analytics): An AI doesn’t inherently know what is happening on your website. Google has millions of digital sensors tracking clicks. The AI needs that raw data to “see.”

- The Guardrail Moat (Canva): An AI hallucination might accidentally make your corporate logo neon pink. Canva provides the strict “Brand Kits” that force the AI to stay inside the lines.

Software companies aren’t going to zero. They will survive by becoming the invisible plumbing of the internet.

This transformation does not automatically spell out a wave of mass defaults. Just hours after delivering another blowout earnings report, Nvidia CEO Jensen Huang pushed back against Wall Street’s doomsday narrative.

His message was blunt: AI agents are not going to cannibalize enterprise software; they are going to become its power users. As he explained, “These agentic AI will be intelligent software that uses these tools on our behalf.”

Whether it is an Excel spreadsheet, a ServiceNow workflow, or an SAP database, these platforms exist for a fundamentally good reason. They are the organizational infrastructure. AI agents won’t replace the tools; they will operate them. As Huang noted, in the end, we still need these tools to finish the work and format the information in a way humans can actually understand.

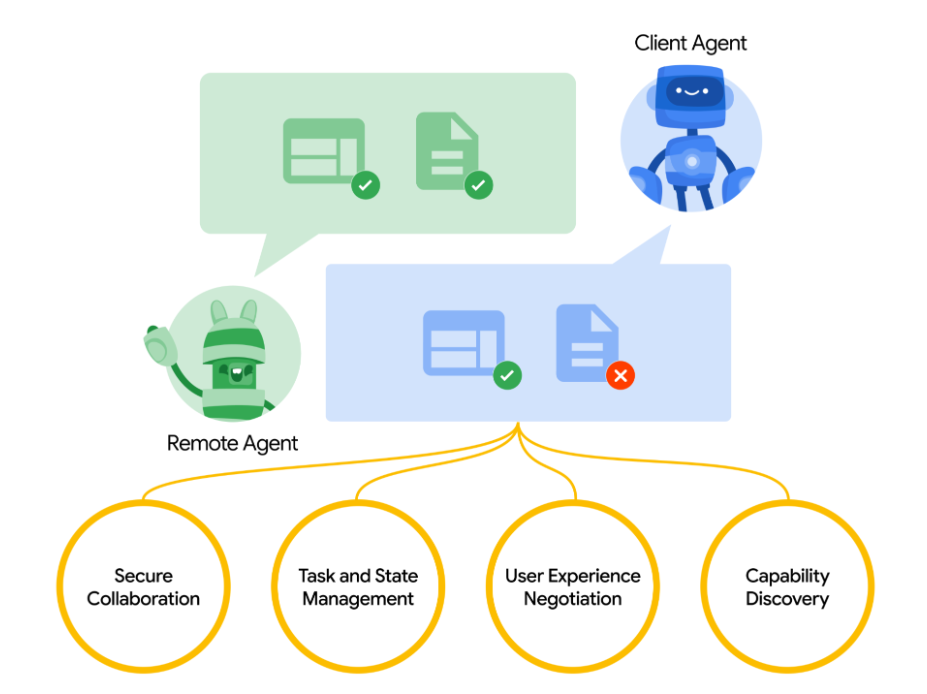

The A2A Ecosystem: When Agents Talk to Agents

If you think the future is just your company’s internal AI agent pulling levers on different software APIs, you are still thinking too small. The industry is rapidly moving toward an external, machine-to-machine economy powered by open standards like Google’s Agent-to-Agent (A2A) protocol.

While internal “multi-agent” architectures involve a closed team of AIs working within your own company’s walled garden, A2A is the open internet for agents. It allows an AI built by one company to dynamically discover, securely communicate with, and effectively hire an entirely independent AI built by another company.

How A2A works

Source: Google

In our marketing example, you wouldn’t just use one AI. Your “Director Agent” would use the A2A protocol to hire a specialized “Google Analytics Agent” to pull the data, securely negotiate with a specialized “Canva Agent” to design the creative, and hand the final product to a specialized “Mailchimp Agent” for delivery.

Software companies will no longer just build platforms; they will build and lease specialized agents into this global workforce. For the private credit industry, this adds another layer of complexity. They aren’t just underwriting software tools anymore; they are underwriting digital employees operating in an entirely autonomous machine-to-machine economy.

The Economic Obliteration and the New Moats

For the shadow banking system holding hundreds of billions in debt, this isn’t an extinction event—it is a massive repricing of risk. The software industry isn’t dying; it is simply mutating into a new form. To keep generating cash and paying back those private credit loans, software companies must fundamentally change what they sell and how they charge for it.

- The Death of the License and the Rise of the “Call”: Currently, if you have 50 employees, you buy 50 human “seats.” But what happens when a single AI agent can seamlessly do the work of those 50 people? The traditional per-seat license implodes. To survive, software companies must pivot to consumption pricing. Bosses will no longer pay flat monthly subscriptions for humans; they will pay fractions of a penny for every “API call” the agent makes. Software ceases to be a fixed subscription and becomes a variable expense—exactly like paying your electric bill.

- Data Security is the New UI: For the last decade, companies spent billions making software “human-friendly.” That capital is now stranded. Agents don’t care about sleek drop-down menus, intuitive design, or pretty color schemes. Human-targeted UI improvements are no longer a selling feature. Instead, the ultimate premium feature is data security. When autonomous machines are rapidly moving massive amounts of proprietary company data across the internet via APIs, the surviving software giants will be the ones offering ironclad security, impenetrable “guardrails,” and flawless backend execution.

- Open the API Gates: Software companies must become radically open. If a platform tries to build a walled garden and block AI agents from plugging in, the agent will simply take its transaction to a competitor that is open. In the agentic future, the path of least resistance wins the revenue.

For the $300 billion private credit market, the game has fundamentally changed. The lenders who survive this cycle will be the ones who realize that the companies they are funding are no longer selling dashboards to humans. They are selling secure, invisible tools to machines.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share

In November 2025, we warned you about the invisible engine funding the artificial intelligence boom in our piece, When AI Meets Private Credit: The Vessel, Not the Flaw. We noted that an opaque constellation of non-bank lenders was quietly fronting massive chunks of the $6.7 trillion needed for global AI infrastructure.

Six months prior, in AI Just Ate Your CRM. Now What?, we mapped out the existential threat facing traditional software, arguing that AI models would soon bypass clunky user dashboards entirely.

Today, those two distinct tectonic plates—shadow finance and AI software disruption are violently colliding. And the tremors are starting to crack the foundation of Wall Street.

Is This The Canary in the Coal Mine?

The shaking started a few weeks ago with Blue Owl Capital.

Blue Owl is a titan in the private credit space, managing nearly $300 billion in investor cash. But recently, their stock plunged as much as 10% in a single day. Why? They abruptly changed the rules on how investors can pull their money out of a major fund, shifting from a guaranteed 5% quarterly redemption to a discretionary payout model.

For perspective, Blue Owl is the second largest behind Blackstone on controlling almost half of BDC assets

Source: Financial Times, Pitchbook

Wall Street veterans immediately flashed back to August 2007. When a massive shadow lender suddenly throws up the gates to stop cash from leaving, it begs the ultimate question: What are they afraid of?

The answer lies in their loan books. In recent years, private credit has extended trillions of dollars in loans to businesses. And their absolute favorite borrower? Software companies.

By industry estimates, at least 20% of all loans extended by private credit funds—and heavily concentrated within Business Development Companies (BDCs)—have gone to software firms. But the true number is likely much higher. A recent Bloomberg analysis found at least 250 investments, worth over $9 billion, that were quietly categorized by lenders as “business services” or “specialty retail” instead of software.

Source: Bloomberg, Barclays, Bloomberg

Private credit lenders loved software for one reason: predictable, recurring revenue. A company with 5,000 employees pays for 5,000 software “seats” every single month. That steady cash flow made it incredibly easy to underwrite massive loans.

But what happens to those loans when AI obliterates the “per-seat” business model?

The “SaaSpocalypse” and the Agentic Future

Let’s add some nuance to the “AI eats software” narrative.

People are panicked that AI will simply delete software companies from existence. That is not entirely true. Software isn’t dying; it is going headless.

To understand this, we need to look at the shift from basic AI Chatbots to AI Agents. A chatbot answers your questions. An AI Agent actually executes multi-step tasks for you across the internet. But an AI Agent does not have eyes. It doesn’t care about pretty dashboards, drop-down menus, or human-friendly interfaces.

It talks to software through an API (Application Programming Interface).

Think of an API as a “Digital Drive-Thru.” If you want food, you don’t have to park, walk inside the restaurant, read the menu, and sit at a table (the old software UI). Instead, you pull your car up to the drive-thru window, hand them a specific, structured order, and they hand you the food. An API allows an AI Agent to pull up to a software company, hand it code, and get the data back instantly without ever “looking” at the website.

A Day in the Life: The Agentic Shift

Let’s look at how this destroys the traditional software workflow. Compare a Marketing Manager’s job today versus the Agentic reality of 2027:

The Old Way (Software as a Destination):

- You log into Google Analytics, manually clicking through filters to discover sales are down in Indonesia.

- You log into Canva, picking a template and manually dragging your brand logo to create a “20% Off” flyer.

- You log into Mailchimp, uploading the flyer, typing the copy, and manually segmenting your Indonesian VIP email list to hit send.

Result: You spent two hours acting as the “Human Glue” holding three different websites together.

The New Way (Software as an Invisible Engine): You open one command window—your AI Agent—and simply say: “Sales in Indonesia are lagging. Create a 20% discount campaign and send it to our top customers there.”

The Agent acts as the Director:

- It calls Google Analytics via API to instantly identify the lapsed customers.

- It calls Canva via API to automatically generate a perfectly on-brand flyer.

- It calls Mailchimp via API to blast the email through their trusted servers.

Result: You never looked at a single website. The software companies provided the grunt work invisibly in the background.

The Infrastructural Moats: Why Software Survives

So, why doesn’t the AI just build its own Mailchimp or Canva? Because traditional software companies own the physical and digital infrastructure.

- The Pipe Moat (Mailchimp): An AI can write a brilliant email, but if it sends 10,000 messages from an unknown server, Gmail will instantly block it as spam. Mailchimp owns the “Trusted Pipes” that the internet respects.

- The Sensor Moat (Google Analytics): An AI doesn’t inherently know what is happening on your website. Google has millions of digital sensors tracking clicks. The AI needs that raw data to “see.”

- The Guardrail Moat (Canva): An AI hallucination might accidentally make your corporate logo neon pink. Canva provides the strict “Brand Kits” that force the AI to stay inside the lines.

Software companies aren’t going to zero. They will survive by becoming the invisible plumbing of the internet.

This transformation does not automatically spell out a wave of mass defaults. Just hours after delivering another blowout earnings report, Nvidia CEO Jensen Huang pushed back against Wall Street’s doomsday narrative.

His message was blunt: AI agents are not going to cannibalize enterprise software; they are going to become its power users. As he explained, “These agentic AI will be intelligent software that uses these tools on our behalf.”

Whether it is an Excel spreadsheet, a ServiceNow workflow, or an SAP database, these platforms exist for a fundamentally good reason. They are the organizational infrastructure. AI agents won’t replace the tools; they will operate them. As Huang noted, in the end, we still need these tools to finish the work and format the information in a way humans can actually understand.

The A2A Ecosystem: When Agents Talk to Agents

If you think the future is just your company’s internal AI agent pulling levers on different software APIs, you are still thinking too small. The industry is rapidly moving toward an external, machine-to-machine economy powered by open standards like Google’s Agent-to-Agent (A2A) protocol.

While internal “multi-agent” architectures involve a closed team of AIs working within your own company’s walled garden, A2A is the open internet for agents. It allows an AI built by one company to dynamically discover, securely communicate with, and effectively hire an entirely independent AI built by another company.

How A2A works

Source: Google

In our marketing example, you wouldn’t just use one AI. Your “Director Agent” would use the A2A protocol to hire a specialized “Google Analytics Agent” to pull the data, securely negotiate with a specialized “Canva Agent” to design the creative, and hand the final product to a specialized “Mailchimp Agent” for delivery.

Software companies will no longer just build platforms; they will build and lease specialized agents into this global workforce. For the private credit industry, this adds another layer of complexity. They aren’t just underwriting software tools anymore; they are underwriting digital employees operating in an entirely autonomous machine-to-machine economy.

The Economic Obliteration and the New Moats

For the shadow banking system holding hundreds of billions in debt, this isn’t an extinction event—it is a massive repricing of risk. The software industry isn’t dying; it is simply mutating into a new form. To keep generating cash and paying back those private credit loans, software companies must fundamentally change what they sell and how they charge for it.

- The Death of the License and the Rise of the “Call”: Currently, if you have 50 employees, you buy 50 human “seats.” But what happens when a single AI agent can seamlessly do the work of those 50 people? The traditional per-seat license implodes. To survive, software companies must pivot to consumption pricing. Bosses will no longer pay flat monthly subscriptions for humans; they will pay fractions of a penny for every “API call” the agent makes. Software ceases to be a fixed subscription and becomes a variable expense—exactly like paying your electric bill.

- Data Security is the New UI: For the last decade, companies spent billions making software “human-friendly.” That capital is now stranded. Agents don’t care about sleek drop-down menus, intuitive design, or pretty color schemes. Human-targeted UI improvements are no longer a selling feature. Instead, the ultimate premium feature is data security. When autonomous machines are rapidly moving massive amounts of proprietary company data across the internet via APIs, the surviving software giants will be the ones offering ironclad security, impenetrable “guardrails,” and flawless backend execution.

- Open the API Gates: Software companies must become radically open. If a platform tries to build a walled garden and block AI agents from plugging in, the agent will simply take its transaction to a competitor that is open. In the agentic future, the path of least resistance wins the revenue.

For the $300 billion private credit market, the game has fundamentally changed. The lenders who survive this cycle will be the ones who realize that the companies they are funding are no longer selling dashboards to humans. They are selling secure, invisible tools to machines.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share