No More ‘Just Right’: Investing After Goldilocks

No More ‘Just Right’: Investing After Goldilocks

“Why is going to the mall so expensive now?”

That’s what a coworker asked me over lunch last week.

He wasn’t talking about a luxury shopping spree. Just a casual weekend outing — lunch, coffee, maybe a bit of browsing. But somehow, it still felt like his wallet had been mugged by a smiling barista and a parking meter.

“It’s not like prices exploded,” he said. “But I always leave feeling poorer than I expected.”

That stuck with me. Because he’s right — something has changed. Not always in ways you can quantify on a receipt, but in how everyday life feels more expensive.

And it’s not just him.

From toothpaste to concert tickets to a bowl of ramen that used to be a daily lunch feature is now a weekend treat instead — the vibes are off. We all feel it. But what’s causing it?

Welcome to the Post-Goldilocks Economy

For 40 years, investors had it good.

- Interest rates kept falling.

- Globalization kept costs low.

- Central banks looked like geniuses.

- Profit margins expanded.

- And your passive 60/40 portfolio? Worked like magic.

This “Great Disinflation” wasn’t divine intervention — it was engineered on five key pillars:

- Cheap labor (thank you, China WTO 2001)

- Frictionless trade (hello, supply chains)

- Central bank credibility (remember when we trusted policy?)

- Demographic tailwinds (young, productive populations)

- Tech productivity (more output, same costs)

Goodbye to the Old Normal of low rates, we are now entering the New Reality of sticky inflation

Together, these forces created a world where companies didn’t need pricing power. Margins went up even as prices stayed flat. It was the investor’s version of having your cake and eating it too — delivered via drone, of course.

But then the cake caught fire.

Scarcity Strikes Back

COVID didn’t just break supply chains. It broke the illusion.

- Just-in-time became just-too-fragile.

- Energy nationalism replaced energy abundance.

- Geopolitics re-entered the chat.

Now, inflation isn’t “transitory.” It’s structural.

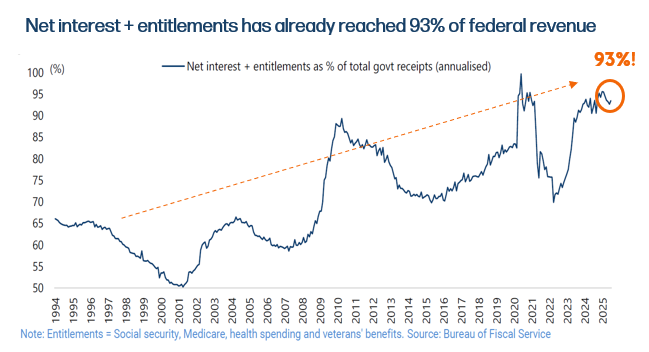

The U.S. Federal Reserve finds itself in a chokehold: raising rates risks detonating the debt bomb, but cutting rates lets inflation rage on. In fact, by 2025, the U.S. is spending 93% of its tax income on just two things: entitlements and interest payments. That leaves… almost nothing for anything else.

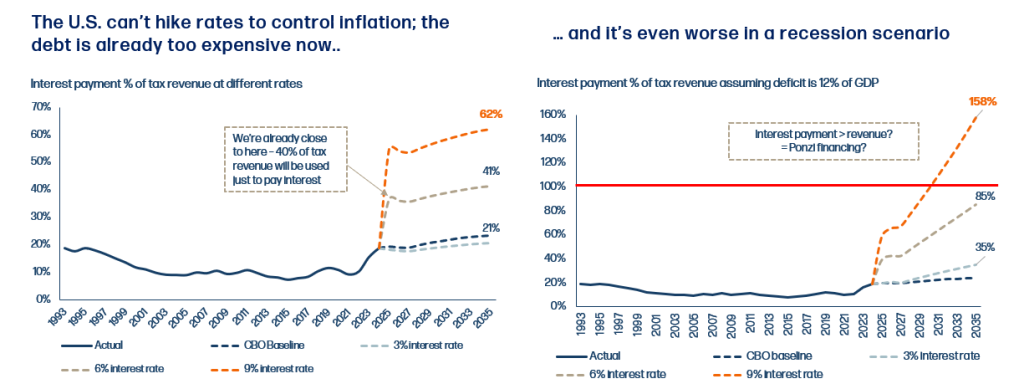

Currently, the U.S. fed fund rate is at 4.5%. If borrowing costs hit even 6% which isn’t that far off, interest alone eats up 40% of tax revenue. And at 9%? The math turns apocalyptic: interest payments could consume more than 100% of revenue under a recession scenario. That’s not fiscal policy — that’s an unsustainable feedback loop.

Paying off just the interest on U.S. debt will quickly deplete U.S. tax revenue. Over 100% of tax revenue will go towards paying back only interest if the U.S. enters a recession!

CPI Is a Mirage — And We’ve Been Here Before

Sound familiar?

We explored this in our earlier blog, The Invisible Inflation We Live With — where inflation wasn’t roaring through your Bloomberg terminal, but sneaking in through smaller chocolate bars, earlier hotel check out times, and subscription plans with less of everything.

That was the consumer-facing version of inflation.

This is the investor-facing one.

Because the same silent shrinkage is happening inside portfolios.

Your bond allocation? Still there on paper — but its real value is slipping, while its role as a diversifier is being squeezed by rising inflation and yields.

Your passive equity exposure? Margin pressure is coming.

That 60/40 mattress? It may need a serious re-stuffing. To be clear: the 60/40 portfolio isn’t dead. But it was built for a world of falling rates, stable currencies, and declining inflation.

That world is now in the rear-view mirror. In its place, we face higher volatility, persistent price pressures, and the return of macro risks we forgot to hedge for.

In this new world, passive portfolios that track the past may not protect the future.

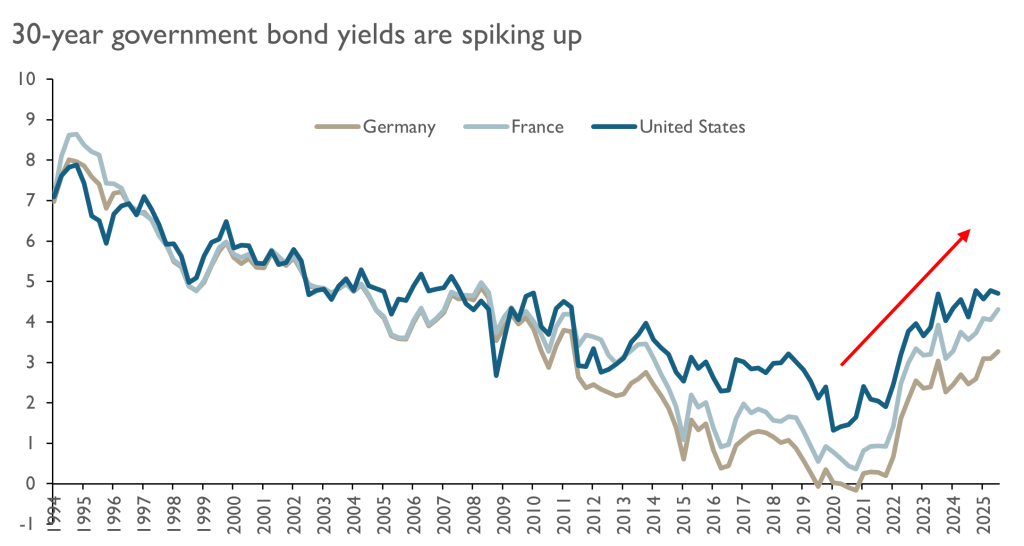

Are longer term bonds really “risk free”? These 30-year ones seem to be struggling to regain investor confidence

So Where Do You Hide?

Well, you don’t hide.

You own the companies that can name their price.

While the average company is getting squeezed between rising input costs and price-sensitive consumers, Pricing Power Equities (PPEs) are doing the opposite:

✅ Raising prices

✅ Keeping volumes steady

✅ Defending (or even expanding) margins

These businesses are not just inflation survivors. They are inflation beneficiaries.

In short, they don’t take prices — they make them.

Pricing Power: The Anti-Inflation Trend?

Here’s what makes this strategy weirdly contrarian: it goes against almost everything we’ve been taught.

“Buy what’s cheap.”

✅ No. Buy what’s irreplaceable.

“Avoid monopolies.”

✅ Not anymore. Embrace natural monopolies, especially ones powered by scale, brand, or ecosystem lock-in.

“Inflation hurts everyone.”

✅ Not the companies who pass it on without losing loyalty, volume, or market share.

Of course, pricing power isn’t the only hero in the inflation story. Hard assets like gold, supply-constrained commodities, and substitution plays all shine in this regime. But pricing power is a rising co-star — elegant, scalable, and increasingly central to how we think about structural resilience. In the 2010s, winners were defined by how lean they could get — the kings of efficiency.

In the 2020s, winners are defined by how much they can charge — and still be loved.

In this new playbook, you’re not looking for cost cutters. You’re looking for:

- Companies that own their supply chains.

- Brands that make people feel something.

- Platforms with user ecosystems so sticky you need social rehab to leave.

- Businesses riding the tailwind of government-made scarcity — like quotas, export bans, or downstream mandates

Final Thought: Scarcity Is the New Alpha

The world of cheap capital, cheap labor, and cheap oil is gone.

We’re now in the age of expensive everything — except, perhaps, your Netflix subscription (for now). In this world, only one thing protects your capital:

Owning the companies that make the rules — not follow them.

Tara Mulia

Admin heyokha

Share

“Why is going to the mall so expensive now?”

That’s what a coworker asked me over lunch last week.

He wasn’t talking about a luxury shopping spree. Just a casual weekend outing — lunch, coffee, maybe a bit of browsing. But somehow, it still felt like his wallet had been mugged by a smiling barista and a parking meter.

“It’s not like prices exploded,” he said. “But I always leave feeling poorer than I expected.”

That stuck with me. Because he’s right — something has changed. Not always in ways you can quantify on a receipt, but in how everyday life feels more expensive.

And it’s not just him.

From toothpaste to concert tickets to a bowl of ramen that used to be a daily lunch feature is now a weekend treat instead — the vibes are off. We all feel it. But what’s causing it?

Welcome to the Post-Goldilocks Economy

For 40 years, investors had it good.

- Interest rates kept falling.

- Globalization kept costs low.

- Central banks looked like geniuses.

- Profit margins expanded.

- And your passive 60/40 portfolio? Worked like magic.

This “Great Disinflation” wasn’t divine intervention — it was engineered on five key pillars:

- Cheap labor (thank you, China WTO 2001)

- Frictionless trade (hello, supply chains)

- Central bank credibility (remember when we trusted policy?)

- Demographic tailwinds (young, productive populations)

- Tech productivity (more output, same costs)

Goodbye to the Old Normal of low rates, we are now entering the New Reality of sticky inflation

Together, these forces created a world where companies didn’t need pricing power. Margins went up even as prices stayed flat. It was the investor’s version of having your cake and eating it too — delivered via drone, of course.

But then the cake caught fire.

Scarcity Strikes Back

COVID didn’t just break supply chains. It broke the illusion.

- Just-in-time became just-too-fragile.

- Energy nationalism replaced energy abundance.

- Geopolitics re-entered the chat.

Now, inflation isn’t “transitory.” It’s structural.

The U.S. Federal Reserve finds itself in a chokehold: raising rates risks detonating the debt bomb, but cutting rates lets inflation rage on. In fact, by 2025, the U.S. is spending 93% of its tax income on just two things: entitlements and interest payments. That leaves… almost nothing for anything else.

Currently, the U.S. fed fund rate is at 4.5%. If borrowing costs hit even 6% which isn’t that far off, interest alone eats up 40% of tax revenue. And at 9%? The math turns apocalyptic: interest payments could consume more than 100% of revenue under a recession scenario. That’s not fiscal policy — that’s an unsustainable feedback loop.

Paying off just the interest on U.S. debt will quickly deplete U.S. tax revenue. Over 100% of tax revenue will go towards paying back only interest if the U.S. enters a recession!

CPI Is a Mirage — And We’ve Been Here Before

Sound familiar?

We explored this in our earlier blog, The Invisible Inflation We Live With — where inflation wasn’t roaring through your Bloomberg terminal, but sneaking in through smaller chocolate bars, earlier hotel check out times, and subscription plans with less of everything.

That was the consumer-facing version of inflation.

This is the investor-facing one.

Because the same silent shrinkage is happening inside portfolios.

Your bond allocation? Still there on paper — but its real value is slipping, while its role as a diversifier is being squeezed by rising inflation and yields.

Your passive equity exposure? Margin pressure is coming.

That 60/40 mattress? It may need a serious re-stuffing. To be clear: the 60/40 portfolio isn’t dead. But it was built for a world of falling rates, stable currencies, and declining inflation.

That world is now in the rear-view mirror. In its place, we face higher volatility, persistent price pressures, and the return of macro risks we forgot to hedge for.

In this new world, passive portfolios that track the past may not protect the future.

Are longer term bonds really “risk free”? These 30-year ones seem to be struggling to regain investor confidence

So Where Do You Hide?

Well, you don’t hide.

You own the companies that can name their price.

While the average company is getting squeezed between rising input costs and price-sensitive consumers, Pricing Power Equities (PPEs) are doing the opposite:

✅ Raising prices

✅ Keeping volumes steady

✅ Defending (or even expanding) margins

These businesses are not just inflation survivors. They are inflation beneficiaries.

In short, they don’t take prices — they make them.

Pricing Power: The Anti-Inflation Trend?

Here’s what makes this strategy weirdly contrarian: it goes against almost everything we’ve been taught.

“Buy what’s cheap.”

✅ No. Buy what’s irreplaceable.

“Avoid monopolies.”

✅ Not anymore. Embrace natural monopolies, especially ones powered by scale, brand, or ecosystem lock-in.

“Inflation hurts everyone.”

✅ Not the companies who pass it on without losing loyalty, volume, or market share.

Of course, pricing power isn’t the only hero in the inflation story. Hard assets like gold, supply-constrained commodities, and substitution plays all shine in this regime. But pricing power is a rising co-star — elegant, scalable, and increasingly central to how we think about structural resilience. In the 2010s, winners were defined by how lean they could get — the kings of efficiency.

In the 2020s, winners are defined by how much they can charge — and still be loved.

In this new playbook, you’re not looking for cost cutters. You’re looking for:

- Companies that own their supply chains.

- Brands that make people feel something.

- Platforms with user ecosystems so sticky you need social rehab to leave.

- Businesses riding the tailwind of government-made scarcity — like quotas, export bans, or downstream mandates

Final Thought: Scarcity Is the New Alpha

The world of cheap capital, cheap labor, and cheap oil is gone.

We’re now in the age of expensive everything — except, perhaps, your Netflix subscription (for now). In this world, only one thing protects your capital:

Owning the companies that make the rules — not follow them.

Tara Mulia

Admin heyokha

Share