The End of an Era: Why We Are Finally Calling It

The End of an Era: Why We Are Finally Calling It

Everyone knows the world is fracturing. We cannot read a financial headline today without seeing the impact of tariffs or supply chain realignments. But acknowledging a headline is not the same as pricing in a permanent reality.

The broader market still treats geopolitical friction as a temporary headache, viewing it as a short-term risk premium that will eventually be resolved by the next election cycle or a neat trade deal. They still believe, deep down, that capital’s ultimate loyalty is to the lowest marginal cost. They are wrong. The era of frictionless borders is on life support, and its impending death is a trend we have been tracking for years.

The Red Thread: We Saw the Fractures in 2018

We have been talking about the reality of deglobalization as far back as our Q3 2018 report. When the U.S. and China first started trading tariff blows, the mainstream financial media brushed it off as a temporary political spat that would be resolved with a neat trade deal.

We disagreed. We noted then that this was the first tremor of a massive, structural decoupling.

By our Q2 and Q3 2019 reports, the writing was clearly on the wall. The trade dispute had morphed into a full-blown technology cold war. With entities being blacklisted and supply chains fracturing, we explicitly warned that the era of relying purely on hyper-efficient global trade was coming to an end. We saw that the unipolar world order was breaking apart and that strategic competition was replacing economic integration. We knew that a system built purely on chasing the lowest marginal cost across oceans was fundamentally fragile.

Read our reports here!

There is clear external validation of just how permanent that fracture has become, look at the architecture of the East today. The Shanghai Cooperation Organisation (SCO) now counts 10 full members accounting for 40% of the world’s population, 30% of global GDP (PPP), and 60% of the Eurasian landmass. All in all, they are holding 20% of proven global oil reserves and 44% of proven natural gas. This is not some fringe realignment. It is a structured, institutional counter to the Western-led order.

The Present Reality: The “Rupture” is Here

Fast forward to today, and the exact deglobalization thesis we mapped out in 2018 is now the consensus among global leaders. There is proof that the old system is breaking, just listen to the people who used to run it.

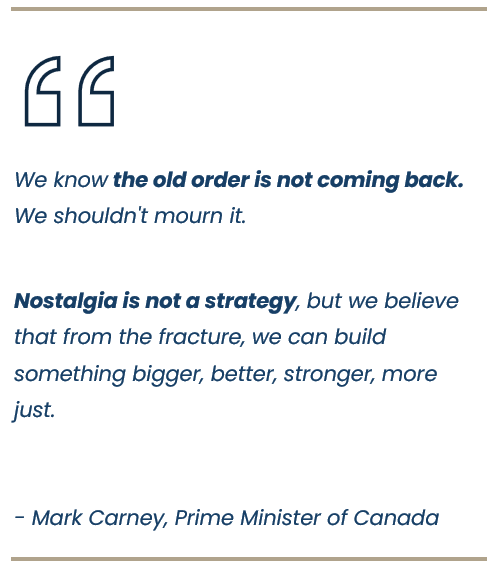

At the World Economic Forum earlier this year, Mark Carney bluntly defined the current state of international relations as a “rupture,” noting that it is not merely a transition. He warned that the old rules-based order no longer functions as advertised, with economic integration now being actively weaponized by great powers.

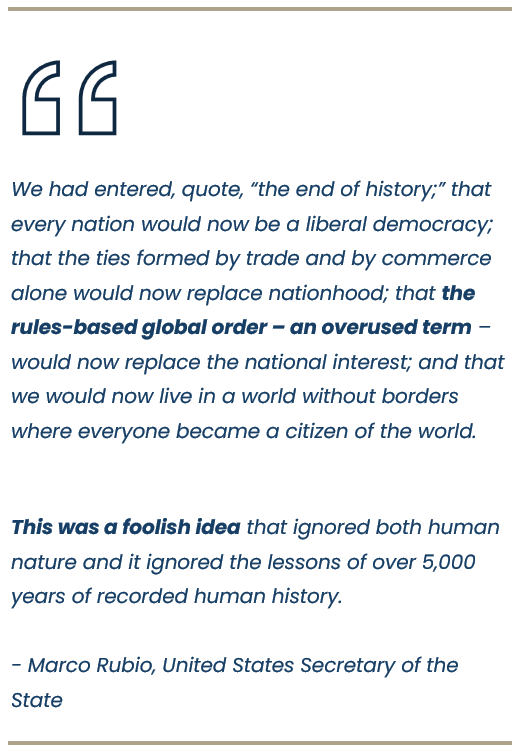

Meanwhile, U.S. Secretary of State Marco Rubio has explicitly declared that the era of globalization is over. He has consistently argued that the old economic consensus failed to moderate national rivalries, pushing instead for aggressive industrial policy, new trade barriers, and a focus on national security over cheap consumer goods.

The clearest proof of this rupture is the semiconductor war. Initial U.S. export controls were viewed in Beijing as a declaration of economic war. The response? According to the Australian Strategic Policy Institute, China now leads in 57 of 64 critical technologies—up from leading in just three a couple of decades ago. The attempt to contain China through tech restrictions ultimately backfired, incentivizing self-reliance and accelerating the very technological competition it sought to prevent.

Now, the U.S. is reacting in kind. Despite heavy political rhetoric regarding deregulation, the U.S. government spent heavily in 2025 to take direct equity stakes in major private companies like Intel and MP Materials. When the U.S. government starts directly buying 10% to 15% stakes in chipmakers and rare earth mines, they are no longer operating in a free-market global economy. This is what weaponized economic integration looks like from the inside.

Capital Chasing Security

The data and the rhetoric are finally aligned. We are watching the artificial intelligence arms race turn aggressively physical. Governments are finally waking up to the fact that they cannot power a sovereign AI grid or secure a defense supply chain with a multilateral trade agreement. They need secure transit and hard assets.

Capital is no longer chasing the lowest marginal cost. It is chasing security.

The transition is brutal. The symptoms are everywhere: sticky inflation, weaponized industrial policy, and a panicked rush into hard assets and physical commodities.

Since we have been warning about this exact trend for over half a decade, and looking at the current state of the fractured global board, we felt it was finally time to acknowledge the inevitable.

So, we wrote a premature obituary.

But every death brings a rebirth. As the illusion of a frictionless global economy is laid to rest, a new era is already rising from the ashes. This is the renaissance of the physical.

When supply chains fracture and fiat currencies are actively weaponized in great power competition, paper promises lose their premium. In times of deep systemic fear, capital instinctively flees the abstract and seeks out the tangible.

This is exactly why our conviction in precious metals and hard assets has never been stronger.

While the broader market panics over every geopolitical headline and scrambles to adjust their portfolios to the latest tariff threat, we are already anchored. Physical gold, silver, and critical industrial commodities do not rely on friendly diplomatic relations or multilateral trade agreements to hold their value. They carry no counterparty risk. They are the ultimate form of financial sovereignty.

We are simply holding the assets built to thrive in the reality of the new, fractured world.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Share

Admin heyokha

Everyone knows the world is fracturing. We cannot read a financial headline today without seeing the impact of tariffs or supply chain realignments. But acknowledging a headline is not the same as pricing in a permanent reality.

The broader market still treats geopolitical friction as a temporary headache, viewing it as a short-term risk premium that will eventually be resolved by the next election cycle or a neat trade deal. They still believe, deep down, that capital’s ultimate loyalty is to the lowest marginal cost. They are wrong. The era of frictionless borders is on life support, and its impending death is a trend we have been tracking for years.

The Red Thread: We Saw the Fractures in 2018

We have been talking about the reality of deglobalization as far back as our Q3 2018 report. When the U.S. and China first started trading tariff blows, the mainstream financial media brushed it off as a temporary political spat that would be resolved with a neat trade deal.

We disagreed. We noted then that this was the first tremor of a massive, structural decoupling.

By our Q2 and Q3 2019 reports, the writing was clearly on the wall. The trade dispute had morphed into a full-blown technology cold war. With entities being blacklisted and supply chains fracturing, we explicitly warned that the era of relying purely on hyper-efficient global trade was coming to an end. We saw that the unipolar world order was breaking apart and that strategic competition was replacing economic integration. We knew that a system built purely on chasing the lowest marginal cost across oceans was fundamentally fragile.

Read our reports here!

There is clear external validation of just how permanent that fracture has become, look at the architecture of the East today. The Shanghai Cooperation Organisation (SCO) now counts 10 full members accounting for 40% of the world’s population, 30% of global GDP (PPP), and 60% of the Eurasian landmass. All in all, they are holding 20% of proven global oil reserves and 44% of proven natural gas. This is not some fringe realignment. It is a structured, institutional counter to the Western-led order.

The Present Reality: The “Rupture” is Here

Fast forward to today, and the exact deglobalization thesis we mapped out in 2018 is now the consensus among global leaders. There is proof that the old system is breaking, just listen to the people who used to run it.

At the World Economic Forum earlier this year, Mark Carney bluntly defined the current state of international relations as a “rupture,” noting that it is not merely a transition. He warned that the old rules-based order no longer functions as advertised, with economic integration now being actively weaponized by great powers.

Meanwhile, U.S. Secretary of State Marco Rubio has explicitly declared that the era of globalization is over. He has consistently argued that the old economic consensus failed to moderate national rivalries, pushing instead for aggressive industrial policy, new trade barriers, and a focus on national security over cheap consumer goods.

The clearest proof of this rupture is the semiconductor war. Initial U.S. export controls were viewed in Beijing as a declaration of economic war. The response? According to the Australian Strategic Policy Institute, China now leads in 57 of 64 critical technologies—up from leading in just three a couple of decades ago. The attempt to contain China through tech restrictions ultimately backfired, incentivizing self-reliance and accelerating the very technological competition it sought to prevent.

Now, the U.S. is reacting in kind. Despite heavy political rhetoric regarding deregulation, the U.S. government spent heavily in 2025 to take direct equity stakes in major private companies like Intel and MP Materials. When the U.S. government starts directly buying 10% to 15% stakes in chipmakers and rare earth mines, they are no longer operating in a free-market global economy. This is what weaponized economic integration looks like from the inside.

Capital Chasing Security

The data and the rhetoric are finally aligned. We are watching the artificial intelligence arms race turn aggressively physical. Governments are finally waking up to the fact that they cannot power a sovereign AI grid or secure a defense supply chain with a multilateral trade agreement. They need secure transit and hard assets.

Capital is no longer chasing the lowest marginal cost. It is chasing security.

The transition is brutal. The symptoms are everywhere: sticky inflation, weaponized industrial policy, and a panicked rush into hard assets and physical commodities.

Since we have been warning about this exact trend for over half a decade, and looking at the current state of the fractured global board, we felt it was finally time to acknowledge the inevitable.

So, we wrote a premature obituary.

But every death brings a rebirth. As the illusion of a frictionless global economy is laid to rest, a new era is already rising from the ashes. This is the renaissance of the physical.

When supply chains fracture and fiat currencies are actively weaponized in great power competition, paper promises lose their premium. In times of deep systemic fear, capital instinctively flees the abstract and seeks out the tangible.

This is exactly why our conviction in precious metals and hard assets has never been stronger.

While the broader market panics over every geopolitical headline and scrambles to adjust their portfolios to the latest tariff threat, we are already anchored. Physical gold, silver, and critical industrial commodities do not rely on friendly diplomatic relations or multilateral trade agreements to hold their value. They carry no counterparty risk. They are the ultimate form of financial sovereignty.

We are simply holding the assets built to thrive in the reality of the new, fractured world.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Share

Admin heyokha