The Calorie Chokepoint: Why Hormuz is a Food Crisis in Slow Motion

The Calorie Chokepoint: Why Hormuz is a Food Crisis in Slow Motion

We sat down to watch the latest sci-fi film “Project Hail Mary” last week expecting something light but got the opposite.

Early in the film, the head of an international task force lays out the stakes to the main character being sent on a desperate space mission: an alien microorganism is slowly consuming the sun’s energy. At current trajectory of colder temperatures, food production will collapses and roughly 25% of the world’s population will die of starvation. Very dire situation for the main character.

Source: MGM

We couldn’t stop thinking about it — not because we’re facing a dying sun, but because a version of a similar downward cascade is playing out right now in the Strait of Hormuz. The oil story has dominated every headline. What isn’t being talked about nearly enough is what’s happening to food.

This Is Not Just an Oil Story

Since late February 2026, the Strait of Hormuz has been effectively disrupted, caught in the crossfire of an escalating Iran conflict. The world knows this. Markets have priced in the oil shock. Analysts have run the Brent scenarios. That conversation is well underway.

Here is the conversation that hasn’t started yet.

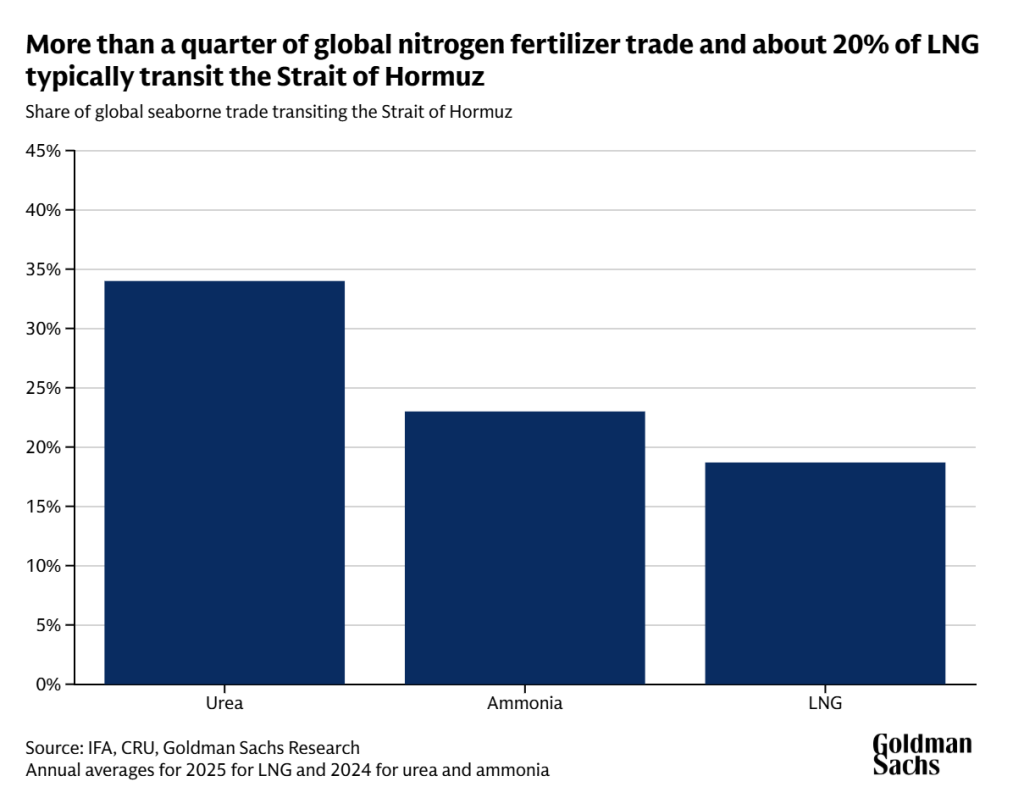

The Strait of Hormuz isn’t just the world’s most important oil chokepoint. It is also the jugular vein of global fertilizer trade. And right now, it is being squeezed.

Source: Goldman Sachs

Consider what flows through those 33 kilometers of water:

- Around 34% of global urea shipments

- Around 23% of global ammonia

- Around 20% of global phosphates

That means close to 50% of world urea exports originate west of Hormuz and must pass through it. That also means close to 30% of all global fertilizer trade transits the Strait.

Oil gets the headlines because its price moves immediately and visibly. Fertilizer deserves its own headline because its price also moves quite quickly and the damage lands months later in the food supply, long after the Strait has reopened and the world has moved on.

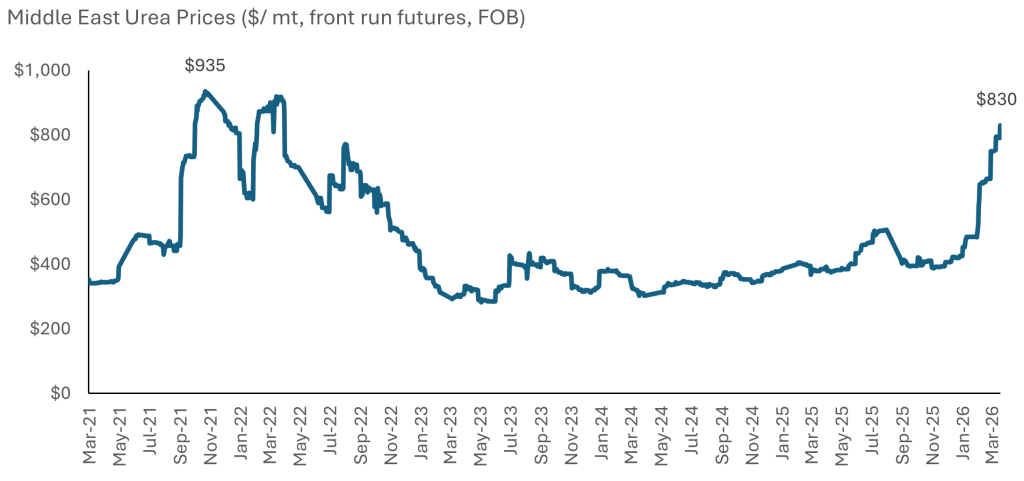

The Price Shock Is Already Here

We said slow motion. But the first act has already been fast. In the roughly six weeks since disruption intensified, fertilizer markets have repriced violently:

- Urea: up around 70% in six weeks, now above $800/ton; up roughly 104% year-to-date on a futures basis

- India import bids: $935–959/ton — roughly double what buyers were paying two months ago

To put the immediate jolt in context: in the first weeks post-disruption, fertilizer markets saw a 28–30% spike. That’s not a rounding error. That’s a supply chain cardiac event.

Will we see it test higher prices than the Russian-Ukraine war?

Source: Bloomberg

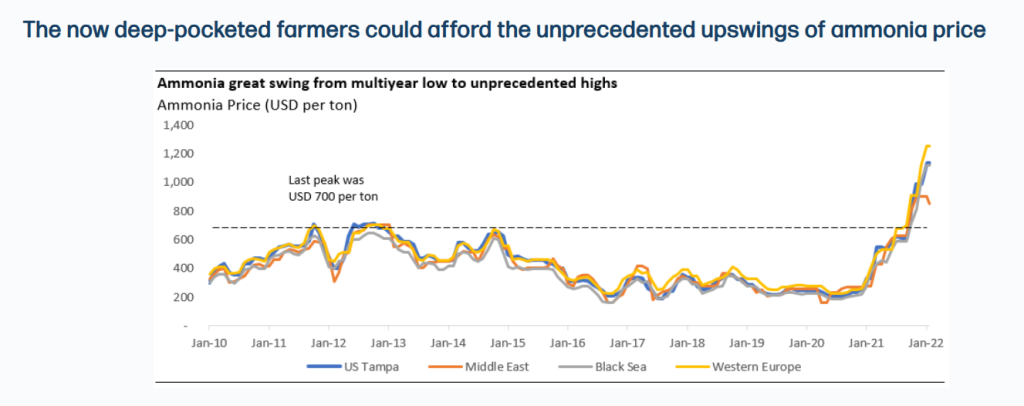

We Have Seen This Movie Before — In 2022

In our earlier blog “Rising Fertiliser and Food Prices: Who Will Be Spared?”, written in April 2022, we tracked what happened when Russia invaded Ukraine and effectively weaponized the nitrogen supply chain. The mechanism was the same: a geopolitical shock hit the gas supply (ammonia’s key feedstock), fertilizer plants went dark across Europe, and prices detonated.

The 2022 Ukraine shock produced:

- Ammonia prices up ~200% from pre-war levels at peak

- Global urea prices hitting record highs above $900/ton

- Food price index (FAO) reaching its highest level ever recorded — March 2022

- Export bans from India, China, and Russia as countries hoarded supply

- Egypt, Sri Lanka, and Pakistan facing acute fertilizer shortages

In case you need a refresher of how it went down back in 2022

Source: Heyokha research, Bloomberg

In 2022, the shock was upstream energy: gas prices broke fertilizer production. In 2026, the shock is logistics: a physical blockade on the world’s most fertilizer-intensive shipping lane. The mechanism is different. The destination is the same.

The Chain Reaction Nobody Is Pricing In

Here is what makes this crisis different from an oil shock — and more dangerous for long-term inflation. Oil prices move, and within months, the effect is felt at the pump. Consumers adjust. Central banks watch CPI. The feedback loop is fast and visible.

Fertilizer doesn’t work that way. It operates on an agricultural calendar. And right now, we are in the exact wrong moment of that calendar.

The sequence looks like this:

- Fertilizer prices spike (now) → farmers in Asia, Africa, and LatAm face input costs they cannot absorb

- Planting decisions change (within weeks) → farmers reduce application rates, switch to lower-input crops, or skip planting altogether

- Crop yields fall (harvest season, Q3–Q4 2026) → lower output than the market expects

- Food supply tightens (post-harvest) → grain, rice, and staple inventories shrink

- Food prices rise (lagged CPI impact) → the inflation the market didn’t price in arrives on schedule

This is not cyclical inflation. This is not a demand shock that the Fed can cool with a rate hike. This is structural inflation driven by a real, physical constraint on one of the most inelastic goods on earth: food. You cannot print more rice. You cannot stimulate your way to a better harvest.

And crucially — the data will look fine right now. Commodity desks will note that food CPI has not moved. Analysts will say the market is calm. That calm is the problem. The harvest hasn’t happened yet.

Who Gets Hit First

Not everyone feels this equally. The geography of vulnerability follows the fertilizer import map, and it skews heavily toward the countries least able to absorb it. India is already bidding urea at $935–959 per ton, roughly double two months ago. Bangladesh, Pakistan, and much of Sub-Saharan Africa run food expenditure ratios above 50% of household income; a 30–50% fertilizer input shock is not an abstraction for the people at the end of this supply chain — it is a decision about whether to plant at all. When farmers in import-dependent economies reduce application rates or skip a crop cycle, the deficit gets quietly written into soil that won’t talk back until harvest season.

Source: Bloomberg

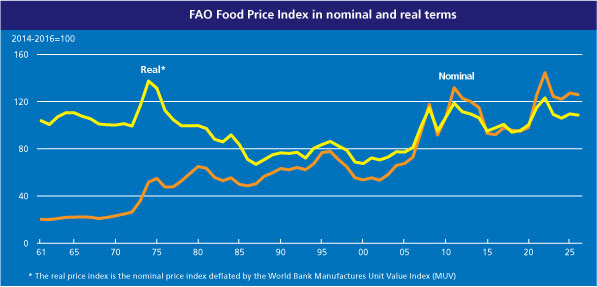

The Inflation That Was Already Coming

We want to be precise about something: this is not a new worry for us. We first wrote about ammonia as a geopolitical weapon in early 2022, in “Rising Fertiliser and Food Prices: Who Will Be Spared?” — before most investors were treating it as anything other than a niche commodity story. The thesis then was that supply chain breakdown, energy crisis, and geopolitical tension had crystallised into a perfect storm for food prices, and that the effects would travel through the system far more slowly and durably than markets expected.

Later that year, when food prices briefly cooled and analysts declared the crisis over, we pushed back in “The End of the Decade of Plenty” blog back in November 2022. The FAO food price index had fallen 14.7% from its March peak, but the dollar had risen 21.5% over the same period, meaning most countries were actually paying more in local currency terms. Export bans were proliferating. The underlying supply-side pressures had not resolved; they had merely gone quiet. We said then: don’t mistake a pause for a resolution.

That lesson applies with full force today. The latest data from FAO ((Food and Agriculture Organization of the United Nations)) is already seeing Food Price Index rising for a second consecutive month, driven by energy related pressures from the Middle East conflict.

Averaged 128.5 points in March 2026, up 3.0 points from February

Source: FAO

What we are describing is not a cyclical event central banks can hike away. It is structural inflation — driven by real, physical constraints on the most inelastic thing on earth. You cannot print more rice. The Hormuz crisis will eventually ease and shipping lanes will reopen, but the harvest that didn’t happen won’t come back.

You cannot retroactively fertilize a field that went under-dosed in April. The consequences are already baked into the ground.

The question for investors isn’t whether this inflation arrives, it’s whether you’re positioned for a world where food prices reprice structurally and stay there. We’ve long believed the answer lies in owning the things scarcity makes more valuable and the kind of exposure to real assets that actually benefits when the fiction of infinite, frictionless abundance runs into a closed strait. The broader point is the same one we’ve been making since the decade of plenty ended: efficiency was the trade of the last era; resilience is the trade of this one.

In the film, (spoiler alert) humanity gets its Hail Mary — a one-in-a-billion miracle, executed by a lone astronaut and some extra-terrestrial help, arriving in the nick of time. Inspiring. Also not our base case.

What is our Hail Mary?

source: MGM

The real-world version of this story doesn’t end with a miracle. It ends with whoever read the data early enough being fine, and whoever assumed the world would stay frictionless being very surprised by their future grocery bill.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share

We sat down to watch the latest sci-fi film “Project Hail Mary” last week expecting something light but got the opposite.

Early in the film, the head of an international task force lays out the stakes to the main character being sent on a desperate space mission: an alien microorganism is slowly consuming the sun’s energy. At current trajectory of colder temperatures, food production will collapses and roughly 25% of the world’s population will die of starvation. Very dire situation for the main character.

Source: MGM

We couldn’t stop thinking about it — not because we’re facing a dying sun, but because a version of a similar downward cascade is playing out right now in the Strait of Hormuz. The oil story has dominated every headline. What isn’t being talked about nearly enough is what’s happening to food.

This Is Not Just an Oil Story

Since late February 2026, the Strait of Hormuz has been effectively disrupted, caught in the crossfire of an escalating Iran conflict. The world knows this. Markets have priced in the oil shock. Analysts have run the Brent scenarios. That conversation is well underway.

Here is the conversation that hasn’t started yet.

The Strait of Hormuz isn’t just the world’s most important oil chokepoint. It is also the jugular vein of global fertilizer trade. And right now, it is being squeezed.

Source: Goldman Sachs

Consider what flows through those 33 kilometers of water:

- Around 34% of global urea shipments

- Around 23% of global ammonia

- Around 20% of global phosphates

That means close to 50% of world urea exports originate west of Hormuz and must pass through it. That also means close to 30% of all global fertilizer trade transits the Strait.

Oil gets the headlines because its price moves immediately and visibly. Fertilizer deserves its own headline because its price also moves quite quickly and the damage lands months later in the food supply, long after the Strait has reopened and the world has moved on.

The Price Shock Is Already Here

We said slow motion. But the first act has already been fast. In the roughly six weeks since disruption intensified, fertilizer markets have repriced violently:

- Urea: up around 70% in six weeks, now above $800/ton; up roughly 104% year-to-date on a futures basis

- India import bids: $935–959/ton — roughly double what buyers were paying two months ago

To put the immediate jolt in context: in the first weeks post-disruption, fertilizer markets saw a 28–30% spike. That’s not a rounding error. That’s a supply chain cardiac event.

Will we see it test higher prices than the Russian-Ukraine war?

Source: Bloomberg

We Have Seen This Movie Before — In 2022

In our earlier blog “Rising Fertiliser and Food Prices: Who Will Be Spared?”, written in April 2022, we tracked what happened when Russia invaded Ukraine and effectively weaponized the nitrogen supply chain. The mechanism was the same: a geopolitical shock hit the gas supply (ammonia’s key feedstock), fertilizer plants went dark across Europe, and prices detonated.

The 2022 Ukraine shock produced:

- Ammonia prices up ~200% from pre-war levels at peak

- Global urea prices hitting record highs above $900/ton

- Food price index (FAO) reaching its highest level ever recorded — March 2022

- Export bans from India, China, and Russia as countries hoarded supply

- Egypt, Sri Lanka, and Pakistan facing acute fertilizer shortages

In case you need a refresher of how it went down back in 2022

Source: Heyokha research, Bloomberg

In 2022, the shock was upstream energy: gas prices broke fertilizer production. In 2026, the shock is logistics: a physical blockade on the world’s most fertilizer-intensive shipping lane. The mechanism is different. The destination is the same.

The Chain Reaction Nobody Is Pricing In

Here is what makes this crisis different from an oil shock — and more dangerous for long-term inflation. Oil prices move, and within months, the effect is felt at the pump. Consumers adjust. Central banks watch CPI. The feedback loop is fast and visible.

Fertilizer doesn’t work that way. It operates on an agricultural calendar. And right now, we are in the exact wrong moment of that calendar.

The sequence looks like this:

- Fertilizer prices spike (now) → farmers in Asia, Africa, and LatAm face input costs they cannot absorb

- Planting decisions change (within weeks) → farmers reduce application rates, switch to lower-input crops, or skip planting altogether

- Crop yields fall (harvest season, Q3–Q4 2026) → lower output than the market expects

- Food supply tightens (post-harvest) → grain, rice, and staple inventories shrink

- Food prices rise (lagged CPI impact) → the inflation the market didn’t price in arrives on schedule

This is not cyclical inflation. This is not a demand shock that the Fed can cool with a rate hike. This is structural inflation driven by a real, physical constraint on one of the most inelastic goods on earth: food. You cannot print more rice. You cannot stimulate your way to a better harvest.

And crucially — the data will look fine right now. Commodity desks will note that food CPI has not moved. Analysts will say the market is calm. That calm is the problem. The harvest hasn’t happened yet.

Who Gets Hit First

Not everyone feels this equally. The geography of vulnerability follows the fertilizer import map, and it skews heavily toward the countries least able to absorb it. India is already bidding urea at $935–959 per ton, roughly double two months ago. Bangladesh, Pakistan, and much of Sub-Saharan Africa run food expenditure ratios above 50% of household income; a 30–50% fertilizer input shock is not an abstraction for the people at the end of this supply chain — it is a decision about whether to plant at all. When farmers in import-dependent economies reduce application rates or skip a crop cycle, the deficit gets quietly written into soil that won’t talk back until harvest season.

Source: Bloomberg

The Inflation That Was Already Coming

We want to be precise about something: this is not a new worry for us. We first wrote about ammonia as a geopolitical weapon in early 2022, in “Rising Fertiliser and Food Prices: Who Will Be Spared?” — before most investors were treating it as anything other than a niche commodity story. The thesis then was that supply chain breakdown, energy crisis, and geopolitical tension had crystallised into a perfect storm for food prices, and that the effects would travel through the system far more slowly and durably than markets expected.

Later that year, when food prices briefly cooled and analysts declared the crisis over, we pushed back in “The End of the Decade of Plenty” blog back in November 2022. The FAO food price index had fallen 14.7% from its March peak, but the dollar had risen 21.5% over the same period, meaning most countries were actually paying more in local currency terms. Export bans were proliferating. The underlying supply-side pressures had not resolved; they had merely gone quiet. We said then: don’t mistake a pause for a resolution.

That lesson applies with full force today. The latest data from FAO ((Food and Agriculture Organization of the United Nations)) is already seeing Food Price Index rising for a second consecutive month, driven by energy related pressures from the Middle East conflict.

Averaged 128.5 points in March 2026, up 3.0 points from February

Source: FAO

What we are describing is not a cyclical event central banks can hike away. It is structural inflation — driven by real, physical constraints on the most inelastic thing on earth. You cannot print more rice. The Hormuz crisis will eventually ease and shipping lanes will reopen, but the harvest that didn’t happen won’t come back.

You cannot retroactively fertilize a field that went under-dosed in April. The consequences are already baked into the ground.

The question for investors isn’t whether this inflation arrives, it’s whether you’re positioned for a world where food prices reprice structurally and stay there. We’ve long believed the answer lies in owning the things scarcity makes more valuable and the kind of exposure to real assets that actually benefits when the fiction of infinite, frictionless abundance runs into a closed strait. The broader point is the same one we’ve been making since the decade of plenty ended: efficiency was the trade of the last era; resilience is the trade of this one.

In the film, (spoiler alert) humanity gets its Hail Mary — a one-in-a-billion miracle, executed by a lone astronaut and some extra-terrestrial help, arriving in the nick of time. Inspiring. Also not our base case.

What is our Hail Mary?

source: MGM

The real-world version of this story doesn’t end with a miracle. It ends with whoever read the data early enough being fine, and whoever assumed the world would stay frictionless being very surprised by their future grocery bill.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share