The Hawk With Clipped Wings: Why Kevin Warsh Is Stuck Between a Rock and a Hard Place

The Hawk With Clipped Wings: Why Kevin Warsh Is Stuck Between a Rock and a Hard Place

This week the Heyokha team is doing something deeply serious and analytical: booking tickets to a movie. Christopher Nolan’s “The Odyssey” lands in cinemas this week, with Matt Damon rowing his way home as the long-suffering Odysseus, and we are far more excited about it than grown professionals probably should admit.

There is one stretch of that voyage we will be watching for in particular.

Odysseus has to steer his ship through a narrow strait guarded on one side by Scylla, a six-headed monster bolted to a rock, and on the other by Charybdis, a whirlpool that swallows ships whole.

The cruel joke of the myth is that there is no clean way through. Sail toward the rock and the monster picks off your crew. Sail toward the whirlpool and you lose the whole ship. All a captain can really do is pick the less catastrophic option and keep narrating confidently so the crew doesn’t panic.

We bring this up because a modern captain is sailing that exact strait right now, and his name is Kevin Warsh.

A Magnificent Speech, and Then Nothing

There is a particular kind of theatre to a Fed chair’s first testimony to Congress, and on July 14 the newly installed Warsh delivered it beautifully.

He invoked the late Alan Greenspan. He spoke of the nation’s founding principles. And then, with the gravity of a man drawing a line in the sand, he vowed that the inflation surge of the last five years “will be a thing of the past.”

It is the kind of line that gets clipped and replayed. Tough. Hawkish. Reassuring, if you are the sort who lies awake worrying about the dollar in your pocket.

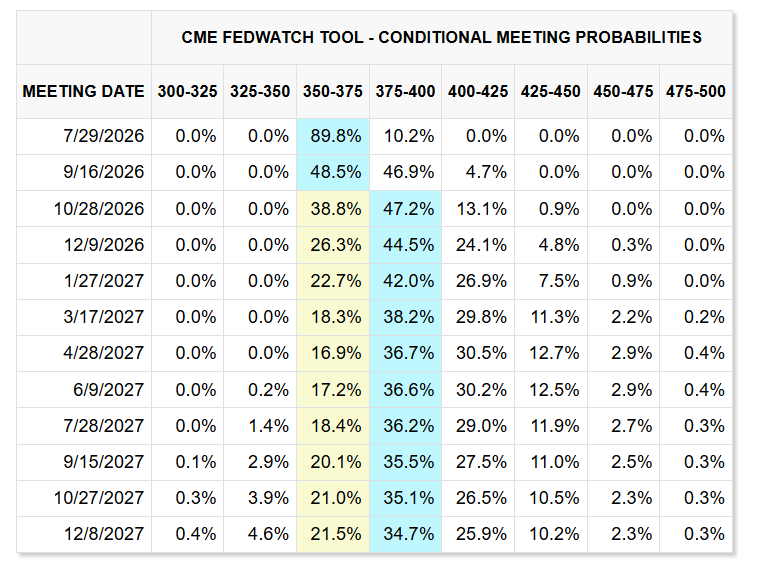

There was just one small detail. Having promised to vanquish inflation, Warsh’s committee had, a month earlier, held interest rates exactly where they found them, at a target range of 3.5% to 3.75%. No hike. Not even a threatened one. The sheriff rode into town, delivered a stirring speech about law and order, and then declined to load the gun.

How people are reacting to this – probabilities of a rate hike is now below 50%

Source: CME Group

This is not, we should say up front, a knock on the man. Warsh’s hawkish credentials are real. After 2008 he was among the loudest voices warning that quantitative easing, the Fed printing money to buy bonds, had gone too far. Say his name and the market hears discipline.

It duly marked gold down when he arrived, on the theory that the adults were back in charge. But there is a widening gap between what a famous hawk says and what a cornered central bank can actually do. In that gap sits the whole story.

Warsh is stuck between a rock and a hard place. The trouble is that he was stuck before he even sat down.

The Rock: You Must Sound Like Volcker

The rock is inflation, and it has not left the building. Warsh himself conceded that the latest cooler reading was “not mission accomplished.” Prices have been rising uncomfortably for years, households are exhausted by it, and a Fed chair who shrugged at inflation would be run out of Washington by lunchtime.

And “not mission accomplished” is doing a lot of quiet work in that sentence. June’s inflation number did come in cooler than almost anyone expected, at 3.5% for the year against the 3.8% the market had penciled in, down from 4.2% in May.

But lift the hood and the relief was almost entirely a swoon in energy prices. Petrol fell, and core inflation, the bit that strips out food and fuel, barely moved. That kind of good news has a short shelf life, and it may already be curdling. The US and Iran ceasefire has broken down, Tehran has again threatened to choke the Strait of Hormuz, the maritime tollbooth through which roughly a fifth of the world’s crude passes, and oil has leapt around 14% back toward $85 a barrel.

We walked through exactly why these chokepoints matter in our previous blog “Tollbooth at the end of the world”

Energy is the whole reason June looked tame. Energy is also the fastest route for July to look frightening. The rock, in other words, is not going anywhere.

So the rock demands a performance of toughness. It demands the Greenspan invocations, the “resolute commitment to price stability,” the promise that high inflation will become a museum exhibit. Every incentive Warsh has, reputational and political and personal, pushes him to sound like Paul Volcker, the chair who broke inflation’s back in the early 1980s by hiking rates into the stratosphere and cheerfully inducing a recession to do it.

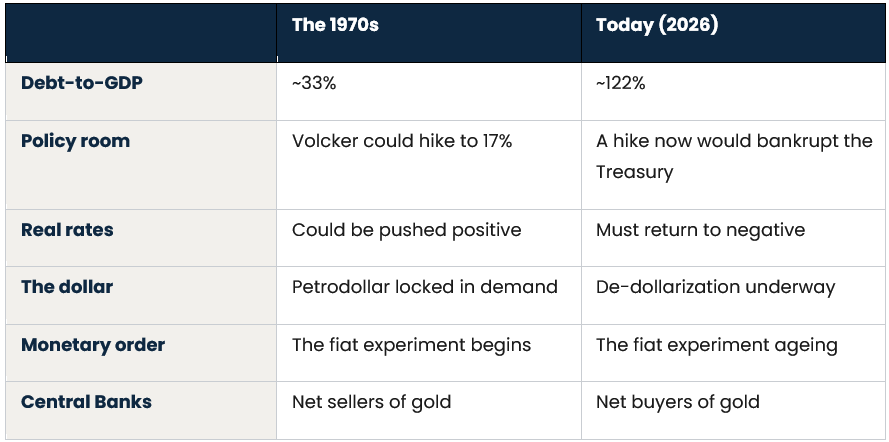

The catch is that Volcker could actually swing the hammer. When he took rates to nearly 20%, US federal debt was a svelte thing, around a third of the size of the economy. The government could absorb the pain because the government barely owed anything. Warsh has inherited the same hammer. What he has not inherited is Volcker’s arm.

The Hard Place: The Bill Nobody Can Pay

Which brings us to the whirlpool: the debt.

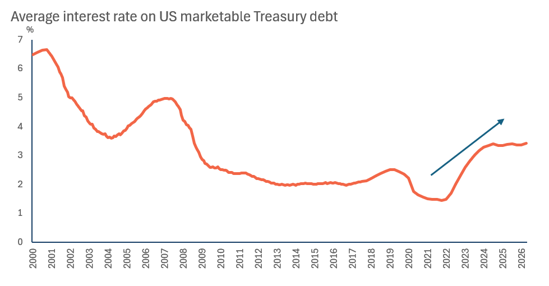

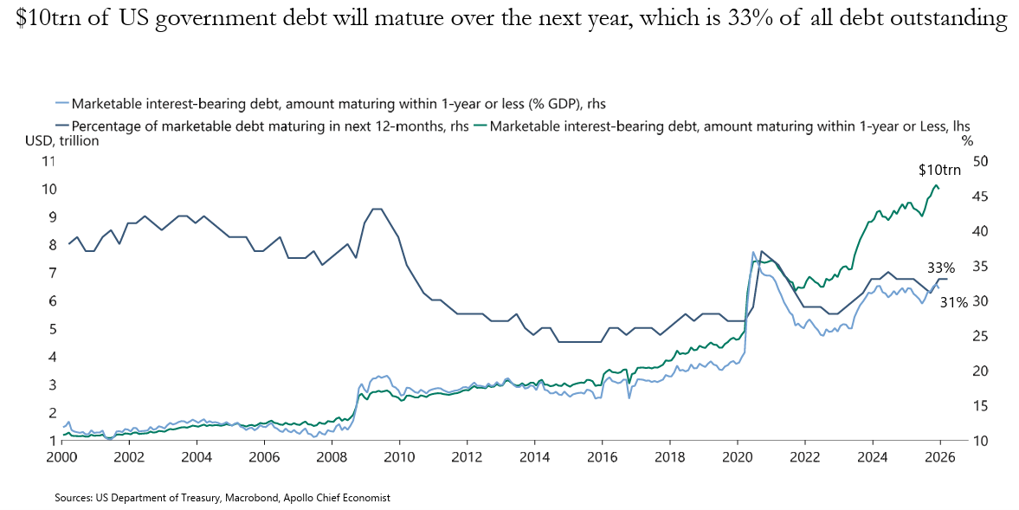

The United States now owes about $39.4 trillion, and this is the part that matters, that pile can only be serviced comfortably at low interest rates. Every percentage point Warsh would add to fight inflation lands directly on the government’s own interest bill, which is already one of the largest single lines in the federal budget.

Raise rates like Volcker and you do not just cool the economy. You detonate the Treasury’s finances.

The debt rolls over at higher interest rates

This is what economists call fiscal dominance, the polite term for the moment when the government’s borrowing needs quietly start steering monetary policy, rather than the other way around. The central bank stops being the disciplinarian and becomes the enabler, because the alternative is a debt crisis.

We laid out the full trajectory in “Banana Republic Yellen” and if anything it has accelerated: once the numbers get big enough, the printing press stops being an emergency tool and becomes a permanent fixture.

Here is the truly awkward bit for our hawk. The tightening he is famous for wanting has already been tried, and it already broke.

Quantitative tightening, the process of shrinking the Fed’s balance sheet by letting its hoard of bonds roll off and draining money back out of the system, quietly died on December 1, 2025. The Fed had spent two years trying to pull cash out.

But when bank reserves got thin enough, the repo market, the overnight plumbing where banks fund themselves, started to groan, and the Fed slammed the process into park. The balance sheet froze at roughly $6.6 trillion, barely half the pandemic bloat unwound, and the Fed now expects it to start growing again as banks come asking for more reserves.

Read that twice. The system tried to run on less money and could not.

The most hawkish maneuver in the toolkit was attempted, and the market seized up like an engine run dry. So when investors cheer a “hawk” taking over, they are cheering a project that already hit a physical wall, before Warsh even arrived. He is inheriting a ship whose oars only pull in one direction.

When You Cannot Move, Move the Walls

Here is where it gets interesting, and where you can watch a genuinely clever man work an impossible problem. If you are wedged between a rock and a whirlpool and you cannot move toward either, there is exactly one move left: change the shape of the strait.

Warsh has wasted no time. On day one he declined to submit his own “dot” to the Fed’s dot-plot, the chart where each official pencils in where they think rates are heading, breaking a tradition that runs back nearly two decades. The effect, whatever the intent, is a central bank that no longer tells you which way it is leaning. It is harder to be caught missing a target you have stopped announcing.

With Warsh being tight-lipped on his personal guidance, maybe this guy will be out of a job?

Then there is the small matter of the scoreboard itself. Warsh has signaled openness to measuring inflation with a “trimmed-mean” gauge, which strips out the categories that move the most. That is another way to say it strips out precisely the alarming bits. It is a bit like declaring yourself on a strict diet after quietly deciding that dessert no longer counts.

And for the grand finale, he has convened five task forces to “start from first principles” and rethink how the Fed does nearly everything: communications, the balance sheet, the data, and the inflation framework itself.

The one on productivity, jobs and AI he handed to Marc Andreessen. Yes, that Andreessen from Andreessen Horowitz. He is the venture capitalist whose firm is one of the most committed backers of the AI boom.

Ask the biggest AI believer in the country whether AI will lift productivity enough to let the Fed cut rates without stoking inflation, and you can probably guess the verdict before the task force even convenes. Warsh has already floated exactly this hope: that the AI build-out will do his tightening for him, letting rates fall without prices rising.

But will AI grow fast enough to get out of the debt? We are not convinced yet given a third of the debt needs to be refinanced

None of these are the acts of a man assembling the brutal, positive-real-rate regime that would actually threaten inflation, or gold. They are the acts of a captain quietly widening the strait so that whatever the current forces him to do next can still be called seamanship.

Back to the perilous journey

Which returns us to Odysseus, and to why the myth is such a good map of the moment.

The whole point of Scylla and Charybdis is that there was no good option, only the least-bad one and a lot of brave talk to get the crew through it. Warsh is navigating the same waters.

On one side, the monster of inflation, which he cannot ignore. On the other, the whirlpool of the debt, which he cannot afford to feed with high rates. He cannot steer hard toward either. So he does the only thing a skilled captain can: he keeps up a confident narration while letting the current carry the ship where it was always going to go.

That is why we think the market has the story upside down. It read the arrival of a celebrated hawk as proof the Fed is serious about discipline. But the hawkishness is a costume the debt cannot afford to wear for real.

Source: CNBC

Appoint the most famous critic of money-printing in the country and the outcome barely changes, because the system has already shown it cannot run on less money. The reputation is not a constraint. It is cover.

This is precisely why, quietly, the people whose job is to hold the world’s reserves keep reaching for the one asset that does not depend on anybody’s promises. Central banks have bought around 1,000 tonnes of gold a year over the past four years, double the previous decade’s pace. Even Tether, a company whose entire product is the digital dollar, has been stacking bullion.

When the people closest to the printing press are the ones buying the thing that cannot be printed, it is worth asking what they know.

Odysseus made it home in the end, but not by defeating the monster or the whirlpool. He survived by accepting that the strait could not be beaten, only crossed, and by being honest with himself about the losses along the way. A Fed chair can promise to make inflation a thing of the past. He can invoke Greenspan, quote the Framers, and mean every word. But talk is a policy tool with a very short half-life. The debt is the thing that actually sets the speed limit, and it does not care how hawkish anyone sounds.

Here in Heyokha, we know where we stand. Enjoy the movie.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share

This week the Heyokha team is doing something deeply serious and analytical: booking tickets to a movie. Christopher Nolan’s “The Odyssey” lands in cinemas this week, with Matt Damon rowing his way home as the long-suffering Odysseus, and we are far more excited about it than grown professionals probably should admit.

There is one stretch of that voyage we will be watching for in particular.

Odysseus has to steer his ship through a narrow strait guarded on one side by Scylla, a six-headed monster bolted to a rock, and on the other by Charybdis, a whirlpool that swallows ships whole.

The cruel joke of the myth is that there is no clean way through. Sail toward the rock and the monster picks off your crew. Sail toward the whirlpool and you lose the whole ship. All a captain can really do is pick the less catastrophic option and keep narrating confidently so the crew doesn’t panic.

We bring this up because a modern captain is sailing that exact strait right now, and his name is Kevin Warsh.

A Magnificent Speech, and Then Nothing

There is a particular kind of theatre to a Fed chair’s first testimony to Congress, and on July 14 the newly installed Warsh delivered it beautifully.

He invoked the late Alan Greenspan. He spoke of the nation’s founding principles. And then, with the gravity of a man drawing a line in the sand, he vowed that the inflation surge of the last five years “will be a thing of the past.”

It is the kind of line that gets clipped and replayed. Tough. Hawkish. Reassuring, if you are the sort who lies awake worrying about the dollar in your pocket.

There was just one small detail. Having promised to vanquish inflation, Warsh’s committee had, a month earlier, held interest rates exactly where they found them, at a target range of 3.5% to 3.75%. No hike. Not even a threatened one. The sheriff rode into town, delivered a stirring speech about law and order, and then declined to load the gun.

How people are reacting to this – probabilities of a rate hike is now below 50%

Source: CME Group

This is not, we should say up front, a knock on the man. Warsh’s hawkish credentials are real. After 2008 he was among the loudest voices warning that quantitative easing, the Fed printing money to buy bonds, had gone too far. Say his name and the market hears discipline.

It duly marked gold down when he arrived, on the theory that the adults were back in charge. But there is a widening gap between what a famous hawk says and what a cornered central bank can actually do. In that gap sits the whole story.

Warsh is stuck between a rock and a hard place. The trouble is that he was stuck before he even sat down.

The Rock: You Must Sound Like Volcker

The rock is inflation, and it has not left the building. Warsh himself conceded that the latest cooler reading was “not mission accomplished.” Prices have been rising uncomfortably for years, households are exhausted by it, and a Fed chair who shrugged at inflation would be run out of Washington by lunchtime.

And “not mission accomplished” is doing a lot of quiet work in that sentence. June’s inflation number did come in cooler than almost anyone expected, at 3.5% for the year against the 3.8% the market had penciled in, down from 4.2% in May.

But lift the hood and the relief was almost entirely a swoon in energy prices. Petrol fell, and core inflation, the bit that strips out food and fuel, barely moved. That kind of good news has a short shelf life, and it may already be curdling. The US and Iran ceasefire has broken down, Tehran has again threatened to choke the Strait of Hormuz, the maritime tollbooth through which roughly a fifth of the world’s crude passes, and oil has leapt around 14% back toward $85 a barrel.

We walked through exactly why these chokepoints matter in our previous blog “Tollbooth at the end of the world”

Energy is the whole reason June looked tame. Energy is also the fastest route for July to look frightening. The rock, in other words, is not going anywhere.

So the rock demands a performance of toughness. It demands the Greenspan invocations, the “resolute commitment to price stability,” the promise that high inflation will become a museum exhibit. Every incentive Warsh has, reputational and political and personal, pushes him to sound like Paul Volcker, the chair who broke inflation’s back in the early 1980s by hiking rates into the stratosphere and cheerfully inducing a recession to do it.

The catch is that Volcker could actually swing the hammer. When he took rates to nearly 20%, US federal debt was a svelte thing, around a third of the size of the economy. The government could absorb the pain because the government barely owed anything. Warsh has inherited the same hammer. What he has not inherited is Volcker’s arm.

The Hard Place: The Bill Nobody Can Pay

Which brings us to the whirlpool: the debt.

The United States now owes about $39.4 trillion, and this is the part that matters, that pile can only be serviced comfortably at low interest rates. Every percentage point Warsh would add to fight inflation lands directly on the government’s own interest bill, which is already one of the largest single lines in the federal budget.

Raise rates like Volcker and you do not just cool the economy. You detonate the Treasury’s finances.

The debt rolls over at higher interest rates

This is what economists call fiscal dominance, the polite term for the moment when the government’s borrowing needs quietly start steering monetary policy, rather than the other way around. The central bank stops being the disciplinarian and becomes the enabler, because the alternative is a debt crisis.

We laid out the full trajectory in “Banana Republic Yellen” and if anything it has accelerated: once the numbers get big enough, the printing press stops being an emergency tool and becomes a permanent fixture.

Here is the truly awkward bit for our hawk. The tightening he is famous for wanting has already been tried, and it already broke.

Quantitative tightening, the process of shrinking the Fed’s balance sheet by letting its hoard of bonds roll off and draining money back out of the system, quietly died on December 1, 2025. The Fed had spent two years trying to pull cash out.

But when bank reserves got thin enough, the repo market, the overnight plumbing where banks fund themselves, started to groan, and the Fed slammed the process into park. The balance sheet froze at roughly $6.6 trillion, barely half the pandemic bloat unwound, and the Fed now expects it to start growing again as banks come asking for more reserves.

Read that twice. The system tried to run on less money and could not.

The most hawkish maneuver in the toolkit was attempted, and the market seized up like an engine run dry. So when investors cheer a “hawk” taking over, they are cheering a project that already hit a physical wall, before Warsh even arrived. He is inheriting a ship whose oars only pull in one direction.

When You Cannot Move, Move the Walls

Here is where it gets interesting, and where you can watch a genuinely clever man work an impossible problem. If you are wedged between a rock and a whirlpool and you cannot move toward either, there is exactly one move left: change the shape of the strait.

Warsh has wasted no time. On day one he declined to submit his own “dot” to the Fed’s dot-plot, the chart where each official pencils in where they think rates are heading, breaking a tradition that runs back nearly two decades. The effect, whatever the intent, is a central bank that no longer tells you which way it is leaning. It is harder to be caught missing a target you have stopped announcing.

With Warsh being tight-lipped on his personal guidance, maybe this guy will be out of a job?

Then there is the small matter of the scoreboard itself. Warsh has signaled openness to measuring inflation with a “trimmed-mean” gauge, which strips out the categories that move the most. That is another way to say it strips out precisely the alarming bits. It is a bit like declaring yourself on a strict diet after quietly deciding that dessert no longer counts.

And for the grand finale, he has convened five task forces to “start from first principles” and rethink how the Fed does nearly everything: communications, the balance sheet, the data, and the inflation framework itself.

The one on productivity, jobs and AI he handed to Marc Andreessen. Yes, that Andreessen from Andreessen Horowitz. He is the venture capitalist whose firm is one of the most committed backers of the AI boom.

Ask the biggest AI believer in the country whether AI will lift productivity enough to let the Fed cut rates without stoking inflation, and you can probably guess the verdict before the task force even convenes. Warsh has already floated exactly this hope: that the AI build-out will do his tightening for him, letting rates fall without prices rising.

But will AI grow fast enough to get out of the debt? We are not convinced yet given a third of the debt needs to be refinanced

None of these are the acts of a man assembling the brutal, positive-real-rate regime that would actually threaten inflation, or gold. They are the acts of a captain quietly widening the strait so that whatever the current forces him to do next can still be called seamanship.

Back to the perilous journey

Which returns us to Odysseus, and to why the myth is such a good map of the moment.

The whole point of Scylla and Charybdis is that there was no good option, only the least-bad one and a lot of brave talk to get the crew through it. Warsh is navigating the same waters.

On one side, the monster of inflation, which he cannot ignore. On the other, the whirlpool of the debt, which he cannot afford to feed with high rates. He cannot steer hard toward either. So he does the only thing a skilled captain can: he keeps up a confident narration while letting the current carry the ship where it was always going to go.

That is why we think the market has the story upside down. It read the arrival of a celebrated hawk as proof the Fed is serious about discipline. But the hawkishness is a costume the debt cannot afford to wear for real.

Source: CNBC

Appoint the most famous critic of money-printing in the country and the outcome barely changes, because the system has already shown it cannot run on less money. The reputation is not a constraint. It is cover.

This is precisely why, quietly, the people whose job is to hold the world’s reserves keep reaching for the one asset that does not depend on anybody’s promises. Central banks have bought around 1,000 tonnes of gold a year over the past four years, double the previous decade’s pace. Even Tether, a company whose entire product is the digital dollar, has been stacking bullion.

When the people closest to the printing press are the ones buying the thing that cannot be printed, it is worth asking what they know.

Odysseus made it home in the end, but not by defeating the monster or the whirlpool. He survived by accepting that the strait could not be beaten, only crossed, and by being honest with himself about the losses along the way. A Fed chair can promise to make inflation a thing of the past. He can invoke Greenspan, quote the Framers, and mean every word. But talk is a policy tool with a very short half-life. The debt is the thing that actually sets the speed limit, and it does not care how hawkish anyone sounds.

Here in Heyokha, we know where we stand. Enjoy the movie.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share