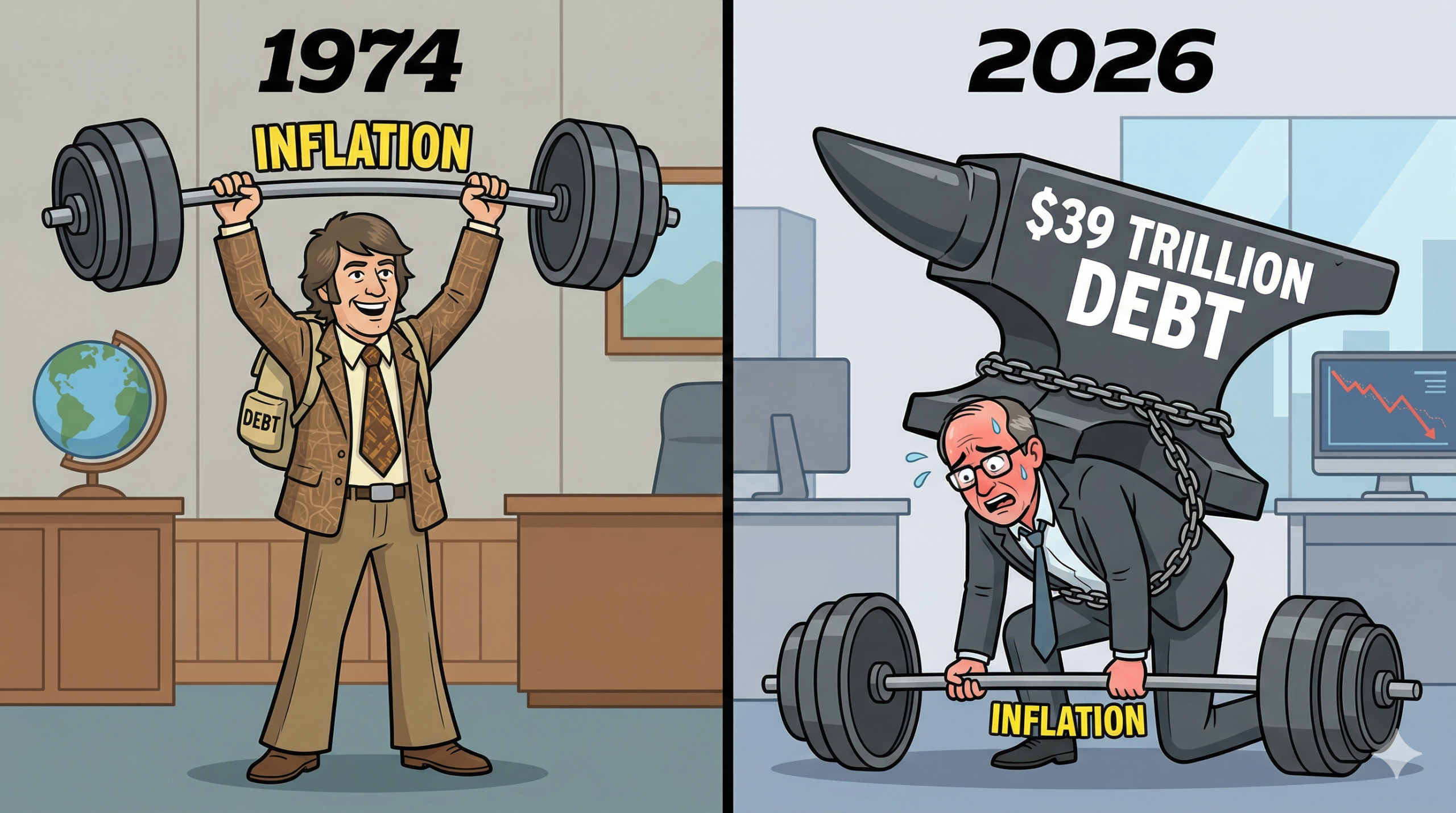

Last week’s post on Yellen left us turning over a question. Has central bank independence ever been tested like this before? Are there moments in history we should be reading our own moment against?

It is worth pausing for a sentence on what we mean. Central bank independence is the working assumption that the people who set interest rates can do so without being told what to do by the people who issue debt.

The Fed has had it, in modern form, since Paul Volcker’s 1979 appointment; most of the rest of the developed world adopted some version of it over the following two decades. Whether that assumption survives the next few years is the question hanging over markets right now.

Our reading is that the answer to the question we started with is yes. Central bank independence has been tested before, on at least four separate occasions in the last century, and the pattern is suggestive: they cluster, with surprising consistency, around wars.

The institution looks, on closer inspection, like a peacetime convention. We seem to be entering not one war but three at once.

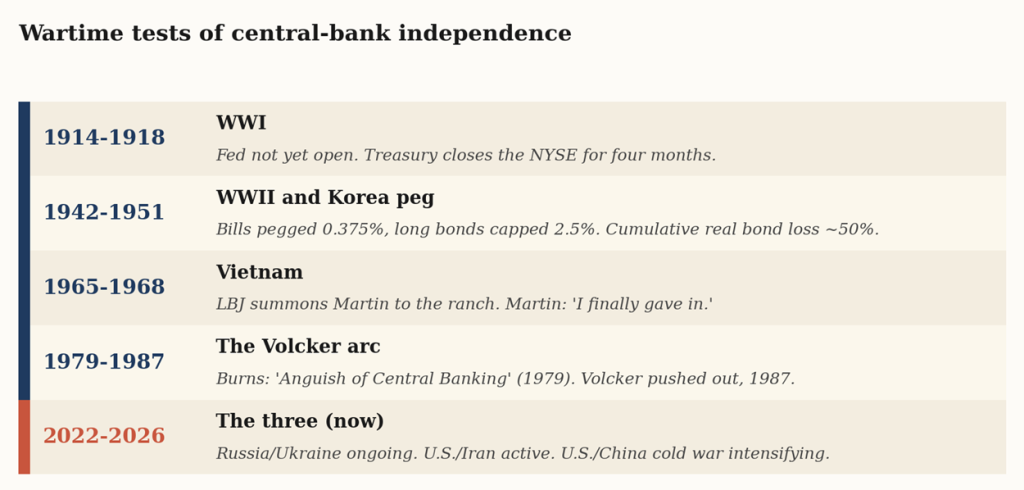

A century of wartime tests of central-bank independence.

Source: Heyokha Research

The pattern: one war tends to be enough

The record is consistent enough to be suggestive. Central banks fold to fiscal needs when the state declares a real emergency. Not always cleanly, not always quickly, but reliably enough to look like a rule.

In late July 1914, with WWI breaking out, U.S. Treasury Secretary William McAdoo asked the New York Stock Exchange to close, to stop foreign liquidations of American assets. It stayed closed, in some form, for four months. The Federal Reserve had been signed into law eight months earlier and would not actually open its doors until November. Independence was an idea. War was the test.

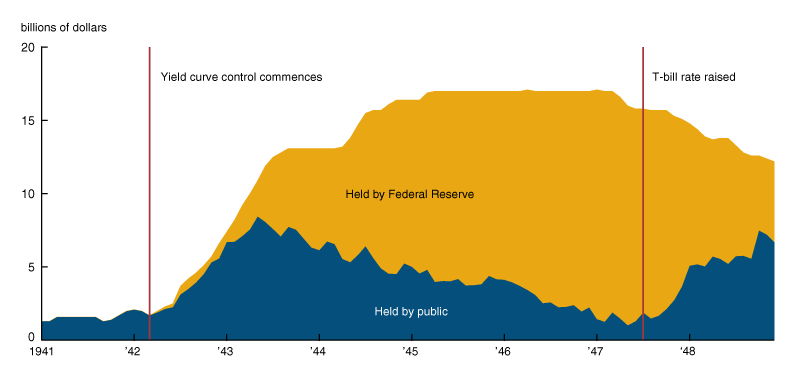

From April 1942 through March 1951, at the Treasury’s request, the Fed pegged short Treasury bills at 0.375% and capped long Treasury yields at 2.5%. CPI peaked at 19.7% YoY in March 1947, making the real long-bond yield that month roughly minus seventeen percent. An investor who held a 30-year Treasury through the peg lost something close to half their purchasing power. The Fed only got its independence back via the 1951 Treasury-Fed Accord, six years after the war had ended. The independence of an institution and the patience of its bondholders, it turns out, are not the same thing.

The hoarding of T-Bills to fund the war debt

Source: Federal Reserve Bank of Chicago, Board of Governors of the Federal Reserve System (1976).

In December 1965, William McChesney Martin’s Fed raised the discount rate during Vietnam financing. Two days later, LBJ summoned him to the Texas ranch (where the President was recovering from gallbladder surgery) and, by most accounts, physically pushed him around the room with the line: Martin, my boys are dying in Vietnam, and you won’t print the money I need. Martin held the line on the rate decision in public. Years later, he confessed to a friend: To my everlasting shame, I finally gave in to him.

The institution had no protection. The man’s stubbornness did, briefly.

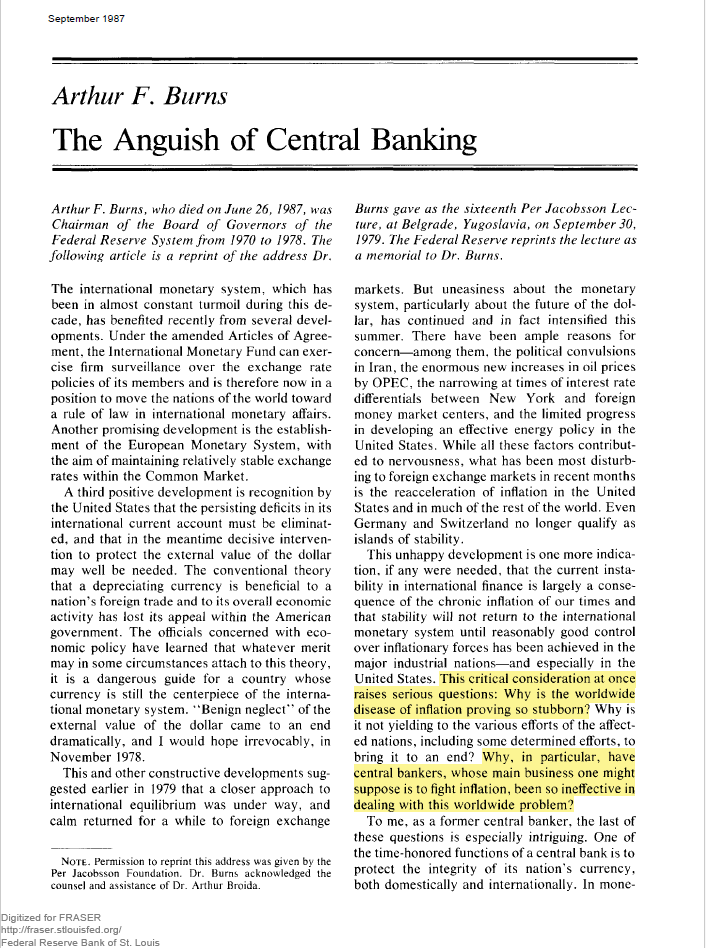

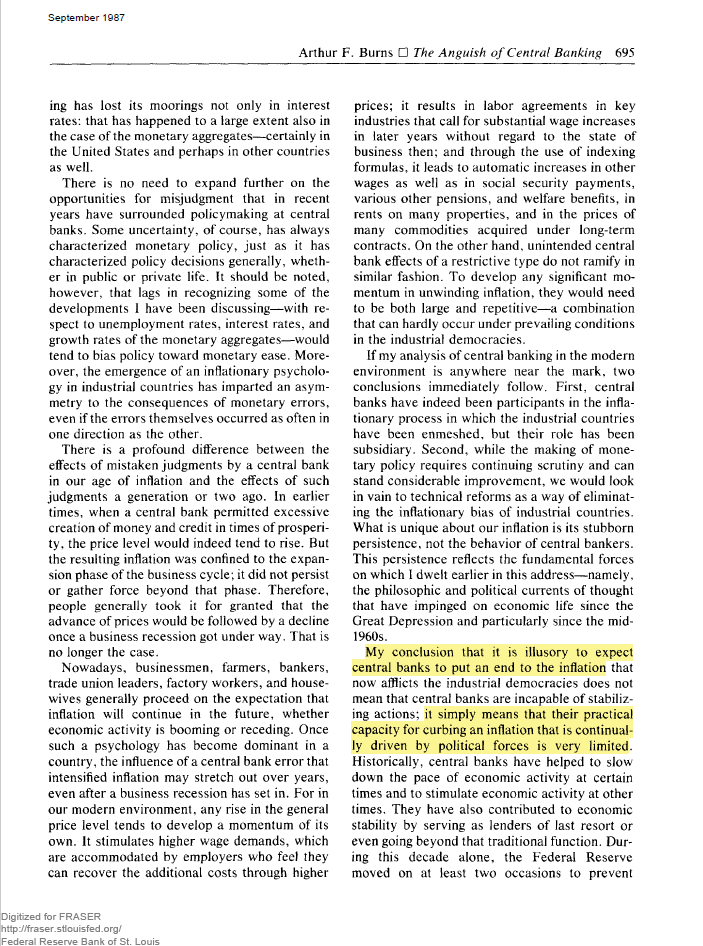

In September 1979, Arthur Burns gave the Per Jacobsson lecture in Belgrade titled “The Anguish of Central Banking.” It read less as theory than as confession: central bankers who try to defy political pressure during a national emergency tend to lose, because the emergency is real, the public sides with the government, and the central bank has no political constituency of its own. Volcker, the figure who briefly seemed to refute him, was being pressed by Reagan’s Treasury to ease by 1986 and was eased into retirement in 1987. The exception, it turns out, also tends to prove the pattern.

source: Chung-Hua Institution for Economic Research

So the pattern, viewed from sufficient height: one genuine national emergency tends to override the convention. We are currently looking at three.

The dashboard, this spring

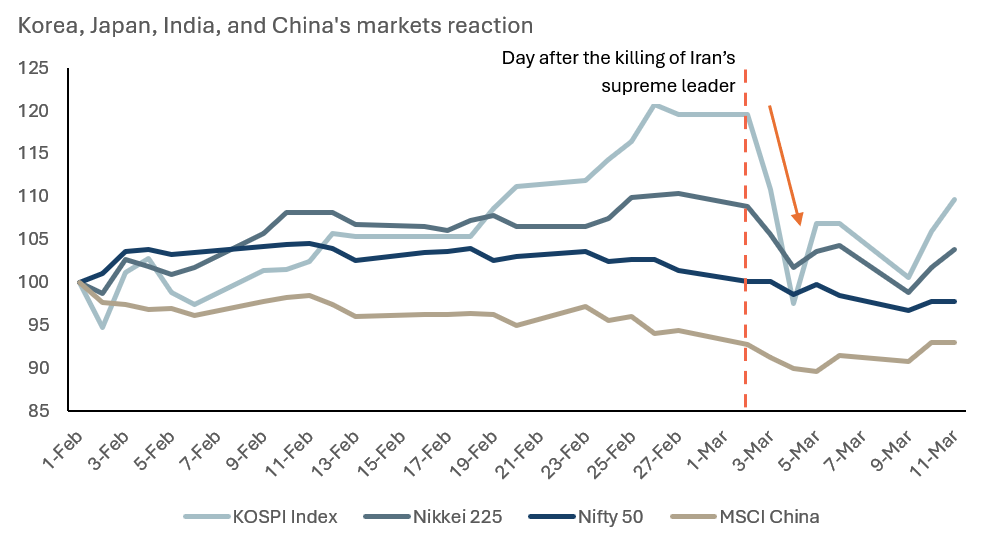

The hot war. The U.S. has been in active engagement with Iran since early February. Joint U.S.-Israeli strikes on 28 February formally opened what the press is now calling the 2026 Iran war. Tankers in and around the Strait of Hormuz are being seized; Iranian drones are being shot down over the Gulf. With Iran reportedly negotiating with China for hypersonic anti-ship missiles, the kind designed to neutralise U.S. naval power in the region, the contest looks less like a regional skirmish than a U.S.-China proxy with Iran as the contested ground.

The cold war. No soldiers shooting; every other lever of state power being pulled. Tariff threats on countries arming Iran. Secondary-sanction letters to Chinese banks. Beijing’s recent 18-point regulation giving authorities the power to investigate and bar foreign-company executives from leaving the country. The arc of containment is being drawn in real time, and capital is being trapped on both sides of it.

The one still ongoing. Russia-Ukraine, now in its fifth year. The EU adopted its 20th sanctions package on 23 April. There is no ceasefire. The war has settled into the kind of grinding precedent that quietly redirects European savings into national defence, which is a precedent in its own right.

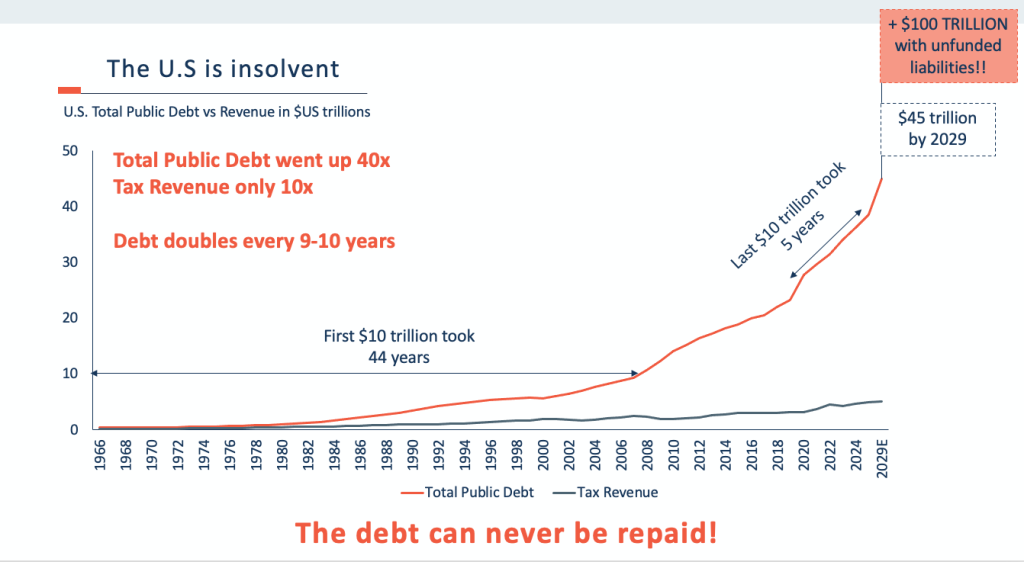

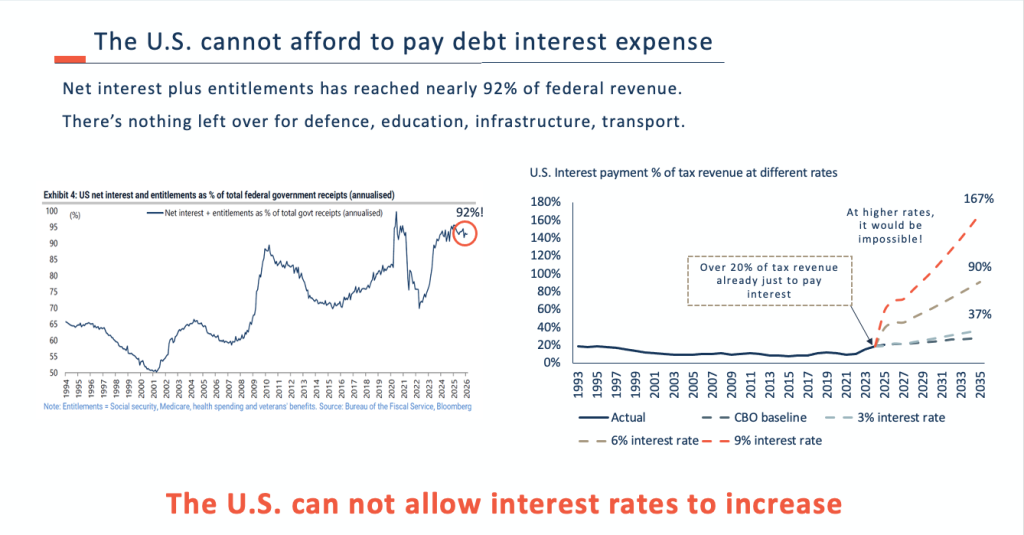

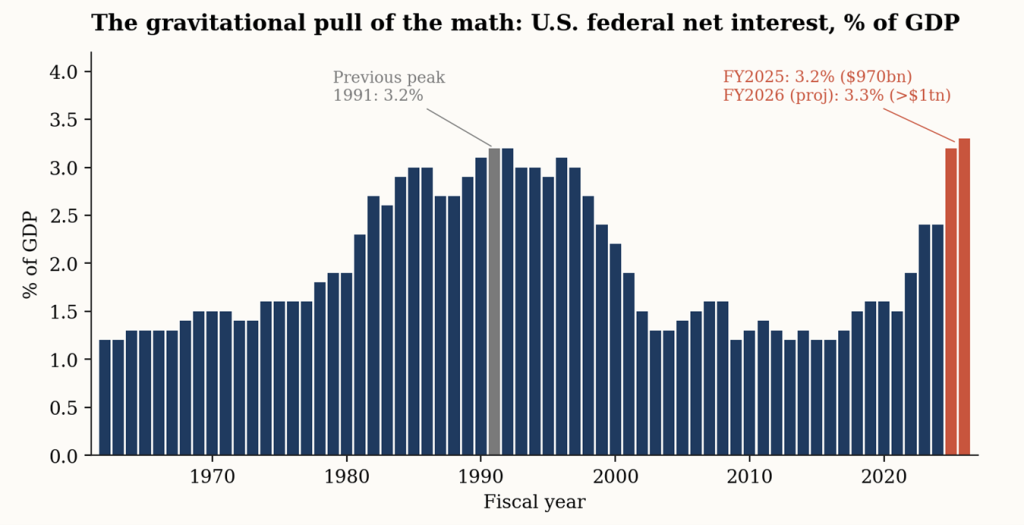

Each alone might be enough to override the convention. Stacked, they’re harder to argue against. We are also stacking them on top of a fiscal position that didn’t exist in 1942 or 1965. U.S. net interest expense reached $970 billion in FY2025 (3.2% of GDP) and is projected to clear $1 trillion in FY2026, already the second-largest line in the federal budget, ahead of defence and behind only Social Security. The temptation to lean on the Fed is not a personality trait of the current administration. It is the gravitational pull of the math.

U.S. federal net interest expense as share of GDP, with FY2026 projection.

Source: CBO, U.S. Office of Management and Budget.

What Burns was really saying

Burns’s anguish was about the gap between the model an economist studies and the institution an economist actually runs. The model assumes the central bank stands apart. The institution does not. It funds whatever the state needs funded when the state declares an emergency. The freedom, mostly, is in how: in the tone, the framing, the press conference.

Excerpts from Arthur Burns’ lecture (former Fed chair in 1970-1978 who is known to let inflation run rampant). This lecture is essentially his defense on Fed’s independence being difficult to uphold

Source: Federal Reserve Bank of St Louis

In practice, if our reading is right, the playbook will look fairly familiar. Powell will signal it one way. Whoever replaces Powell will signal it more quietly. The substance will be similar: rates capped relative to inflation, captive buyers of U.S. bonds manufactured, the debt stock eroded in real terms over the next decade. The wars get paid for, slowly, by whoever’s savings sit in nominal currency or government debt.

Markets keep treating each new data point (a rate decision, a Treasury auction, a Powell press conference) as a referendum on whether the regime is changing. We understand the appeal: watching the data point is something you can do, and feels like agency. Our suspicion, offered in the spirit it deserves, is that the referendum has been held. What’s left is the speed at which bond, equity and currency markets adjust to the new state.

If that’s roughly right, and we hold it the way one ought to hold any reading of an ongoing event, the implications are the ones we’ve been quietly writing about for years. Gold, owned for the boring decades and not just the loud ones. Real assets with pricing power. Some non-USD exposure, since this is, eventually, a story about the unit of account. A polite skepticism toward any narrative that quietly assumes a developed-world central bank will choose inflation control over fiscal accommodation in this environment.

That choice was probably always going to be made for them. One war, the record suggests, is already tough enough. We repeat again dear readers – we are in three. It will be near impossible to have a choice.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share

Last week’s post on Yellen left us turning over a question. Has central bank independence ever been tested like this before? Are there moments in history we should be reading our own moment against?

It is worth pausing for a sentence on what we mean. Central bank independence is the working assumption that the people who set interest rates can do so without being told what to do by the people who issue debt.

The Fed has had it, in modern form, since Paul Volcker’s 1979 appointment; most of the rest of the developed world adopted some version of it over the following two decades. Whether that assumption survives the next few years is the question hanging over markets right now.

Our reading is that the answer to the question we started with is yes. Central bank independence has been tested before, on at least four separate occasions in the last century, and the pattern is suggestive: they cluster, with surprising consistency, around wars.

The institution looks, on closer inspection, like a peacetime convention. We seem to be entering not one war but three at once.

A century of wartime tests of central-bank independence.

Source: Heyokha Research

The pattern: one war tends to be enough

The record is consistent enough to be suggestive. Central banks fold to fiscal needs when the state declares a real emergency. Not always cleanly, not always quickly, but reliably enough to look like a rule.

In late July 1914, with WWI breaking out, U.S. Treasury Secretary William McAdoo asked the New York Stock Exchange to close, to stop foreign liquidations of American assets. It stayed closed, in some form, for four months. The Federal Reserve had been signed into law eight months earlier and would not actually open its doors until November. Independence was an idea. War was the test.

From April 1942 through March 1951, at the Treasury’s request, the Fed pegged short Treasury bills at 0.375% and capped long Treasury yields at 2.5%. CPI peaked at 19.7% YoY in March 1947, making the real long-bond yield that month roughly minus seventeen percent. An investor who held a 30-year Treasury through the peg lost something close to half their purchasing power. The Fed only got its independence back via the 1951 Treasury-Fed Accord, six years after the war had ended. The independence of an institution and the patience of its bondholders, it turns out, are not the same thing.

The hoarding of T-Bills to fund the war debt

Source: Federal Reserve Bank of Chicago, Board of Governors of the Federal Reserve System (1976).

In December 1965, William McChesney Martin’s Fed raised the discount rate during Vietnam financing. Two days later, LBJ summoned him to the Texas ranch (where the President was recovering from gallbladder surgery) and, by most accounts, physically pushed him around the room with the line: Martin, my boys are dying in Vietnam, and you won’t print the money I need. Martin held the line on the rate decision in public. Years later, he confessed to a friend: To my everlasting shame, I finally gave in to him.

The institution had no protection. The man’s stubbornness did, briefly.

In September 1979, Arthur Burns gave the Per Jacobsson lecture in Belgrade titled “The Anguish of Central Banking.” It read less as theory than as confession: central bankers who try to defy political pressure during a national emergency tend to lose, because the emergency is real, the public sides with the government, and the central bank has no political constituency of its own. Volcker, the figure who briefly seemed to refute him, was being pressed by Reagan’s Treasury to ease by 1986 and was eased into retirement in 1987. The exception, it turns out, also tends to prove the pattern.

source: Chung-Hua Institution for Economic Research

So the pattern, viewed from sufficient height: one genuine national emergency tends to override the convention. We are currently looking at three.

The dashboard, this spring

The hot war. The U.S. has been in active engagement with Iran since early February. Joint U.S.-Israeli strikes on 28 February formally opened what the press is now calling the 2026 Iran war. Tankers in and around the Strait of Hormuz are being seized; Iranian drones are being shot down over the Gulf. With Iran reportedly negotiating with China for hypersonic anti-ship missiles, the kind designed to neutralise U.S. naval power in the region, the contest looks less like a regional skirmish than a U.S.-China proxy with Iran as the contested ground.

The cold war. No soldiers shooting; every other lever of state power being pulled. Tariff threats on countries arming Iran. Secondary-sanction letters to Chinese banks. Beijing’s recent 18-point regulation giving authorities the power to investigate and bar foreign-company executives from leaving the country. The arc of containment is being drawn in real time, and capital is being trapped on both sides of it.

The one still ongoing. Russia-Ukraine, now in its fifth year. The EU adopted its 20th sanctions package on 23 April. There is no ceasefire. The war has settled into the kind of grinding precedent that quietly redirects European savings into national defence, which is a precedent in its own right.

Each alone might be enough to override the convention. Stacked, they’re harder to argue against. We are also stacking them on top of a fiscal position that didn’t exist in 1942 or 1965. U.S. net interest expense reached $970 billion in FY2025 (3.2% of GDP) and is projected to clear $1 trillion in FY2026, already the second-largest line in the federal budget, ahead of defence and behind only Social Security. The temptation to lean on the Fed is not a personality trait of the current administration. It is the gravitational pull of the math.

U.S. federal net interest expense as share of GDP, with FY2026 projection.

Source: CBO, U.S. Office of Management and Budget.

What Burns was really saying

Burns’s anguish was about the gap between the model an economist studies and the institution an economist actually runs. The model assumes the central bank stands apart. The institution does not. It funds whatever the state needs funded when the state declares an emergency. The freedom, mostly, is in how: in the tone, the framing, the press conference.

Excerpts from Arthur Burns’ lecture (former Fed chair in 1970-1978 who is known to let inflation run rampant). This lecture is essentially his defense on Fed’s independence being difficult to uphold

Source: Federal Reserve Bank of St Louis

In practice, if our reading is right, the playbook will look fairly familiar. Powell will signal it one way. Whoever replaces Powell will signal it more quietly. The substance will be similar: rates capped relative to inflation, captive buyers of U.S. bonds manufactured, the debt stock eroded in real terms over the next decade. The wars get paid for, slowly, by whoever’s savings sit in nominal currency or government debt.

Markets keep treating each new data point (a rate decision, a Treasury auction, a Powell press conference) as a referendum on whether the regime is changing. We understand the appeal: watching the data point is something you can do, and feels like agency. Our suspicion, offered in the spirit it deserves, is that the referendum has been held. What’s left is the speed at which bond, equity and currency markets adjust to the new state.

If that’s roughly right, and we hold it the way one ought to hold any reading of an ongoing event, the implications are the ones we’ve been quietly writing about for years. Gold, owned for the boring decades and not just the loud ones. Real assets with pricing power. Some non-USD exposure, since this is, eventually, a story about the unit of account. A polite skepticism toward any narrative that quietly assumes a developed-world central bank will choose inflation control over fiscal accommodation in this environment.

That choice was probably always going to be made for them. One war, the record suggests, is already tough enough. We repeat again dear readers – we are in three. It will be near impossible to have a choice.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share

Source: Heyokha Research

Source: Heyokha Research Now it’s higher than WW2!

Now it’s higher than WW2! Source: Heyokha Research

Source: Heyokha Research