Amidst a surge of negative headlines in the Western press, Indonesia’s nickel revolution is transforming the global EV supply chain. This comprehensive report delves into whether these criticisms hold any truth or if they are simply tactics by competitors to undermine Indonesia’s growth. By examining advanced technologies like High-Pressure Acid Leach (HPAL) and highlighting significant investments from both Chinese and Western companies, we uncover the real story of how Indonesia is not only meeting global nickel demand but leading in sustainable mining practices. Dive in to explore the facts and debunk the myths surrounding this pivotal industry shift.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labor.

Share

Published: Aug 01 2024

Amidst a surge of negative headlines in the Western press, Indonesia’s nickel revolution is transforming the global EV supply chain. This comprehensive report delves into whether these criticisms hold any truth or if they are simply tactics by competitors to undermine Indonesia’s growth. By examining advanced technologies like High-Pressure Acid Leach (HPAL) and highlighting significant investments from both Chinese and Western companies, we uncover the real story of how Indonesia is not only meeting global nickel demand but leading in sustainable mining practices. Dive in to explore the facts and debunk the myths surrounding this pivotal industry shift.

Indonesia’s journey towards an energy transition, particularly with the adoption of electric vehicles (EVs), has been met with a fair share of skepticism. Concerns about the availability of charging stations, the cost-efficiency of EVs, and the overall practicality of long-distance travel in an EV have loomed large. However, our recent road round trip from Jakarta to Semarang which is around 400km one way pleasantly surprised us, casting away many of those doubts. Here’s a recount of our electrifying adventure that proved the naysayers wrong.

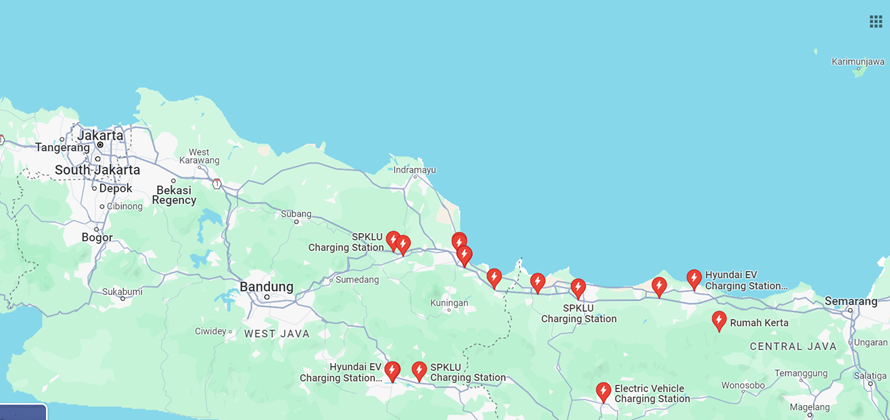

Charging stations aplenty from Jakarta to Semarang

Bird eye view of several charging stations by the National Electric Company along the toll roads

Starting at 5:30am from our office with a fully charged battery and a sense of adventure, we were ready to begin. Mind you, this was our first time taking our EV, a Hyundai Ioniq 5, to a trip this far and long so we were cautiously optimistic. Leaving at the break of dawn has its perks namely avoiding the notorious Jakarta traffic jam. Whizzing past several rest areas, we were able to spot almost if not all had the electric sign logos on their billboards showing EV charging station availability. Fortune was on our side.

With rest areas aplenty by the toll roads, our first leg of the journey took us to the midpoint at the KM 228A rest area. We covered 243 km in under 3 hours at 80-110 km/h with a battery life of 50% remaining. Upon first glance, the charging stations were clear to locate and readily available with no lines. We charged 35,77 kWh for Rp 96,000 in just 54 minutes – the perfect amount of time for a leisurely breakfast.

Jakarta to our first charging station rest area

Location: SPKLU KM 228A rest area

By 10am, we were back on the road and reached Semarang by 12pm. This leg of the trip covered 201 km and took around 2 hours and 14 minutes. Traffic thinned out at this point and we were able to speed up to 140 km/h in the hot weather, leaving the battery at 41%.

Our next pit stop was at the PLN office in Semarang, where we juiced up 47,80 kWh for Rp 130,000 in 59 minutes. This charging station went above and beyond with its offerings including a lounge with full air conditioning, television, lounge chairs, and a coffee vending machine. With free amenities such as these, road tripping has never felt so easy.

Luxury at its finest in an EV charging station out of all places

Location: SPKLU PLN UID Central Java & DIY

All recharged both body and vehicle, we headed to the Padma Hotel to situate for the night. When parking, the hotel lot itself offered 2-3 AC type charging stations and several other EV cars were also at the ready to charge. It appears that EV cars are continuing to grow its interest even all the way in Semarang.

We spent the next day exploring the city. For readers who have never been, Semarang is the capital and largest city of Central Java, rich with history of being a major port during the Dutch colonial era. Walking around Old Town, well-preserved Dutch colonial buildings and antique shops lined the streets transporting you back in time. Its historical port has made Semarang to be a melting pot of Chinese, Indian Arab, and European culture as well, lending an abundant variety of charm and heritage on every street corner.

Gorgeous historical charm of Semarang

Photo credits: IG @sutanto.harsono and Wuddy Warsono

We headed to the city center for lunch and were greeted with a plethora of delicious local cuisine at the D’Kambodja Heritage restaurant. With its location being a cultural heritage building, we found that the interior blended Indonesian Dutch Chinese architecture lended a refreshing revitalized modern twist. Javanese ornaments and colorful flowers dripped from the ceiling, bringing a vibrant atmosphere to complement the “buffet style” of local dishes that will leave your mouth watering.

A feast of colors for the eyes and stomach

The D’Kambodja Heritage restaurant was opened by Anne Avantie, famed fashion designer who modernized the kebaya (traditional Indonesian long sleeve garment).

Our hunger for local eats and thirst for history appeased, we headed to meet with local businesses. Having spoken with those in various sectors, we found that businesses in Central Java is thriving. This is largely due to the relocations of many factories from West Java into the central region, driven mainly from a desire to capitalize on the region’s lower wages. We had the opportunity to also visit the Grand Batang City, the new industrial park for infrastructure development. Although the area is still under construction, the potential for growth is evident. Tangible growth can be seen in Central Java through these new businesses and initiatives, promising an exciting economic boom.

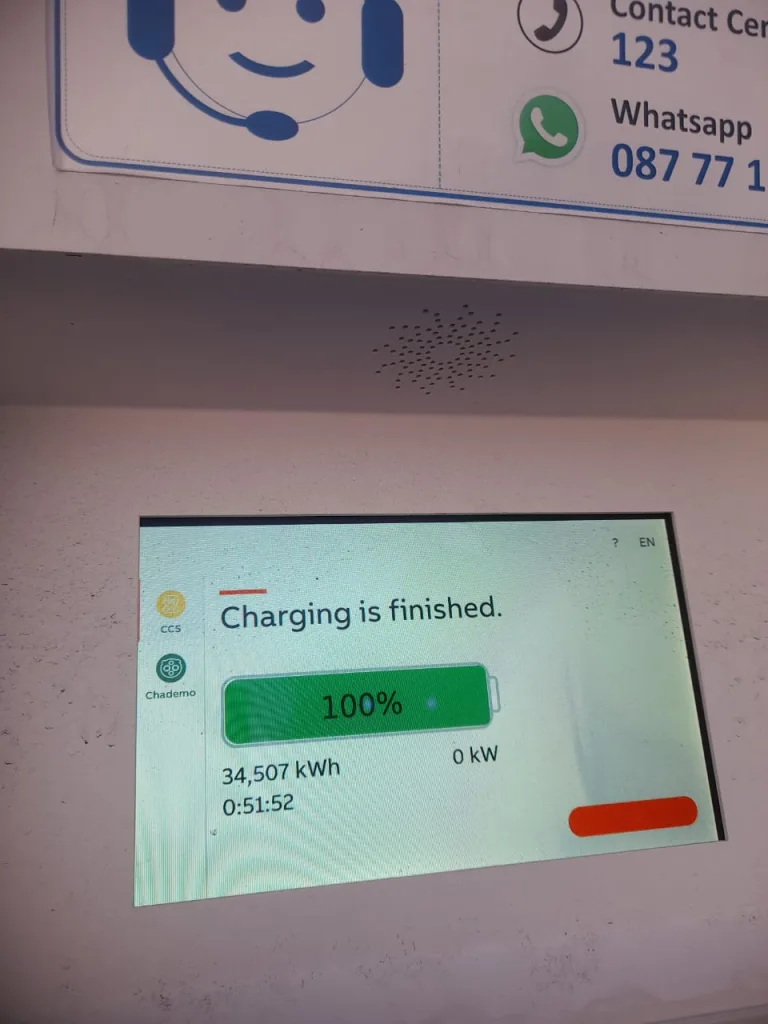

It was with this exciting sentiment that we made our way to one last charging station before starting our journey back to Jakarta. This rest area costing Rp 95,000 for 34.5 kWh and took 53 minutes to fully charge. Once again, easy to find and locate with no lines to wait behind. The premises themselves are clean and charging features easy to navigate ourselves.

Laying the groundwork: new industrial structures in the making

First picture: Alderon Factory (IMPC group)

Second and third picture: ongoing structures being built

It was with this exciting sentiment that we made our way to one last charging station before starting our journey back to Jakarta. This rest area costing Rp 95,000 for 34.5 kWh and took 53 minutes to fully charge. Once again, easy to find and locate with no lines to wait behind. The premises themselves are clean and charging features easy to navigate ourselves.

Our last pit stop before heading back home

Location: SPKLU KM 360 B Toll Batang – Semarang rest area

The total trip from Jakarta to Semarang and back roughly covered 900 km, which only needed 3 pit stops to charge the car and were a breeze to locate. At an average cost of Rp 2,727 per kWh, we spent a total of Rp 321,966 to and back. Compared to a gas car, we estimate it would have roughly costed around a whopping Rp 1,106,250 for the same distance. Our wallets were crying in relief.

Electric cars are a win for your wallet

Semarang offered convenient charging options, including the Padma Hotel’s AC stations and numerous AC and DC stations along the toll roads. We counted around 9-10 EV charging stations between Jakarta and Semarang, none of which were crowded. Should EV interest surge, we do think there would be a growing need for more charging stations. This trip is also a testament proving that EVs are not only cost-effective but also comparable in travel time to gasoline cars. EVs are not only kind to the planet but also to the pocket, matching gasoline cars in travel time while delivering significant savings. With this electrifying adventure, the future of travel is bright, efficient, and definitely more affordable.

Drive electric, save green: both the planet and your wallet will thank you!

Tara Mulia

Admin heyokha

Feedback for Us

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labor.

Share

Published: Jul 09 2024

Indonesia’s journey towards an energy transition, particularly with the adoption of electric vehicles (EVs), has been met with a fair share of skepticism. Concerns about the availability of charging stations, the cost-efficiency of EVs, and the overall practicality of long-distance travel in an EV have loomed large. However, our recent road round trip from Jakarta to Semarang which is around 400km one way pleasantly surprised us, casting away many of those doubts. Here’s a recount of our electrifying adventure that proved the naysayers wrong.

Charging stations aplenty from Jakarta to Semarang

Bird eye view of several charging stations by the National Electric Company along the toll roads

Starting at 5:30am from our office with a fully charged battery and a sense of adventure, we were ready to begin. Mind you, this was our first time taking our EV, a Hyundai Ioniq 5, to a trip this far and long so we were cautiously optimistic. Leaving at the break of dawn has its perks namely avoiding the notorious Jakarta traffic jam. Whizzing past several rest areas, we were able to spot almost if not all had the electric sign logos on their billboards showing EV charging station availability. Fortune was on our side.

With rest areas aplenty by the toll roads, our first leg of the journey took us to the midpoint at the KM 228A rest area. We covered 243 km in under 3 hours at 80-110 km/h with a battery life of 50% remaining. Upon first glance, the charging stations were clear to locate and readily available with no lines. We charged 35,77 kWh for Rp 96,000 in just 54 minutes – the perfect amount of time for a leisurely breakfast.

Jakarta to our first charging station rest area

Location: SPKLU KM 228A rest area

By 10am, we were back on the road and reached Semarang by 12pm. This leg of the trip covered 201 km and took around 2 hours and 14 minutes. Traffic thinned out at this point and we were able to speed up to 140 km/h in the hot weather, leaving the battery at 41%.

Our next pit stop was at the PLN office in Semarang, where we juiced up 47,80 kWh for Rp 130,000 in 59 minutes. This charging station went above and beyond with its offerings including a lounge with full air conditioning, television, lounge chairs, and a coffee vending machine. With free amenities such as these, road tripping has never felt so easy.

Luxury at its finest in an EV charging station out of all places

Location: SPKLU PLN UID Central Java & DIY

All recharged both body and vehicle, we headed to the Padma Hotel to situate for the night. When parking, the hotel lot itself offered 2-3 AC type charging stations and several other EV cars were also at the ready to charge. It appears that EV cars are continuing to grow its interest even all the way in Semarang.

We spent the next day exploring the city. For readers who have never been, Semarang is the capital and largest city of Central Java, rich with history of being a major port during the Dutch colonial era. Walking around Old Town, well-preserved Dutch colonial buildings and antique shops lined the streets transporting you back in time. Its historical port has made Semarang to be a melting pot of Chinese, Indian Arab, and European culture as well, lending an abundant variety of charm and heritage on every street corner.

Gorgeous historical charm of Semarang

Photo credits: IG @sutanto.harsono and Wuddy Warsono

We headed to the city center for lunch and were greeted with a plethora of delicious local cuisine at the D’Kambodja Heritage restaurant. With its location being a cultural heritage building, we found that the interior blended Indonesian Dutch Chinese architecture lended a refreshing revitalized modern twist. Javanese ornaments and colorful flowers dripped from the ceiling, bringing a vibrant atmosphere to complement the “buffet style” of local dishes that will leave your mouth watering.

A feast of colors for the eyes and stomach

The D’Kambodja Heritage restaurant was opened by Anne Avantie, famed fashion designer who modernized the kebaya (traditional Indonesian long sleeve garment).

Our hunger for local eats and thirst for history appeased, we headed to meet with local businesses. Having spoken with those in various sectors, we found that businesses in Central Java is thriving. This is largely due to the relocations of many factories from West Java into the central region, driven mainly from a desire to capitalize on the region’s lower wages. We had the opportunity to also visit the Grand Batang City, the new industrial park for infrastructure development. Although the area is still under construction, the potential for growth is evident. Tangible growth can be seen in Central Java through these new businesses and initiatives, promising an exciting economic boom.

It was with this exciting sentiment that we made our way to one last charging station before starting our journey back to Jakarta. This rest area costing Rp 95,000 for 34.5 kWh and took 53 minutes to fully charge. Once again, easy to find and locate with no lines to wait behind. The premises themselves are clean and charging features easy to navigate ourselves.

Laying the groundwork: new industrial structures in the making

First picture: Alderon Factory (IMPC group)

Second and third picture: ongoing structures being built

It was with this exciting sentiment that we made our way to one last charging station before starting our journey back to Jakarta. This rest area costing Rp 95,000 for 34.5 kWh and took 53 minutes to fully charge. Once again, easy to find and locate with no lines to wait behind. The premises themselves are clean and charging features easy to navigate ourselves.

Our last pit stop before heading back home

Location: SPKLU KM 360 B Toll Batang – Semarang rest area

The total trip from Jakarta to Semarang and back roughly covered 900 km, which only needed 3 pit stops to charge the car and were a breeze to locate. At an average cost of Rp 2,727 per kWh, we spent a total of Rp 321,966 to and back. Compared to a gas car, we estimate it would have roughly costed around a whopping Rp 1,106,250 for the same distance. Our wallets were crying in relief.

Electric cars are a win for your wallet

Semarang offered convenient charging options, including the Padma Hotel’s AC stations and numerous AC and DC stations along the toll roads. We counted around 9-10 EV charging stations between Jakarta and Semarang, none of which were crowded. Should EV interest surge, we do think there would be a growing need for more charging stations. This trip is also a testament proving that EVs are not only cost-effective but also comparable in travel time to gasoline cars. EVs are not only kind to the planet but also to the pocket, matching gasoline cars in travel time while delivering significant savings. With this electrifying adventure, the future of travel is bright, efficient, and definitely more affordable.

Drive electric, save green: both the planet and your wallet will thank you!

Tara Mulia

Admin heyokha

Feedback for Us

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labor.

“Investing in EMs in the past decade is like preparing for a firework show that ends with a single sparkler—underwhelming and disappointing.”

We’re all familiar with the conversations above, albeit in different forms. Just mention “EM (Emerging Market) equity” at a cocktail party, and you’ll see people quickly finishing their drinks and changing the subject to US market investing. Could this be a classic example of Peter Lynch’s cocktail party theory, indicating that the market is bottoming out?

Beyond the liquor In “One Up on Wall Street,” Peter Lynch identified cocktail party conversations as a significant contrarian market indicator. When people avoid discussing certain investments, it’s often a sign that the market is bottoming, presenting an opportunity to find undervalued stocks. Conversely, when such gatherings are filled with investment tips and general euphoria, it typically signals that the market is peaking and a downturn may be imminent.

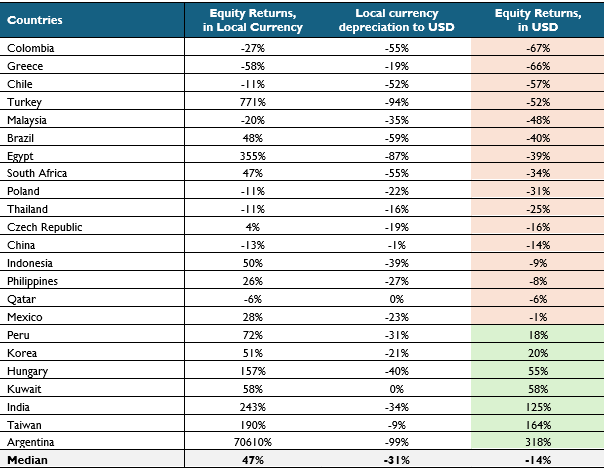

The following table below showcases why people have been quickly jumping to avoid topics linked to anything with EM investing.

Discussing EM equity returns in the past decade is a conversation-stopper

Equity returns and currencies performance of EM between 2013 to Q1 2024

Note: The equity market return of each country is represented by its respective MSCI country index, rounded.

Source: Bloomberg

EM equity returns over the past decade have indeed been dismal, particularly in USD terms. Of the 23 emerging markets tracked by MSCI, fifteen recorded positive returns in local currency terms. However, only six recorded positive returns when local currency depreciation is taken into account.

Focusing on our Southeast Asia market, none have been positive in USD terms. It’s no wonder it feels like a rollercoaster that has never left the ground.

Take Indonesia, for instance: Indonesian equities, as represented by MSCI Indonesia, achieved a cumulative return of 50 percent over the past decade. However, when we consider the 39 percent depreciation of the Rupiah during this period, the return plunged to a negative 9 percent.

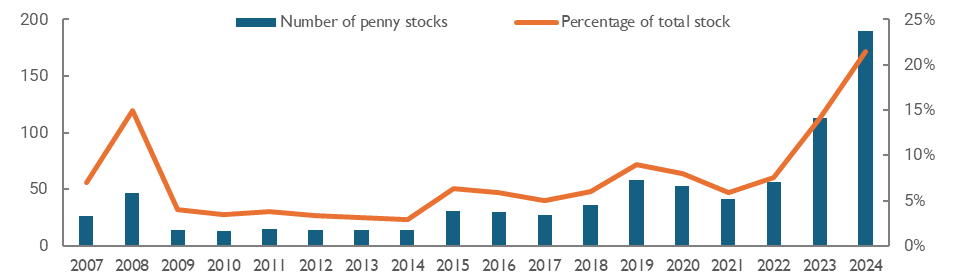

Another perspective, as illustrated in the table below, is that no less than 22 percent of Indonesian stocks are currently trading at or below IDR 50, which used to be the floor price until recent changes. This represents a record high, more than three times the figures seen during the COVID era. To make matters worse, trading volume has significantly decreased. Public expectations for future returns from equity investing are very low or nonexistent.

Penny stocks make up a fifth of Indonesian stocks

# of stocks traded at Rp 50 per share, the lowest possible price in JCI

Source: Bloomberg

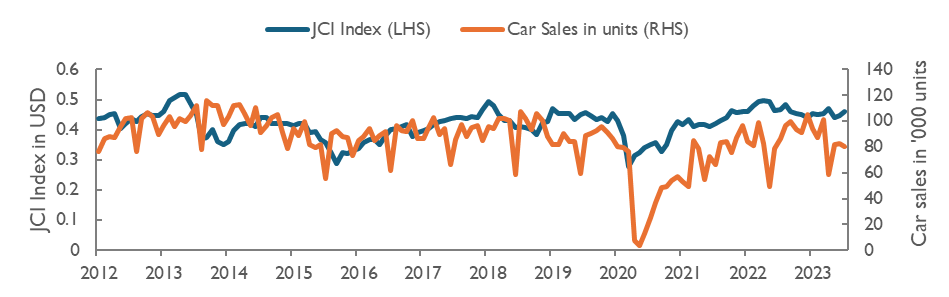

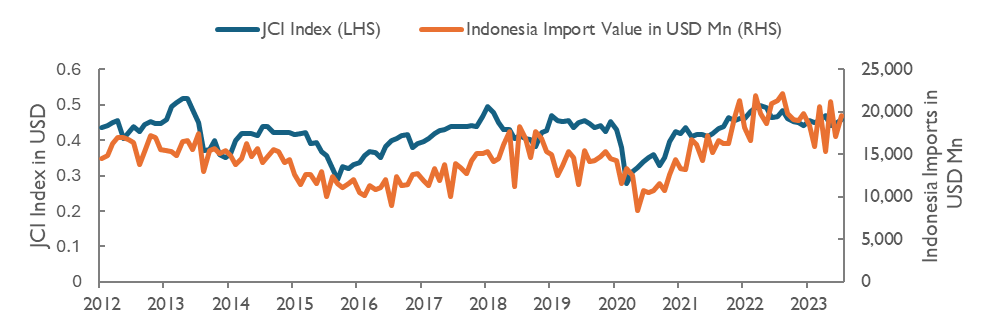

Moving on to the real sectors, the situation is not any better. Key economic indicators of middle-class prosperity, such as auto sales, have been going nowhere for the past 14 years since 2010, despite a 39.4% GDP per capita growth. Are things really that bad? Yes, they are.

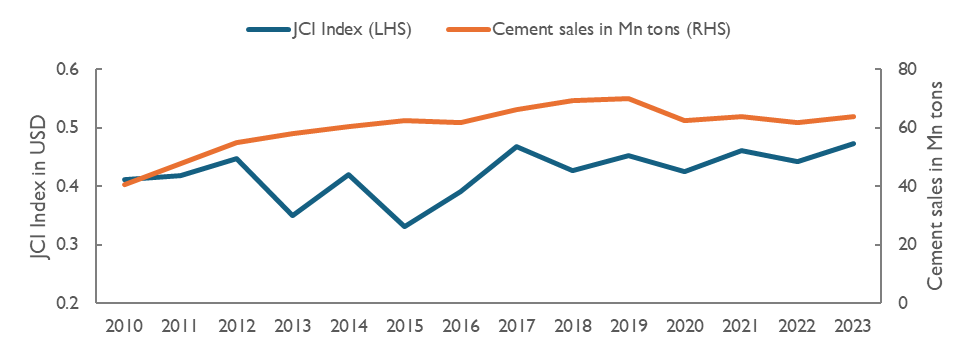

Jakarta Composite Index (“JCI”) in USD echoes coincidence indicators

Indonesia 4W car sales, imports, and cement sales are flat

Source: Bloomberg, Gaikindo (Ministry of Industry)

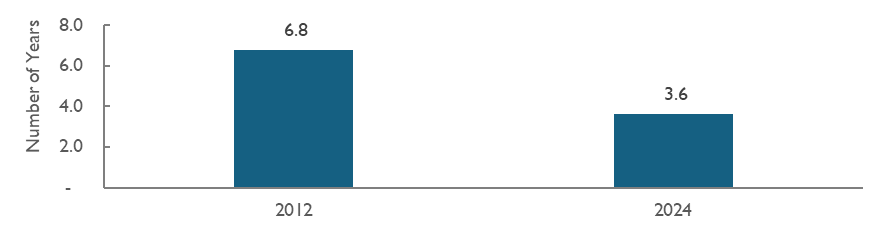

Oddly enough, the number of years it takes to afford the go to car on minimum wage has decreased. What is missing here?

Note: Annualized average minimum wage in Indonesia divided by Toyota Avanza1.3 E M/T car price of the respective year

Source: Auto2000, Kemnaker (Ministry of Manpower).

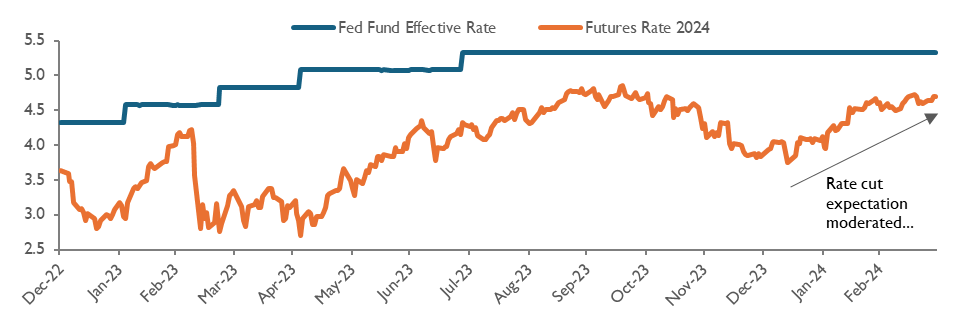

Stockbrokers, struggling with the decreasing revenue pool, have hoped on prophecies of rate cuts. The only difference in their forecasts was which month the rate cuts were going to be delivered. We know what happened next. Until today, the coaster is still stuck on the ground and the greenback has been mighty. This has been weighing down on the EM equities.

Rate cut expectation fades?

The Fed futures rate (%) and effective fund rate

Source: Bloomberg

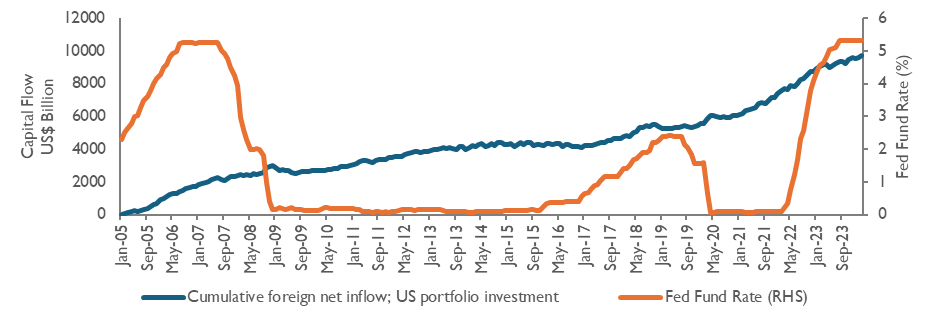

High interest rates draws back capital back to the US

Cumulative foreign net inflow of US portfolio (US$ Bn, since 2005) vs. Fed Fund Rate

Source: Bloomberg

In order for EMs to start performing, the prayer list includes: (1) tamed inflation, (2) recession, and (3) rate cuts as a result of the previous two. Some of these prayers are materializing, but not yet fully granted.

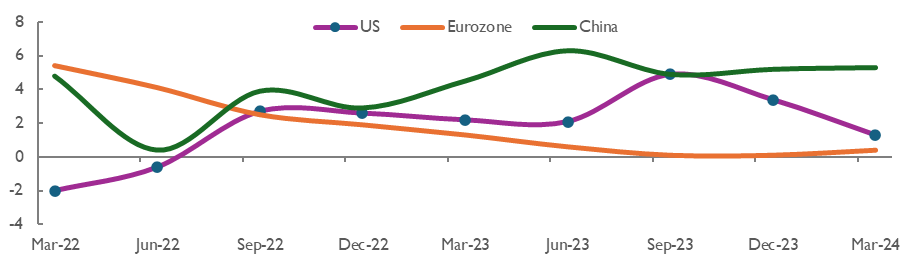

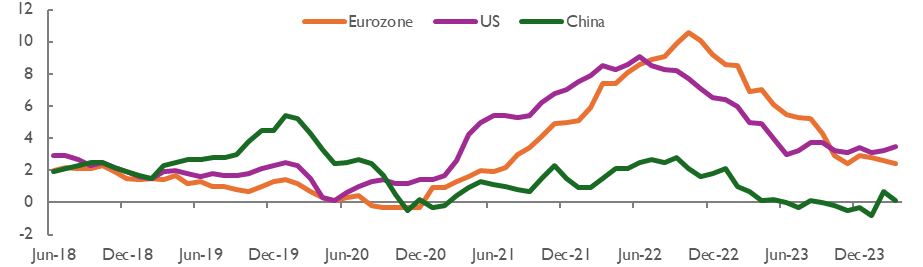

Moderating inflation and weak US economics are precursors for rate cuts

Real GDP growth (YoY) stagnated in Europe, slowed in the US, and was modest in China

CPI inflation (%, YoY) moderating into a new higher-normal

Source: Bloomberg

With all the negativity, it’s easy to fall into the gloom and doom camp about everything. However, much like a dense forest where sunlight occasionally breaks through the canopy, pockets of strength can still be found outside the US market. These bright spots offer hope and opportunity, reminding us that even amidst widespread challenges, there are areas where growth and resilience continue to thrive.

Now imagine a flat bowl balanced on a bamboo tower, filled with water. If everything were static, the water would overflow equally everywhere. But the market isn’t static; it’s a wild circus with elephants (market players) pushing the bowl, spilling water mostly where they prefer, leaving other places dry.

Some get the flow, Some do not

Similarly in emerging markets, some regions are left parched, while others are flourishing with liquidity. Take Argentina, for example. Thanks to radical changes like a smaller government and dollarization, its stock market is bubbling up nicely.

Sure, some might say Argentina’s market is just a tiny puddle in the vast ocean of global capital, with only a USD 53 billion market size. But this goes to show that even in a topsy-turvy market, there are still pockets of opportunity.

So, is it just a periphery market phenomenon in the EM space? We think not. Enter India.

Modi’s administration introduced game-changing economic reforms that transformed India into one of the world’s leading economies. In this case, the game changers are: (1) pro-investment policies and (2) savvy and effective approach to attract Western investments averting from China.

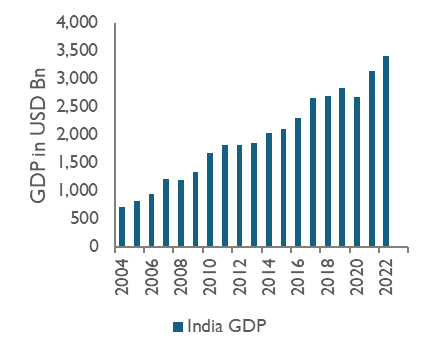

Indonesia’s trade surplus with India – potential commodity supercycle is on the horizon

India GDP (left), in bn USD. Indonesia – India trade balance (right). In USD bn

Source: Bloomberg, Government of Indonesia

Currently, India’s per capita income stands at a modest USD 2,400. However, using the rule of 72, we can make an optimistic projection. Assuming a 6% GDP per capita growth year over year, Indians will be twice as rich in just 12 years.

When incomes rise, consumption patterns change. The first things people tend to buy with their newfound wealth are goods. And when we talk about goods, we’re talking about commodities—lots of them. Increased demand for commodities translates into a thriving market for producers and exporters. Enter Indonesia, which happens to be rich in natural resources and commodities.

Indonesia stands to gain significantly from this economic evolution in India. With its vast reserves of minerals, agricultural products, and energy resources, Indonesia is perfectly positioned to supply the growing Indian appetite for commodities. As India’s middle class expands and consumption increases, Indonesian exports to India are likely to surge, benefiting both economies.

So, while India’s per capita income growth signals a brighter future for its citizens, it also opens up lucrative opportunities for Indonesia. This symbiotic relationship highlights the interconnected nature of global economies, where the prosperity of one nation can ripple out to benefit others.

Still on the subject of Indonesia, recent negative headlines have highlighted the potential for public debt to GDP to reach 50% from the current 39%. Simple arithmetic suggests that this reported figure does not add up.

Leveraging up to 50% would entail significant ramifications, including: (1) interest expenses to revenue reaching 30%, worse than Bangladesh, (2) implying a fiscal deficit of over 5%, well above the 3% limit stipulated by current law, (3) changing this law being improbable given the current parliamentary composition, (4) a significant sovereign downgrade, problematic given that the capital and current account remain negative, and (5) the crowding-out effect, where higher interest rates and an influx of government bonds discourage private sector investments.

All of the above does not seem to be a sensible move for the new Indonesian government.

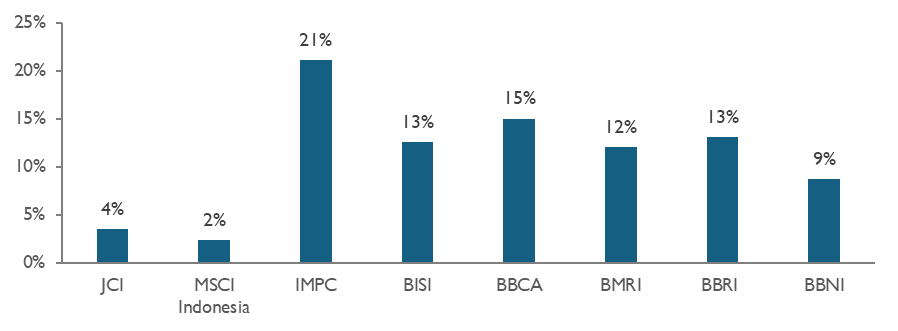

Case in point: finding Pocket of performance in Indonesia

Most investors are already familiar with the success stories of Indonesia’s big four banks. However, despite the prevalent bearish sentiment in the small to mid-cap space in Indonesia, there are noteworthy fast-growing companies in this category. These companies often fly under the radar of many investors, yet they offer significant growth potential. Bisi International (BISI IJ) and Impack Pratama (IMPC IJ) are prime examples of such hidden gems. BISI IJ is a major player in agricultural solutions, providing a wide range of products and services to enhance agricultural productivity. IMPC IJ specializes in alternative building materials, offering innovative and sustainable solutions for construction projects.

What sets these companies apart is their exceptional execution in relatively niche markets that are typically unappealing to larger conglomerates. BISI IJ excels in its specialized agricultural market, leveraging its expertise to drive growth and innovation. Similarly, IMPC IJ focuses on alternative building materials, a sector often overlooked by bigger players. This focus allows both companies to carve out strong market positions and achieve impressive growth rates. Their success stories underscore the potential that exists in Indonesia’s small to mid-cap space, offering investors attractive opportunities beyond the well-known large-cap stocks.

There are gems in muddy water

CAGR (%) on TTM EPS in USD (2014-2024)

CAGR (%) on Total Net Return with Dividends in USD (2014-2024)

Source: Bloomberg

Another topic we have seen people turn away from in a cocktail party until very recently is precious metals. Gold and its poor cousin silver may seem like the dinosaurs of the investment world—static, unexciting, and about as useful as a paperweight in the digital age. It doesn’t generate dividends, won’t give you the thrill of tech stocks, and can sit there for ages without making a splash.

Here’s the kicker: investors should still keep an eye on it. Despite its old-school charm, precious metals have a knack for shining when things get rough. It’s the financial world’s version of a trusty old sweater, offering warmth and comfort when the economic weather turns chilly. So, while it might not be the flashiest asset in your portfolio, it’s definitely one asset class worth allocating into.

Time to rethink your holiday

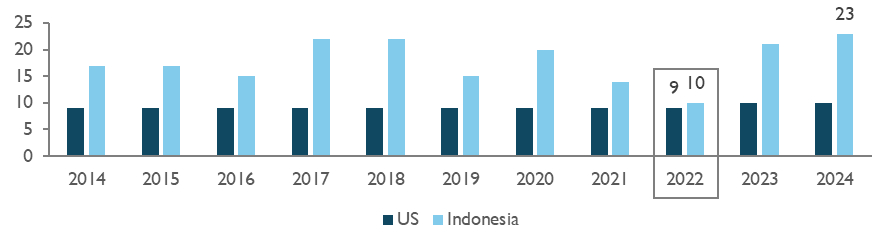

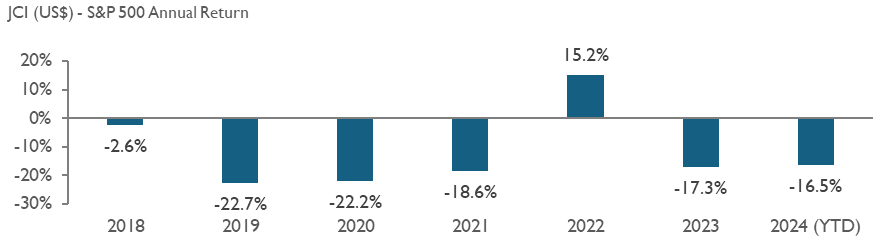

Indonesia is breaking records, but it’s not for the hottest chili or longest dance marathon—it’s for holidays, racking up a whopping 23 days off this year. Meanwhile, the US sticks to a lean average of 9 days. For investors, it’s been a rough ride in emerging markets, with US stocks often leaving Indonesian ones eating dust. Interestingly in 2022, Indonesia’s Jakarta Composite Index (JCI) outshined the S&P 500 with a dazzling 15% gain. Coincidentally, Indonesia only took 10 holidays that year, almost mirroring the US. Could fewer holidays be the secret sauce for market success? Something to chew on as we plan our next beach getaway!

Indonesia’s JCI outperformed S&P500 when its holidays were the lowest

Number of stock market holidays of the US vs Indonesia (in days)

Source: Bloomberg

Admin heyokha

Feedback for Us

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labor.

Share

Published: Jul 02 2024

“Investing in EMs in the past decade is like preparing for a firework show that ends with a single sparkler—underwhelming and disappointing.”

We’re all familiar with the conversations above, albeit in different forms. Just mention “EM (Emerging Market) equity” at a cocktail party, and you’ll see people quickly finishing their drinks and changing the subject to US market investing. Could this be a classic example of Peter Lynch’s cocktail party theory, indicating that the market is bottoming out?

Beyond the liquor In “One Up on Wall Street,” Peter Lynch identified cocktail party conversations as a significant contrarian market indicator. When people avoid discussing certain investments, it’s often a sign that the market is bottoming, presenting an opportunity to find undervalued stocks. Conversely, when such gatherings are filled with investment tips and general euphoria, it typically signals that the market is peaking and a downturn may be imminent.

The following table below showcases why people have been quickly jumping to avoid topics linked to anything with EM investing.

Discussing EM equity returns in the past decade is a conversation-stopper

Equity returns and currencies performance of EM between 2013 to Q1 2024

Note: The equity market return of each country is represented by its respective MSCI country index, rounded.

Source: Bloomberg

EM equity returns over the past decade have indeed been dismal, particularly in USD terms. Of the 23 emerging markets tracked by MSCI, fifteen recorded positive returns in local currency terms. However, only six recorded positive returns when local currency depreciation is taken into account.

Focusing on our Southeast Asia market, none have been positive in USD terms. It’s no wonder it feels like a rollercoaster that has never left the ground.

Take Indonesia, for instance: Indonesian equities, as represented by MSCI Indonesia, achieved a cumulative return of 50 percent over the past decade. However, when we consider the 39 percent depreciation of the Rupiah during this period, the return plunged to a negative 9 percent.

Another perspective, as illustrated in the table below, is that no less than 22 percent of Indonesian stocks are currently trading at or below IDR 50, which used to be the floor price until recent changes. This represents a record high, more than three times the figures seen during the COVID era. To make matters worse, trading volume has significantly decreased. Public expectations for future returns from equity investing are very low or nonexistent.

Penny stocks make up a fifth of Indonesian stocks

# of stocks traded at Rp 50 per share, the lowest possible price in JCI

Source: Bloomberg

Moving on to the real sectors, the situation is not any better. Key economic indicators of middle-class prosperity, such as auto sales, have been going nowhere for the past 14 years since 2010, despite a 39.4% GDP per capita growth. Are things really that bad? Yes, they are.

Jakarta Composite Index (“JCI”) in USD echoes coincidence indicators

Indonesia 4W car sales, imports, and cement sales are flat

Source: Bloomberg, Gaikindo (Ministry of Industry)

Oddly enough, the number of years it takes to afford the go to car on minimum wage has decreased. What is missing here?

Note: Annualized average minimum wage in Indonesia divided by Toyota Avanza1.3 E M/T car price of the respective year

Source: Auto2000, Kemnaker (Ministry of Manpower).

Stockbrokers, struggling with the decreasing revenue pool, have hoped on prophecies of rate cuts. The only difference in their forecasts was which month the rate cuts were going to be delivered. We know what happened next. Until today, the coaster is still stuck on the ground and the greenback has been mighty. This has been weighing down on the EM equities.

Rate cut expectation fades?

The Fed futures rate (%) and effective fund rate

Source: Bloomberg

High interest rates draws back capital back to the US

Cumulative foreign net inflow of US portfolio (US$ Bn, since 2005) vs. Fed Fund Rate

Source: Bloomberg

In order for EMs to start performing, the prayer list includes: (1) tamed inflation, (2) recession, and (3) rate cuts as a result of the previous two. Some of these prayers are materializing, but not yet fully granted.

Moderating inflation and weak US economics are precursors for rate cuts

Real GDP growth (YoY) stagnated in Europe, slowed in the US, and was modest in China

CPI inflation (%, YoY) moderating into a new higher-normal

Source: Bloomberg

With all the negativity, it’s easy to fall into the gloom and doom camp about everything. However, much like a dense forest where sunlight occasionally breaks through the canopy, pockets of strength can still be found outside the US market. These bright spots offer hope and opportunity, reminding us that even amidst widespread challenges, there are areas where growth and resilience continue to thrive.

Now imagine a flat bowl balanced on a bamboo tower, filled with water. If everything were static, the water would overflow equally everywhere. But the market isn’t static; it’s a wild circus with elephants (market players) pushing the bowl, spilling water mostly where they prefer, leaving other places dry.

Some get the flow, Some do not

Similarly in emerging markets, some regions are left parched, while others are flourishing with liquidity. Take Argentina, for example. Thanks to radical changes like a smaller government and dollarization, its stock market is bubbling up nicely.

Sure, some might say Argentina’s market is just a tiny puddle in the vast ocean of global capital, with only a USD 53 billion market size. But this goes to show that even in a topsy-turvy market, there are still pockets of opportunity.

So, is it just a periphery market phenomenon in the EM space? We think not. Enter India.

Modi’s administration introduced game-changing economic reforms that transformed India into one of the world’s leading economies. In this case, the game changers are: (1) pro-investment policies and (2) savvy and effective approach to attract Western investments averting from China.

Indonesia’s trade surplus with India – potential commodity supercycle is on the horizon

India GDP (left), in bn USD. Indonesia – India trade balance (right). In USD bn

Source: Bloomberg, Government of Indonesia

Currently, India’s per capita income stands at a modest USD 2,400. However, using the rule of 72, we can make an optimistic projection. Assuming a 6% GDP per capita growth year over year, Indians will be twice as rich in just 12 years.

When incomes rise, consumption patterns change. The first things people tend to buy with their newfound wealth are goods. And when we talk about goods, we’re talking about commodities—lots of them. Increased demand for commodities translates into a thriving market for producers and exporters. Enter Indonesia, which happens to be rich in natural resources and commodities.

Indonesia stands to gain significantly from this economic evolution in India. With its vast reserves of minerals, agricultural products, and energy resources, Indonesia is perfectly positioned to supply the growing Indian appetite for commodities. As India’s middle class expands and consumption increases, Indonesian exports to India are likely to surge, benefiting both economies.

So, while India’s per capita income growth signals a brighter future for its citizens, it also opens up lucrative opportunities for Indonesia. This symbiotic relationship highlights the interconnected nature of global economies, where the prosperity of one nation can ripple out to benefit others.

Still on the subject of Indonesia, recent negative headlines have highlighted the potential for public debt to GDP to reach 50% from the current 39%. Simple arithmetic suggests that this reported figure does not add up.

Leveraging up to 50% would entail significant ramifications, including: (1) interest expenses to revenue reaching 30%, worse than Bangladesh, (2) implying a fiscal deficit of over 5%, well above the 3% limit stipulated by current law, (3) changing this law being improbable given the current parliamentary composition, (4) a significant sovereign downgrade, problematic given that the capital and current account remain negative, and (5) the crowding-out effect, where higher interest rates and an influx of government bonds discourage private sector investments.

All of the above does not seem to be a sensible move for the new Indonesian government.

Case in point: finding Pocket of performance in Indonesia

Most investors are already familiar with the success stories of Indonesia’s big four banks. However, despite the prevalent bearish sentiment in the small to mid-cap space in Indonesia, there are noteworthy fast-growing companies in this category. These companies often fly under the radar of many investors, yet they offer significant growth potential. Bisi International (BISI IJ) and Impack Pratama (IMPC IJ) are prime examples of such hidden gems. BISI IJ is a major player in agricultural solutions, providing a wide range of products and services to enhance agricultural productivity. IMPC IJ specializes in alternative building materials, offering innovative and sustainable solutions for construction projects.

What sets these companies apart is their exceptional execution in relatively niche markets that are typically unappealing to larger conglomerates. BISI IJ excels in its specialized agricultural market, leveraging its expertise to drive growth and innovation. Similarly, IMPC IJ focuses on alternative building materials, a sector often overlooked by bigger players. This focus allows both companies to carve out strong market positions and achieve impressive growth rates. Their success stories underscore the potential that exists in Indonesia’s small to mid-cap space, offering investors attractive opportunities beyond the well-known large-cap stocks.

There are gems in muddy water

CAGR (%) on TTM EPS in USD (2014-2024)

CAGR (%) on Total Net Return with Dividends in USD (2014-2024)

Source: Bloomberg

Another topic we have seen people turn away from in a cocktail party until very recently is precious metals. Gold and its poor cousin silver may seem like the dinosaurs of the investment world—static, unexciting, and about as useful as a paperweight in the digital age. It doesn’t generate dividends, won’t give you the thrill of tech stocks, and can sit there for ages without making a splash.

Here’s the kicker: investors should still keep an eye on it. Despite its old-school charm, precious metals have a knack for shining when things get rough. It’s the financial world’s version of a trusty old sweater, offering warmth and comfort when the economic weather turns chilly. So, while it might not be the flashiest asset in your portfolio, it’s definitely one asset class worth allocating into.

Time to rethink your holiday

Indonesia is breaking records, but it’s not for the hottest chili or longest dance marathon—it’s for holidays, racking up a whopping 23 days off this year. Meanwhile, the US sticks to a lean average of 9 days. For investors, it’s been a rough ride in emerging markets, with US stocks often leaving Indonesian ones eating dust. Interestingly in 2022, Indonesia’s Jakarta Composite Index (JCI) outshined the S&P 500 with a dazzling 15% gain. Coincidentally, Indonesia only took 10 holidays that year, almost mirroring the US. Could fewer holidays be the secret sauce for market success? Something to chew on as we plan our next beach getaway!

Indonesia’s JCI outperformed S&P500 when its holidays were the lowest

Number of stock market holidays of the US vs Indonesia (in days)

Source: Bloomberg

Admin heyokha

Feedback for Us

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labor.

Share

Stay Connected with Heyokha

Sign up to receive insights, updates, and perspectives directly from Heyokha

Stay Connected with Heyokha

Sign up to receive insights, updates, and perspectives directly from Heyokha

We drive our mission with an exceptional culture through applying a growth mindset where holistic and on the ground research is at our core.

You must read the following information before proceeding. By accessing this website and any pages thereof, you acknowledge that you have read the following information and accept the terms and conditions set out below and agree to be bound by such terms and conditions. If you do not agree to such terms and conditions, please do not access this website or any pages thereof.

The website has been prepared by Heyokha Brothers Limited and is solely intended for informational purposes and should not be construed as an inducement to purchase or sell any security, product, service, or investment. The Site does not solicit an offer to buy or sell any financial instrument or enter into any agreement. It is important to note that the opinions expressed on the Site are not considered investment advice, and it is recommended that individuals seek independent advice as needed to address their specific objectives, financial situation, or needs. It is the responsibility of the persons who access this website to observe all applicable laws and regulations.

The Site offers general information exclusively and does not consider the individual circumstances of any person. The data, opinions, and estimates presented on the Site are current as of the publication date and are subject to changes without notice. Additionally, it is possible that such information may become obsolete with time.

Intended Users

The content presented on this website is exclusively intended for authorized intermediaries and qualified investors within Hong Kong, such as institutional investors, professional investors, and accredited investors (as defined under the SFO). It is not intended for retail investors or individuals located outside of Hong Kong.

The products and services mentioned on this website may or may not be authorized or registered for distribution in a particular jurisdiction and may not be suitable for all investor types. It is important to note that this website is not intended to constitute an offer or solicitation, nor is it directed toward individuals if the provider of the information is prohibited by any law of any jurisdiction from making the information available. Moreover, the website is not intended for any use that would violate local laws or regulations. The provider of the information is not permitted to promote any products or services mentioned on this website in jurisdictions where such promotion would be prohibited.

If you are not a qualified investor or licensed intermediary in Hong Kong, you should not proceed any further.

No Investment Advice

The information provided on this Website is for informational purposes only and should not be considered as investment advice or a recommendation to buy, sell, hold, or transact in any investment. It is strongly recommended that individuals seek professional investment advice before making any investment decisions.

The information presented on this Website does not consider the investment objectives, specific needs, or financial situations of any investor. It is important to note that nothing on this Website is intended to constitute financial, legal, accounting, or tax advice.

Before making any investment decision, individuals should carefully consider whether an investment aligns with their investment objectives, specific needs, and financial situation. This should also include informing oneself of any potential tax implications, legal requirements, foreign exchange restrictions, or exchange control requirements that may be relevant to an investment based on the laws of one’s citizenship, residence, or domicile. If there is any doubt regarding the information on this Website, it is recommended that individuals seek independent professional financial advice.

It is important to note that any opinion, comment, article, financial analysis, market forecast, market commentary, or other information published on the Website is not binding on Heyokha or its affiliates, and they are not responsible for the information, opinions, or ideas presented.

Obligations and Resposibilities of Users

Users are solely responsible for protecting and backing up their data and equipment, as well as taking reasonable precautions against any computer virus or other destructive elements. Additionally, users must ensure that their access to the Site is adequately secured against unauthorized access.

Users are prohibited from using the Site for any unlawful, defamatory, offensive, abusive, indecent, menacing, or threatening purposes, or in any way that infringes upon intellectual property rights or confidentiality obligations. Furthermore, users may not use the Site to cause annoyance, inconvenience, or anxiety to others, or in any way that violates any applicable laws or regulations.

Users must comply with any terms notified to them by third-party suppliers of data or services to the Site. This may include entering into a direct agreement with such third parties in respect of their use of the dat

Third-Party Content

This website may contain Third Party Content or links to websites maintained by third parties that are not affiliated with Heyokha. Heyokha does not participate in the preparation, adoption, or editing of such third-party materials and does not endorse or approve such content, either explicitly or implicitly. Any opinions or recommendations expressed on third party materials are solely those of the independent providers and not of Heyokha. Heyokha is not responsible for any errors or omissions relating to specific information provided by any third party.

Although Heyokha aims to provide accurate and timely information to users, neither Heyokha nor the Third-Party Content providers guarantee on the accuracy, timeliness, completeness, usefulness, or any other aspect of the information presented. Heyokha is not responsible or liable for any content, including advertising, products, or other materials on or available from third party sites. Users access and use Third Party content is at their own risk, and it is provided for informational purposes only. Both Heyokha and the Third-Party shall not be liable for any loss or damage arising from users’ reliance upon such information.

Intellectual Property Rights

The content of this website is subject to copyright and other intellectual property laws. All trademarks, service marks, logos, and brand features displayed on the website are owned by their respective owners, except as explicitly noted. Users may use the information on this website and reproduce it for personal reference only. However, reproduction, distribution, transmission, incorporation in any other database, document, or material, and sale or distribution of any part of the contents of the website is strictly prohibited. Users may download or print individual sections of the website for personal use and information only, provided they are legally entitled to access the material and retain all copyright and other proprietary notices.

Any unauthorized use of the content, trademarks, service marks, or logos displayed on the website may violate copyright, trademark, or other intellectual property laws, as well as laws of privacy and publicity and communications. Any reference or link to any specific commercial product, process, or service by trade name, trademark, manufacturer, or otherwise, does not necessarily constitute or imply its endorsement, recommendation, or favouring by our company.

We provide such references or links solely for the convenience of our users and to provide additional information. Our company is not responsible for the accuracy, legality, or content of any external website or resource linked to or referenced from our website. Users are solely responsible for complying with the terms and conditions of any external websites or resources.

Cookies

In order to enhance user experience and simplify future visits, this website may utilize cookies to track your activity. However, if you do not want to store cookies on your device, you can disable them by adjusting your browser’s security settings.

Data Privacy

Please read our Privacy Statement before providing Heyokha with any personal information on this website. By providing any personal information on this website, you will be deemed to have read and accepted our Privacy Statement.

Use of Website

The information contained on the website is accurate only as of the date of publication and does not constitute investment advice or recommendations. While certain tools available on the website may provide general investment or financial analyses based upon personalized input, such results are for information purposes only, and users should refer to the assumptions and limitations relevant to the use of such tools as set out on the website. Users are solely responsible for determining whether any investment, security or strategy, or any other product or service is appropriate or suitable for them based on their investment objectives and personal and financial situation. Users should consult their independent professional advisers if they have any questions. Any person considering an investment should seek independent advice on the suitability or otherwise of the particular investment.

Disclaimer of Liability Heyokha makes no warranty as to the accuracy, completeness, security, and confidentiality of information available through the website. Heyokha, its affiliates, directors, officers, or employees accept no liability for any errors or omissions relating to information available through the website or for any damages, losses or expenses arising in connection with the website, whether direct or indirect, arising from the use of the website or its contents. Heyokha also reserves the right to modify, suspend, or discontinue the website at any time without notice. Heyokha shall not be liable for any such modification, suspension, or discontinuance.

×

Data Privacy Terms and Conditions

Personal Information Collection Statement:

Pursuant to the Personal Data (Privacy) Ordinance (the ‘Ordinance’), Heyokha Brothers Limited is fully committed to safeguarding the privacy and security of personal information in compliance with all relevant laws and regulations. This statement outlines how we collect, use, and protect personal information provided to us.

Collection of Personal Information:

We collect and maintain personal information, in a manner consistent with all relevant laws and regulations. We take necessary measures to ensure that personal information is correct and up to date. Personal information will only be used for the purpose of utilization and will not be disclosed to third parties (except our related parties e.g.: Administrators) without consent from the individual, except for justifiable grounds as required by laws and regulations.

We may collect various types of personal data from or about you, including:

Your name

Your user names and passwords

Contact information, including address, email address and/or telephone number

Information relating to your engagement with material that we publish or otherwise provide to you

Records of our interactions with you, including any messages you send us, your comments and questions and any other information you choose to provide.

The Company may automatically collect information about you from computer or internet browser through the use of cookies, pixel tags, and other similar technologies to enhance the user experience on its websites.

Third parties may be used to collect personal data and information indirectly through monitoring activities conducted by the Company or on its behalf.

Company does not knowingly collect personal data from anyone under the age of 18 and does not seek to collect or process sensitive information unless required or permitted by law and with express consent.

Uses of your Personal Data:

We may use your personal data for the purposes it was provided and in connection with our services as described below:

Provide products/services or info as requested or expected.

Fulfill agreements and facilitate business dealings.

Manage relationships, analyse websites and communications, and merge personal data for relevance.

Support and improve existing products/services, and plan/develop new ones.

Count/recognize website visitors and analyse usage.

To comply with and assess compliance with applicable laws, rules and regulations and internal policies and procedures.

Use information for any other purpose with consent.

Protection of Personal Information:

We provide thorough training to our officers and employees to prevent the leakage or inappropriate use of personal information and provide information on a need-to-know basis. Managers in charge for controls and inspections are appointed, and appropriate control systems are established to ensure the privacy and security of personal information.

In the event that personal information is provided to an external contractor (e.g.: Administrator), we take responsibility for ensuring that the external contractor has proper systems in place to protect the privacy of personal information.

Third parties disclosure of Personal Information:

Personal information held by us relating to an individual will be kept confidential but may be provided to third parties the following purpose:

Comply with applicable laws or legal processes.

Investigate and prevent illegal activity, fraud, or violations of terms and conditions.

Protect and defend legal rights or defend against legal claims.

Facilitate business or asset transactions, such as financing, mergers, acquisitions, or bankruptcy.

With our related parties (e.g.: administrators) that are subject to appropriate data protection obligations

Representatives, agents or custodians appointed by the client (e.g.: Auditors, accountant)

Retention of Personal Information:

Disclosure, correction and termination of usage shall be carried out upon request of an individual in accordance with relevant laws and regulations.

Personal information collected will be retained for no longer than is necessary for the fulfilment of the purposes for which it was collected as per applicable laws and regulations.

Rights of the Individual:

Under relevant laws and regulations, any individual has the right to request access to any of the personal data that we hold by submitting a written request. Individuals are also entitled to request to correct, cancel or delete any of the personal data we hold if they believe such information is inaccurate, out of date or we no longer have a legitimate interest or lawful justification to retain or process.

×

Disclaimer

Heyokha Brothers Limited is the issuer of this website and holds Type 4 (advising on securities) and Type 9 (asset management) licenses issued by the Securities and Futures Commission in Hong Kong.

The information provided on this website has been prepared solely for licensed intermediaries and qualified investors in Hong Kong, including professional investors, institutional investors, and accredited investors (as defined under the Securities and Futures Ordinance). The information provided on this website is for informational purposes only and should not be construed as investment advice, nor an offer to sell or a solicitation of an offer to buy any security, investment product, or service.

Investment involves risk and investors may lose their entire investment. Investors are advised to seek professional advice before making any investment decisions. Past performance is not indicative of future performance and the value of investments may fluctuate. Please refer to the offering document(s) for details, including the investment objectives, risk factors, and fees and charges.

Heyokha Brothers Limited reserves the right to amend, update, or remove any information on this website at any time without notice. By accessing and using this website, you agree to be bound by the above terms and conditions.

You must read the following information before proceeding. By accessing this website and any pages thereof, you acknowledge that you have read the following information and accept the terms and conditions set out below and agree to be bound by such terms and conditions. If you do not agree to such terms and conditions, please do not access this website or any pages thereof.

The website has been prepared by Heyokha Brothers Limited and is solely intended for informational purposes and should not be construed as an inducement to purchase or sell any security, product, service, or investment. The Site does not solicit an offer to buy or sell any financial instrument or enter into any agreement. It is important to note that the opinions expressed on the Site are not considered investment advice, and it is recommended that individuals seek independent advice as needed to address their specific objectives, financial situation, or needs. It is the responsibility of the persons who access this website to observe all applicable laws and regulations.

The Site offers general information exclusively and does not consider the individual circumstances of any person. The data, opinions, and estimates presented on the Site are current as of the publication date and are subject to changes without notice. Additionally, it is possible that such information may become obsolete with time.

Intended Users

The content presented on this website is exclusively intended for authorized intermediaries and qualified investors within Hong Kong, such as institutional investors, professional investors, and accredited investors (as defined under the SFO). It is not intended for retail investors or individuals located outside of Hong Kong.

The products and services mentioned on this website may or may not be authorized or registered for distribution in a particular jurisdiction and may not be suitable for all investor types. It is important to note that this website is not intended to constitute an offer or solicitation, nor is it directed toward individuals if the provider of the information is prohibited by any law of any jurisdiction from making the information available. Moreover, the website is not intended for any use that would violate local laws or regulations. The provider of the information is not permitted to promote any products or services mentioned on this website in jurisdictions where such promotion would be prohibited.

If you are not a qualified investor or licensed intermediary in Hong Kong, you should not proceed any further.

No Investment Advice

The information provided on this Website is for informational purposes only and should not be considered as investment advice or a recommendation to buy, sell, hold, or transact in any investment. It is strongly recommended that individuals seek professional investment advice before making any investment decisions.

The information presented on this Website does not consider the investment objectives, specific needs, or financial situations of any investor. It is important to note that nothing on this Website is intended to constitute financial, legal, accounting, or tax advice.

Before making any investment decision, individuals should carefully consider whether an investment aligns with their investment objectives, specific needs, and financial situation. This should also include informing oneself of any potential tax implications, legal requirements, foreign exchange restrictions, or exchange control requirements that may be relevant to an investment based on the laws of one’s citizenship, residence, or domicile. If there is any doubt regarding the information on this Website, it is recommended that individuals seek independent professional financial advice.

It is important to note that any opinion, comment, article, financial analysis, market forecast, market commentary, or other information published on the Website is not binding on Heyokha or its affiliates, and they are not responsible for the information, opinions, or ideas presented.

Obligations and Resposibilities of Users

Users are solely responsible for protecting and backing up their data and equipment, as well as taking reasonable precautions against any computer virus or other destructive elements. Additionally, users must ensure that their access to the Site is adequately secured against unauthorized access.

Users are prohibited from using the Site for any unlawful, defamatory, offensive, abusive, indecent, menacing, or threatening purposes, or in any way that infringes upon intellectual property rights or confidentiality obligations. Furthermore, users may not use the Site to cause annoyance, inconvenience, or anxiety to others, or in any way that violates any applicable laws or regulations.

Users must comply with any terms notified to them by third-party suppliers of data or services to the Site. This may include entering into a direct agreement with such third parties in respect of their use of the dat

Third-Party Content

This website may contain Third Party Content or links to websites maintained by third parties that are not affiliated with Heyokha. Heyokha does not participate in the preparation, adoption, or editing of such third-party materials and does not endorse or approve such content, either explicitly or implicitly. Any opinions or recommendations expressed on third party materials are solely those of the independent providers and not of Heyokha. Heyokha is not responsible for any errors or omissions relating to specific information provided by any third party.

Although Heyokha aims to provide accurate and timely information to users, neither Heyokha nor the Third-Party Content providers guarantee on the accuracy, timeliness, completeness, usefulness, or any other aspect of the information presented. Heyokha is not responsible or liable for any content, including advertising, products, or other materials on or available from third party sites. Users access and use Third Party content is at their own risk, and it is provided for informational purposes only. Both Heyokha and the Third-Party shall not be liable for any loss or damage arising from users’ reliance upon such information.

Intellectual Property Rights

The content of this website is subject to copyright and other intellectual property laws. All trademarks, service marks, logos, and brand features displayed on the website are owned by their respective owners, except as explicitly noted. Users may use the information on this website and reproduce it for personal reference only. However, reproduction, distribution, transmission, incorporation in any other database, document, or material, and sale or distribution of any part of the contents of the website is strictly prohibited. Users may download or print individual sections of the website for personal use and information only, provided they are legally entitled to access the material and retain all copyright and other proprietary notices.

Any unauthorized use of the content, trademarks, service marks, or logos displayed on the website may violate copyright, trademark, or other intellectual property laws, as well as laws of privacy and publicity and communications. Any reference or link to any specific commercial product, process, or service by trade name, trademark, manufacturer, or otherwise, does not necessarily constitute or imply its endorsement, recommendation, or favouring by our company.

We provide such references or links solely for the convenience of our users and to provide additional information. Our company is not responsible for the accuracy, legality, or content of any external website or resource linked to or referenced from our website. Users are solely responsible for complying with the terms and conditions of any external websites or resources.

Cookies

In order to enhance user experience and simplify future visits, this website may utilize cookies to track your activity. However, if you do not want to store cookies on your device, you can disable them by adjusting your browser’s security settings.

Data Privacy

Please read our Privacy Statement before providing Heyokha with any personal information on this website. By providing any personal information on this website, you will be deemed to have read and accepted our Privacy Statement.

Use of Website

The information contained on the website is accurate only as of the date of publication and does not constitute investment advice or recommendations. While certain tools available on the website may provide general investment or financial analyses based upon personalized input, such results are for information purposes only, and users should refer to the assumptions and limitations relevant to the use of such tools as set out on the website. Users are solely responsible for determining whether any investment, security or strategy, or any other product or service is appropriate or suitable for them based on their investment objectives and personal and financial situation. Users should consult their independent professional advisers if they have any questions. Any person considering an investment should seek independent advice on the suitability or otherwise of the particular investment.

Disclaimer of Liability Heyokha makes no warranty as to the accuracy, completeness, security, and confidentiality of information available through the website. Heyokha, its affiliates, directors, officers, or employees accept no liability for any errors or omissions relating to information available through the website or for any damages, losses or expenses arising in connection with the website, whether direct or indirect, arising from the use of the website or its contents. Heyokha also reserves the right to modify, suspend, or discontinue the website at any time without notice. Heyokha shall not be liable for any such modification, suspension, or discontinuance.

×

Data Privacy Terms and Conditions

Personal Information Collection Statement:

Pursuant to the Personal Data (Privacy) Ordinance (the ‘Ordinance’), Heyokha Brothers Limited is fully committed to safeguarding the privacy and security of personal information in compliance with all relevant laws and regulations. This statement outlines how we collect, use, and protect personal information provided to us.

Collection of Personal Information:

We collect and maintain personal information, in a manner consistent with all relevant laws and regulations. We take necessary measures to ensure that personal information is correct and up to date. Personal information will only be used for the purpose of utilization and will not be disclosed to third parties (except our related parties e.g.: Administrators) without consent from the individual, except for justifiable grounds as required by laws and regulations.

We may collect various types of personal data from or about you, including:

Your name

Your user names and passwords

Contact information, including address, email address and/or telephone number

Information relating to your engagement with material that we publish or otherwise provide to you

Records of our interactions with you, including any messages you send us, your comments and questions and any other information you choose to provide.

The Company may automatically collect information about you from computer or internet browser through the use of cookies, pixel tags, and other similar technologies to enhance the user experience on its websites.

Third parties may be used to collect personal data and information indirectly through monitoring activities conducted by the Company or on its behalf.

Company does not knowingly collect personal data from anyone under the age of 18 and does not seek to collect or process sensitive information unless required or permitted by law and with express consent.

Uses of your Personal Data:

We may use your personal data for the purposes it was provided and in connection with our services as described below:

Provide products/services or info as requested or expected.

Fulfill agreements and facilitate business dealings.

Manage relationships, analyse websites and communications, and merge personal data for relevance.

Support and improve existing products/services, and plan/develop new ones.

Count/recognize website visitors and analyse usage.

To comply with and assess compliance with applicable laws, rules and regulations and internal policies and procedures.

Use information for any other purpose with consent.

Protection of Personal Information:

We provide thorough training to our officers and employees to prevent the leakage or inappropriate use of personal information and provide information on a need-to-know basis. Managers in charge for controls and inspections are appointed, and appropriate control systems are established to ensure the privacy and security of personal information.

In the event that personal information is provided to an external contractor (e.g.: Administrator), we take responsibility for ensuring that the external contractor has proper systems in place to protect the privacy of personal information.

Third parties disclosure of Personal Information:

Personal information held by us relating to an individual will be kept confidential but may be provided to third parties the following purpose:

Comply with applicable laws or legal processes.

Investigate and prevent illegal activity, fraud, or violations of terms and conditions.

Protect and defend legal rights or defend against legal claims.

Facilitate business or asset transactions, such as financing, mergers, acquisitions, or bankruptcy.

With our related parties (e.g.: administrators) that are subject to appropriate data protection obligations

Representatives, agents or custodians appointed by the client (e.g.: Auditors, accountant)

Retention of Personal Information:

Disclosure, correction and termination of usage shall be carried out upon request of an individual in accordance with relevant laws and regulations.

Personal information collected will be retained for no longer than is necessary for the fulfilment of the purposes for which it was collected as per applicable laws and regulations.

Rights of the Individual:

Under relevant laws and regulations, any individual has the right to request access to any of the personal data that we hold by submitting a written request. Individuals are also entitled to request to correct, cancel or delete any of the personal data we hold if they believe such information is inaccurate, out of date or we no longer have a legitimate interest or lawful justification to retain or process.

×

Disclaimer

Heyokha Brothers Limited is the issuer of this website and holds Type 4 (advising on securities) and Type 9 (asset management) licenses issued by the Securities and Futures Commission in Hong Kong.

The information provided on this website has been prepared solely for licensed intermediaries and qualified investors in Hong Kong, including professional investors, institutional investors, and accredited investors (as defined under the Securities and Futures Ordinance). The information provided on this website is for informational purposes only and should not be construed as investment advice, nor an offer to sell or a solicitation of an offer to buy any security, investment product, or service.

Investment involves risk and investors may lose their entire investment. Investors are advised to seek professional advice before making any investment decisions. Past performance is not indicative of future performance and the value of investments may fluctuate. Please refer to the offering document(s) for details, including the investment objectives, risk factors, and fees and charges.

Heyokha Brothers Limited reserves the right to amend, update, or remove any information on this website at any time without notice. By accessing and using this website, you agree to be bound by the above terms and conditions.