The Trojans, the story goes, had no idea. The horse looked like a gift, so they pulled it inside and celebrated, and by the time the soldiers climbed out it was far too late.

The modern re-run of that story, film director Christopher Nolan suggests, is stranger still.

Asked about artificial intelligence while promoting his new film The Odyssey, he offered an image we have not been able to shake: “AI is a Trojan horse that everybody knows the Greeks are inside. It’s a transparent horse. It’s made of glass. Everybody can see what’s going on inside of there.”

Source: hugodecryptegrandsformats Youtube

He added something sharper still: “I’ve never seen a technology advancing so rapidly that’s been so completely rejected by the public.”

Now, Nolan is a filmmaker, not an economist, and some of what he is reacting to is his own industry’s revolt against AI: the actors, writers and artists who watched it come for their work first and the “AI slop” it produces. But the people it comes for next look a lot like the rest of us.

Sit with what Nolan said for a second. This time the horse is see-through. The crowd can watch the soldiers loading their spears. And the crowd is cheering it through the gates regardless, because the people handing over the gift keep promising that what is inside is not an army but a golden age.

Maybe it is. We are not here to argue that AI is fake or feeble; betting against it has been a fast way to look foolish.

We are here to talk about the part nobody selling the horse wants to linger on: the gap between the day the soldiers climb out and the day the golden age is supposed to arrive.

The Valley Between Two Worlds

Peter Diamandis, who wrote a book literally called Abundance, is one of the great evangelists for the AI future. Even he does not pretend the road is smooth. He describes a stretch he calls “the chasm,” a period in which the old jobs vanish before the new prosperity shows up. He puts it at two to eight years.

Mo Gawdat, the former chief business officer of Google’s moonshot lab, thinks it is longer and darker, calling it a twelve to fifteen year “dystopia” before things get better.

How Mo Gawdat, former chief business officer of Google’s moonshot lab sees what will transpire moving forward

Here is the trouble with a chasm. How green does the far side have to be to justify the crossing? It does not matter how green it is if you cannot get across. Next decade’s abundance does not pay this month’s rent.

And the crossing, on the optimists’ own timelines, is measured not in months but in years. As one MIT study in 2025 found, 95% of companies deploying generative AI had yet to see any measurable return at all. The payoff is a promise. The disruption is already here.

So before we admire the far side, let us be honest about the valley.

Who Falls In First

The first wave is the one everyone pictures: routine, physical, blue-collar work. In the United States alone:

- Around 2.2 million people drive heavy trucks for a living, before you count couriers and ride-hailing drivers.

- Roughly 5 million work in food service.

- Close to 2.8 million staff call centres.

The machines are already here for them. Tesla and BYD have turned the car itself into a robot, and Elon Musk, whose trillion-dollar pay deal back in November 2025 is pegged to shipping a million humanoid Optimus robots, talked cheerfully about a world with more robots than people.

National Bureau of Economic Research on “ How Adaptable are American Workers to AI-Induced Job Displacement”?

The comforting reply has always been that the displaced will retrain into something better. But retrain into what, exactly? Not every laid-off truck driver becomes an AI engineer, and the internet does not need more influencers.

Then comes the part that is genuinely new, and the reason this is a middle-class story and not just a blue-collar one. The wave does not stop at the bottom of the ladder. It climbs.

As Gawdat lays it out, AI comes for the rungs we always assumed were safe:

- The paralegal.

- The financial analyst.

- The radiologist reading a scan.

- The graphic designer.

- Even the layer of middle management whose whole job was coordinating other people.

This is not a fringe worry.

Dario Amodei, the chief executive of Anthropic, warns that AI could wipe out half of all entry-level white-collar jobs and push unemployment to 10 to 20% within five years, with finance, law, consulting and tech first in line.

When the person building the thing is the one raising the alarm, it is worth taking the alarm more seriously than the sales pitch.

And here is the part that should stop you cold: it does not take mass unemployment to do real damage. Gawdat puts the threshold bluntly. “At 10 to 20% job displacement, you’re in a very different economy, an economy that is clearly spiraling downwards.”

Remember that consumer spending is close to 70% of the US economy. The workers being automated away are also the customers who buy what the economy makes. What happens to a business when the people it just replaced were also the people who bought its product?

You do not simply create an unemployment problem. You knock the legs out from under demand itself.

The Generation That Did Everything Right

You can already watch the chasm opening, if you know where to look. We sat through the clips from this year’s American graduation season, and they are something to behold. Students booed their own commencement speakers for daring to praise AI.

Eric Schmidt, the former chief executive of Google, was jeered at the University of Arizona.

Picture it: a generation that spent four years and a small fortune on a degree, booing the future being handed to them. It is easy to call that entitled. We think it is something closer to clear-eyed.

The cruelty is in the order of events. The bottom rung of the white-collar ladder, the entry-level job a graduate used to climb, is the first thing sawn off, stranding the people who did everything they were told to do.

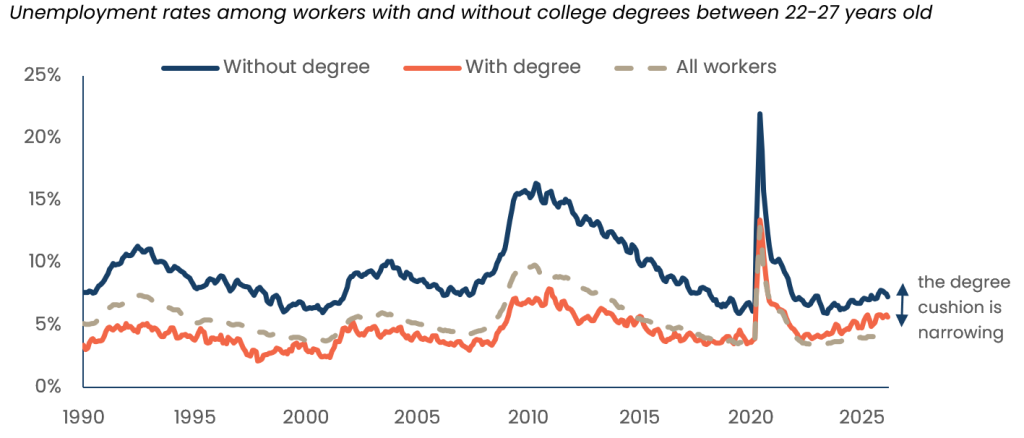

How will the youth get jobs? Even those with degrees are losing out

Source: U.S. Census Bureau and U.S. Bureau of Labor Statistics, Current Population Survey (IPUMS)

The Nobel laureate Geoffrey Hinton, often called the godfather of AI, framed the real fear better than any protest sign. The graduates, he suggests, are not frightened of the technology. They are frightened of the bargain: a system in which the gains flow to shareholders and the redundancy flows to them, with no net to catch the fall and no healthcare that is not tied to a job.

As Hinton puts it, AI “will make a few people much richer and most people poorer. That’s not AI’s fault, that is the capitalist system.”

That single sentence reframes the whole debate. The problem in the belly of the glass horse is not the machine. It is how we have decided to share what the machine produces. Gawdat says it plainly: “This is a distribution problem, not a technology one.”

China Cheers, America Boos

Here is where the view widens, because the same glass horse looks completely different depending on which gate it is rolling through.

A 2024 Ipsos survey of more than 23,000 people across 32 countries asked a simple question: do the benefits of AI outweigh the harms? The answers split the world almost neatly in two:

- China: 83% said yes.

- Indonesia: 80%.

- Thailand: 77%.

- United States: just 39%.

- The Netherlands, most fearful of all: 36%.

The Anglosphere are the most nervous for AI whereas Asia are most excited

Source: Ipsos

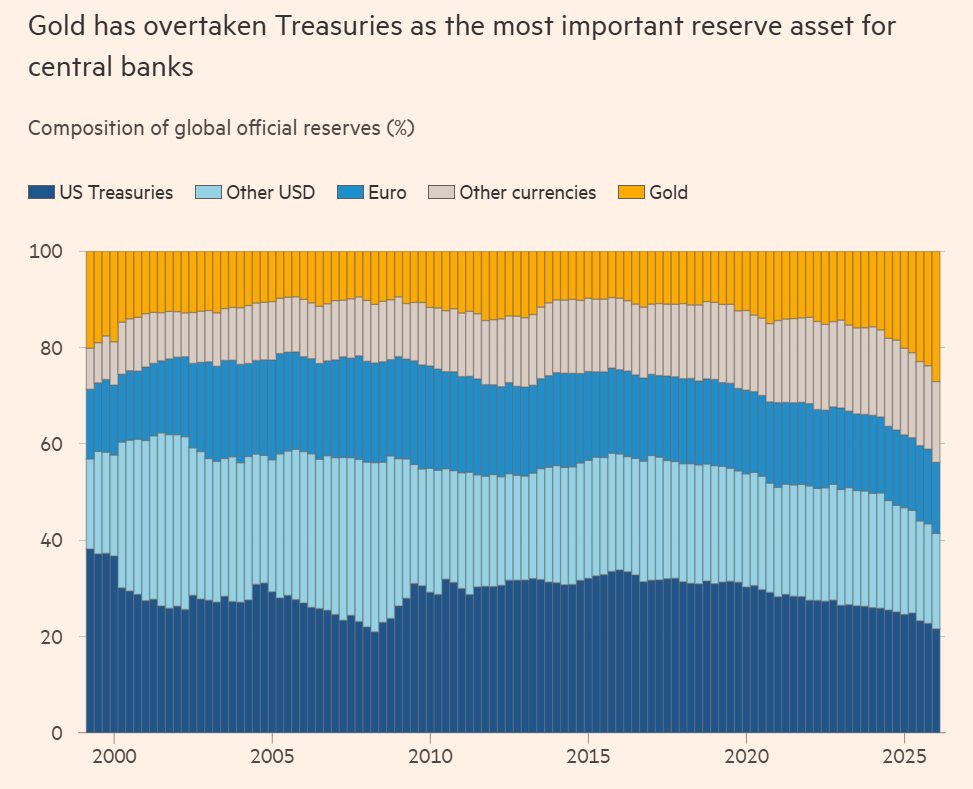

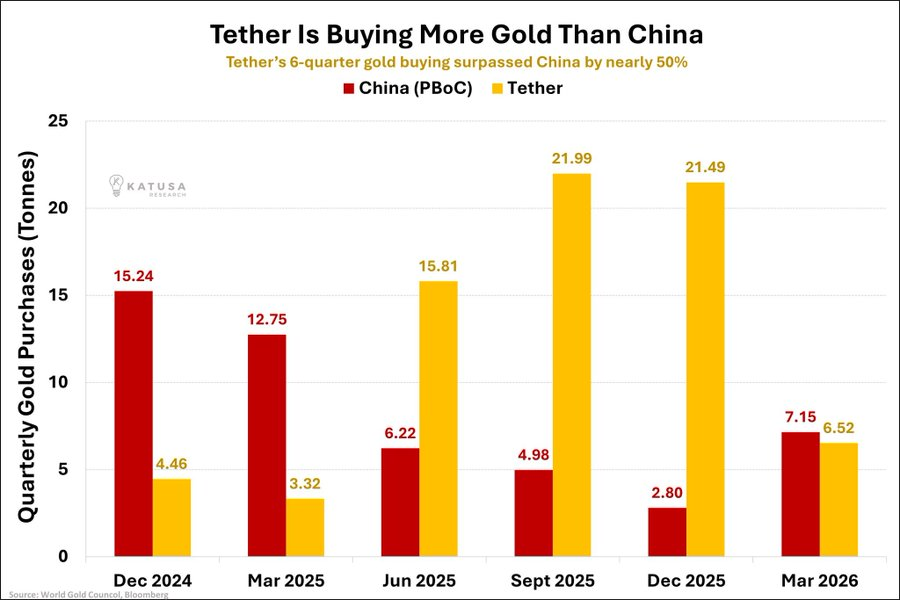

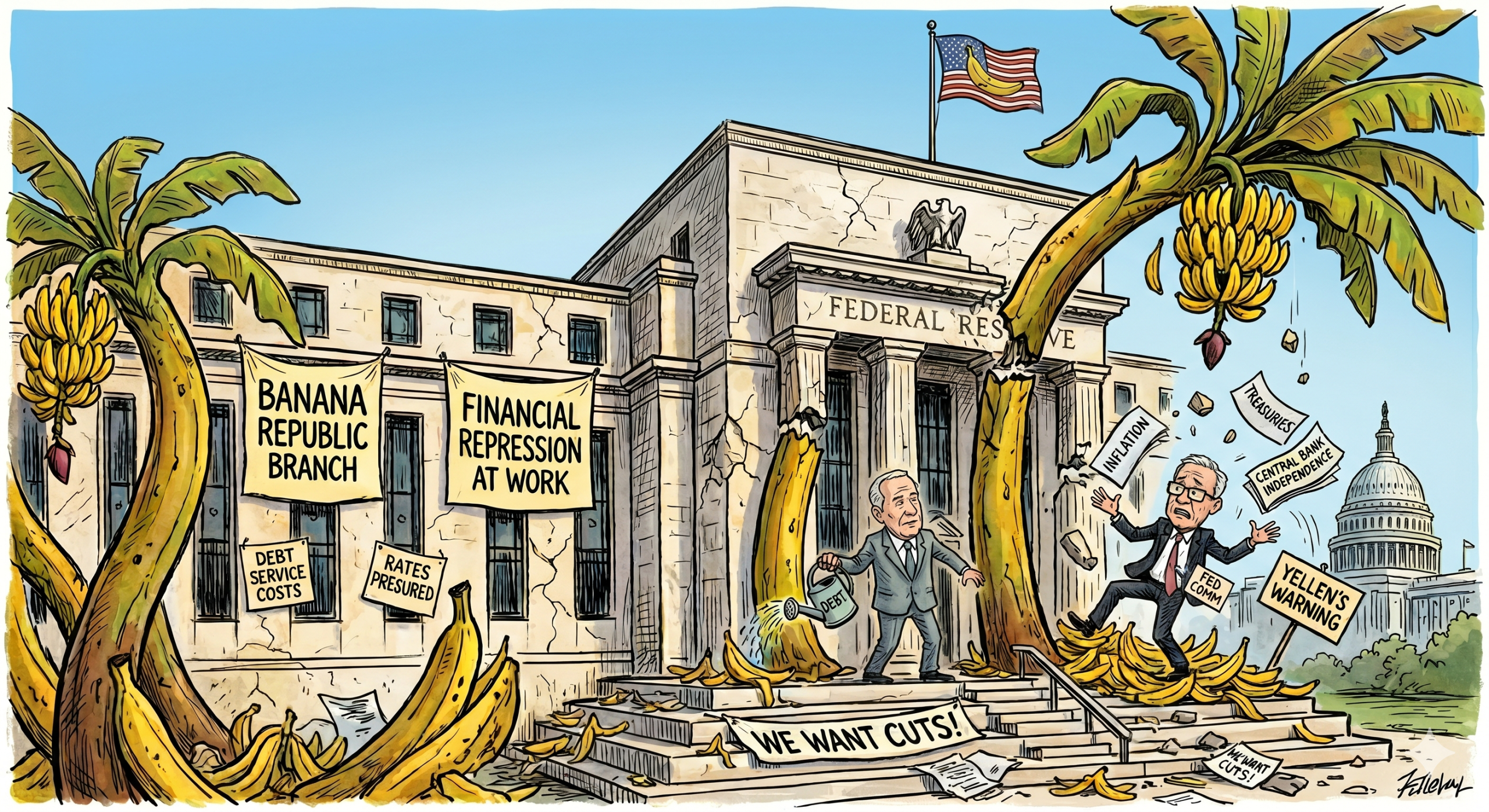

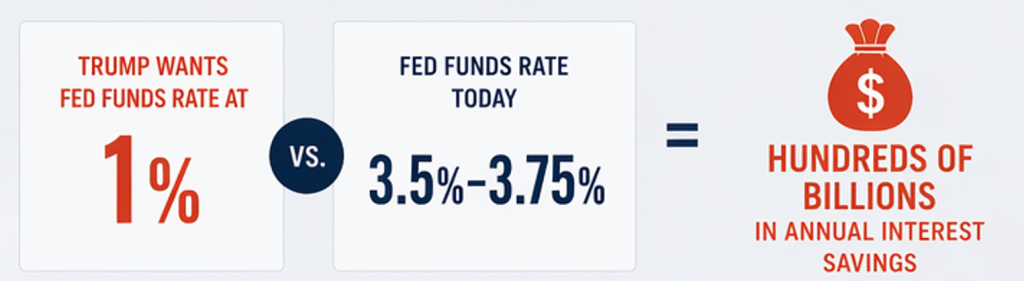

It is worth holding the two pictures side by side. A rising power, China, greets the new machine with 83% optimism, and at the very same time steadily swaps its dollars for gold.

A late-cycle power, the United States, fears the machine, cannot agree on how to share its spoils, and answers every shock by printing more of the very currency the rest of the world is quietly edging away from.

The technology is identical. Only the safety net differs.

Run the same automation through a society with universal healthcare and a real income floor, and losing your job to a robot is a setback rather than a catastrophe. America has no such cushion, so the displacement does not stay quiet.

It becomes an immediate demand to be made whole, and there is only one way a government in this fiscal position can meet that demand: off the printing press.

So the booing graduates and the money-printing turn out to be the same story told from opposite ends. A society that will not share the gains of automation through wages and taxes ends up redistributing them anyway, through inflation.

The Same Story We Always Tell

Step back far enough and something clicks into place. This is the same story we have been telling for years, only now seen from the inside.

The world is quietly losing faith in the dollar, and in paper money as a whole.

You can watch it in the one place that cannot spin a press release: central banks voting with their reserves, selling US Treasuries and buying gold. We tracked the retail end of that shift in “Gold out of Stock? But Still in Our Minds” the queues around the block in Asia; the central banks are now doing the same thing at scale.

That is the external symptom of an empire past its peak. And it does not arrive as one dramatic event.

It looks exactly like what we have been describing: a confident newcomer calmly accumulating real assets, while the incumbent debases its paper and argues with itself about who gets what.

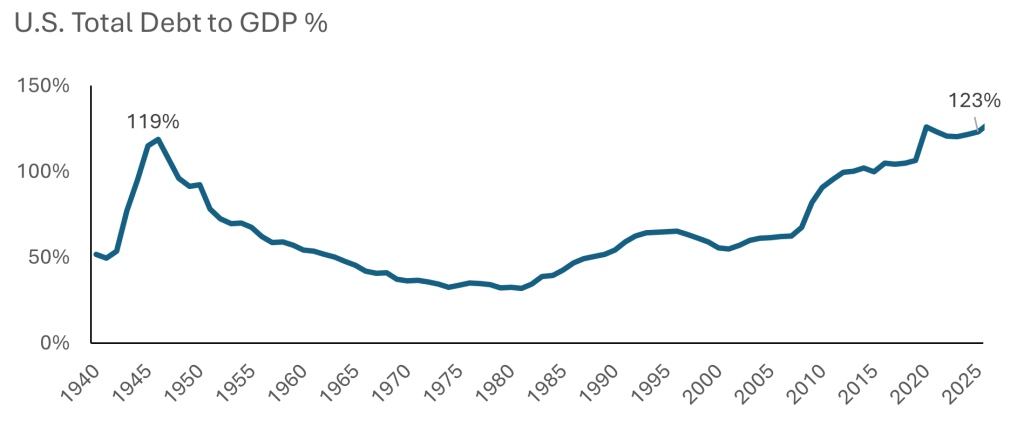

Ray Dalio has a name for this. He calls it the late stage of the long-term debt and empire cycle, the point where money-printing stops being a question of whether and becomes a question of when. Seen that way, AI is not the escape hatch from the cycle. On the evidence of its own graduates, it is the accelerant. It pulls the reckoning forward.

America looks to be heading downhill

Source: Ray Dalio

The Oldest Story There Is

Nolan chose The Odyssey for a reason. It is a three-thousand-year-old story, and we keep retelling it, in every language and every century, because underneath the sea monsters it is really a story about us. The tale does not change. Only the costumes do.

The loss of faith in a currency is that same kind of story.

It has played out in Rome, in Weimar, in a dozen empires that were each certain their paper was the exception.

The machine is new. The plot is ancient: a society is handed a gift it can all see through, refuses to share what the gift produces, papers over the anger by quietly printing money, and one day discovers the money itself is the thing people no longer trust. We argued in “Philosophy eats AI” that the hardest questions this technology raises are not technical but human. This is the hardest of them.

So what do we do with a horse we can all see through? Nolan’s own answer was not to smash it. “Technology”, he said, “is always going to give us great gifts, but it has to be viewed with skepticism, and the motives of the people giving it to us also have to be viewed with skepticism.”

Source: hugodecryptegrandsformats Youtube

Source: hugodecryptegrandsformats Youtube

It is a stance we share. Healthy skepticism is not fear of progress; it is simply insisting on the oldest and most useful questions there are: who gets the gains, who pays the cost, and how that cost gets paid.

The abundance may be real… But the danger was never that AI destroys every job. It is that the gains pool at the top, with the few who own the machines, while the strain spreads to everyone else. It does not have to erase the work to hollow out the middle. It only has to keep the winnings and pass down the losses.

The gift is genuine. So are the soldiers. Both things are true at once.

And a society that will not share the winnings through wages and taxes ends up sharing the losses anyway, through inflation. The bill always gets paid. So far, Washington keeps paying it at the printing press.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share

The Trojans, the story goes, had no idea. The horse looked like a gift, so they pulled it inside and celebrated, and by the time the soldiers climbed out it was far too late.

The modern re-run of that story, film director Christopher Nolan suggests, is stranger still.

Asked about artificial intelligence while promoting his new film The Odyssey, he offered an image we have not been able to shake: “AI is a Trojan horse that everybody knows the Greeks are inside. It’s a transparent horse. It’s made of glass. Everybody can see what’s going on inside of there.”

Source: hugodecryptegrandsformats Youtube

He added something sharper still: “I’ve never seen a technology advancing so rapidly that’s been so completely rejected by the public.”

Now, Nolan is a filmmaker, not an economist, and some of what he is reacting to is his own industry’s revolt against AI: the actors, writers and artists who watched it come for their work first and the “AI slop” it produces. But the people it comes for next look a lot like the rest of us.

Sit with what Nolan said for a second. This time the horse is see-through. The crowd can watch the soldiers loading their spears. And the crowd is cheering it through the gates regardless, because the people handing over the gift keep promising that what is inside is not an army but a golden age.

Maybe it is. We are not here to argue that AI is fake or feeble; betting against it has been a fast way to look foolish.

We are here to talk about the part nobody selling the horse wants to linger on: the gap between the day the soldiers climb out and the day the golden age is supposed to arrive.

The Valley Between Two Worlds

Peter Diamandis, who wrote a book literally called Abundance, is one of the great evangelists for the AI future. Even he does not pretend the road is smooth. He describes a stretch he calls “the chasm,” a period in which the old jobs vanish before the new prosperity shows up. He puts it at two to eight years.

Mo Gawdat, the former chief business officer of Google’s moonshot lab, thinks it is longer and darker, calling it a twelve to fifteen year “dystopia” before things get better.

How Mo Gawdat, former chief business officer of Google’s moonshot lab sees what will transpire moving forward

Here is the trouble with a chasm. How green does the far side have to be to justify the crossing? It does not matter how green it is if you cannot get across. Next decade’s abundance does not pay this month’s rent.

And the crossing, on the optimists’ own timelines, is measured not in months but in years. As one MIT study in 2025 found, 95% of companies deploying generative AI had yet to see any measurable return at all. The payoff is a promise. The disruption is already here.

So before we admire the far side, let us be honest about the valley.

Who Falls In First

The first wave is the one everyone pictures: routine, physical, blue-collar work. In the United States alone:

- Around 2.2 million people drive heavy trucks for a living, before you count couriers and ride-hailing drivers.

- Roughly 5 million work in food service.

- Close to 2.8 million staff call centres.

The machines are already here for them. Tesla and BYD have turned the car itself into a robot, and Elon Musk, whose trillion-dollar pay deal back in November 2025 is pegged to shipping a million humanoid Optimus robots, talked cheerfully about a world with more robots than people.

National Bureau of Economic Research on “ How Adaptable are American Workers to AI-Induced Job Displacement”?

The comforting reply has always been that the displaced will retrain into something better. But retrain into what, exactly? Not every laid-off truck driver becomes an AI engineer, and the internet does not need more influencers.

Then comes the part that is genuinely new, and the reason this is a middle-class story and not just a blue-collar one. The wave does not stop at the bottom of the ladder. It climbs.

As Gawdat lays it out, AI comes for the rungs we always assumed were safe:

- The paralegal.

- The financial analyst.

- The radiologist reading a scan.

- The graphic designer.

- Even the layer of middle management whose whole job was coordinating other people.

This is not a fringe worry.

Dario Amodei, the chief executive of Anthropic, warns that AI could wipe out half of all entry-level white-collar jobs and push unemployment to 10 to 20% within five years, with finance, law, consulting and tech first in line.

When the person building the thing is the one raising the alarm, it is worth taking the alarm more seriously than the sales pitch.

And here is the part that should stop you cold: it does not take mass unemployment to do real damage. Gawdat puts the threshold bluntly. “At 10 to 20% job displacement, you’re in a very different economy, an economy that is clearly spiraling downwards.”

Remember that consumer spending is close to 70% of the US economy. The workers being automated away are also the customers who buy what the economy makes. What happens to a business when the people it just replaced were also the people who bought its product?

You do not simply create an unemployment problem. You knock the legs out from under demand itself.

The Generation That Did Everything Right

You can already watch the chasm opening, if you know where to look. We sat through the clips from this year’s American graduation season, and they are something to behold. Students booed their own commencement speakers for daring to praise AI.

Eric Schmidt, the former chief executive of Google, was jeered at the University of Arizona.

Picture it: a generation that spent four years and a small fortune on a degree, booing the future being handed to them. It is easy to call that entitled. We think it is something closer to clear-eyed.

The cruelty is in the order of events. The bottom rung of the white-collar ladder, the entry-level job a graduate used to climb, is the first thing sawn off, stranding the people who did everything they were told to do.

How will the youth get jobs? Even those with degrees are losing out

Source: U.S. Census Bureau and U.S. Bureau of Labor Statistics, Current Population Survey (IPUMS)

The Nobel laureate Geoffrey Hinton, often called the godfather of AI, framed the real fear better than any protest sign. The graduates, he suggests, are not frightened of the technology. They are frightened of the bargain: a system in which the gains flow to shareholders and the redundancy flows to them, with no net to catch the fall and no healthcare that is not tied to a job.

As Hinton puts it, AI “will make a few people much richer and most people poorer. That’s not AI’s fault, that is the capitalist system.”

That single sentence reframes the whole debate. The problem in the belly of the glass horse is not the machine. It is how we have decided to share what the machine produces. Gawdat says it plainly: “This is a distribution problem, not a technology one.”

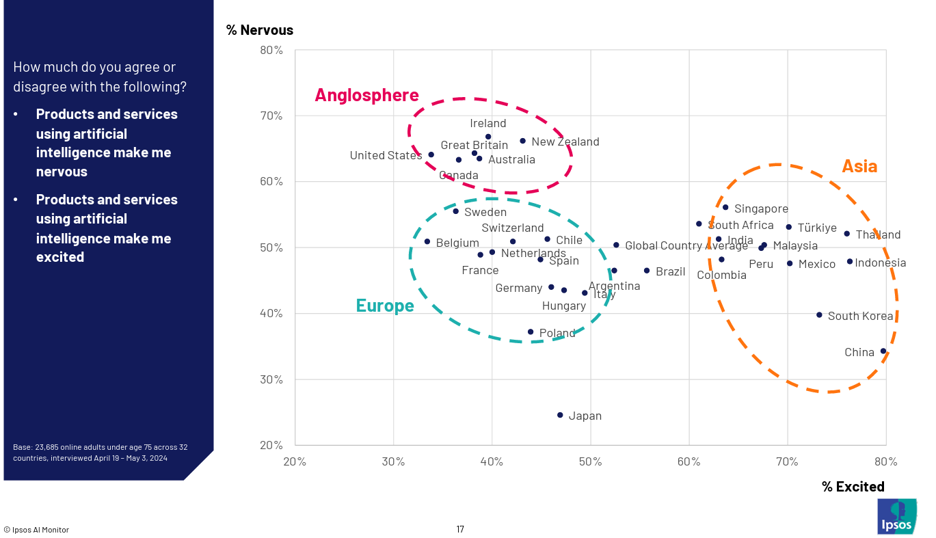

China Cheers, America Boos

Here is where the view widens, because the same glass horse looks completely different depending on which gate it is rolling through.

A 2024 Ipsos survey of more than 23,000 people across 32 countries asked a simple question: do the benefits of AI outweigh the harms? The answers split the world almost neatly in two:

- China: 83% said yes.

- Indonesia: 80%.

- Thailand: 77%.

- United States: just 39%.

- The Netherlands, most fearful of all: 36%.

The Anglosphere are the most nervous for AI whereas Asia are most excited

Source: Ipsos

It is worth holding the two pictures side by side. A rising power, China, greets the new machine with 83% optimism, and at the very same time steadily swaps its dollars for gold.

A late-cycle power, the United States, fears the machine, cannot agree on how to share its spoils, and answers every shock by printing more of the very currency the rest of the world is quietly edging away from.

The technology is identical. Only the safety net differs.

Run the same automation through a society with universal healthcare and a real income floor, and losing your job to a robot is a setback rather than a catastrophe. America has no such cushion, so the displacement does not stay quiet.

It becomes an immediate demand to be made whole, and there is only one way a government in this fiscal position can meet that demand: off the printing press.

So the booing graduates and the money-printing turn out to be the same story told from opposite ends. A society that will not share the gains of automation through wages and taxes ends up redistributing them anyway, through inflation.

The Same Story We Always Tell

Step back far enough and something clicks into place. This is the same story we have been telling for years, only now seen from the inside.

The world is quietly losing faith in the dollar, and in paper money as a whole.

You can watch it in the one place that cannot spin a press release: central banks voting with their reserves, selling US Treasuries and buying gold. We tracked the retail end of that shift in “Gold out of Stock? But Still in Our Minds” the queues around the block in Asia; the central banks are now doing the same thing at scale.

That is the external symptom of an empire past its peak. And it does not arrive as one dramatic event.

It looks exactly like what we have been describing: a confident newcomer calmly accumulating real assets, while the incumbent debases its paper and argues with itself about who gets what.

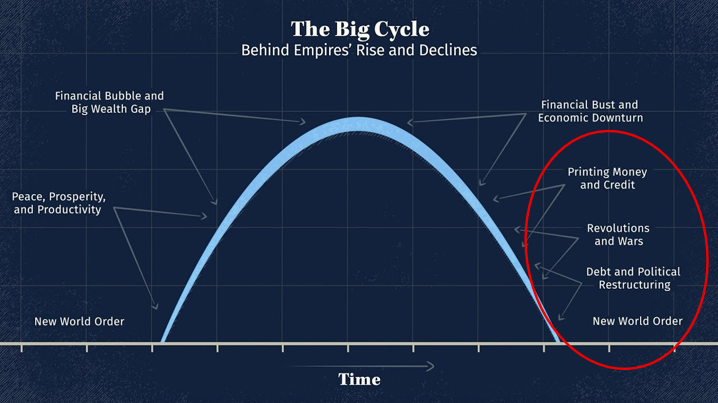

Ray Dalio has a name for this. He calls it the late stage of the long-term debt and empire cycle, the point where money-printing stops being a question of whether and becomes a question of when. Seen that way, AI is not the escape hatch from the cycle. On the evidence of its own graduates, it is the accelerant. It pulls the reckoning forward.

America looks to be heading downhill

Source: Ray Dalio

The Oldest Story There Is

Nolan chose The Odyssey for a reason. It is a three-thousand-year-old story, and we keep retelling it, in every language and every century, because underneath the sea monsters it is really a story about us. The tale does not change. Only the costumes do.

The loss of faith in a currency is that same kind of story.

It has played out in Rome, in Weimar, in a dozen empires that were each certain their paper was the exception.

The machine is new. The plot is ancient: a society is handed a gift it can all see through, refuses to share what the gift produces, papers over the anger by quietly printing money, and one day discovers the money itself is the thing people no longer trust. We argued in “Philosophy eats AI” that the hardest questions this technology raises are not technical but human. This is the hardest of them.

So what do we do with a horse we can all see through? Nolan’s own answer was not to smash it. “Technology”, he said, “is always going to give us great gifts, but it has to be viewed with skepticism, and the motives of the people giving it to us also have to be viewed with skepticism.”

Source: hugodecryptegrandsformats Youtube

It is a stance we share. Healthy skepticism is not fear of progress; it is simply insisting on the oldest and most useful questions there are: who gets the gains, who pays the cost, and how that cost gets paid.

The abundance may be real… But the danger was never that AI destroys every job. It is that the gains pool at the top, with the few who own the machines, while the strain spreads to everyone else. It does not have to erase the work to hollow out the middle. It only has to keep the winnings and pass down the losses.

The gift is genuine. So are the soldiers. Both things are true at once.

And a society that will not share the winnings through wages and taxes ends up sharing the losses anyway, through inflation. The bill always gets paid. So far, Washington keeps paying it at the printing press.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share

1988 comic ridiculing the Reserve Bank of New Zealand’s inflation prediction

1988 comic ridiculing the Reserve Bank of New Zealand’s inflation prediction The religion, live on air. First thing that appeared on our Bloomberg TV

The religion, live on air. First thing that appeared on our Bloomberg TV New Zealand started it first and others began to follow suit

New Zealand started it first and others began to follow suit Source: Fortune

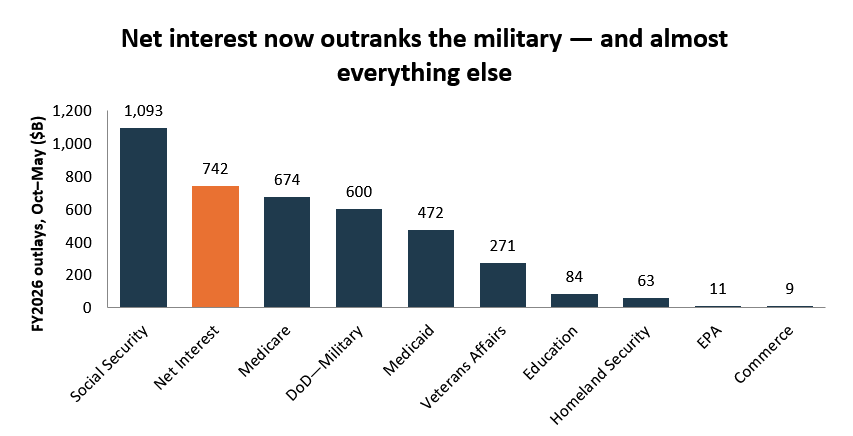

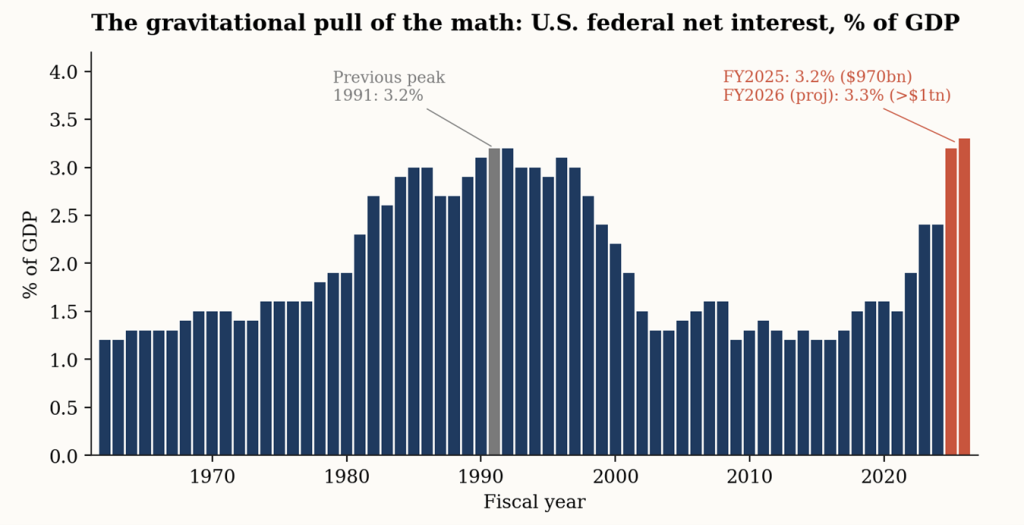

Source: Fortune Source: Congressional Budget Office

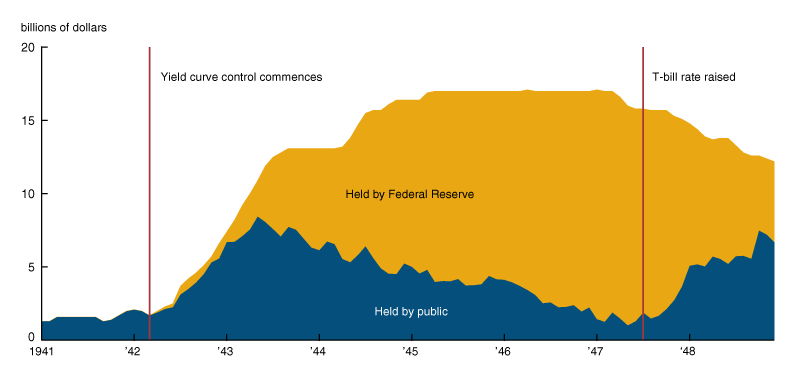

Source: Congressional Budget Office War bonds ads in the New York city subway back in the 1940s

War bonds ads in the New York city subway back in the 1940s

Source: Heyokha Research

Source: Heyokha Research Now it’s higher than WW2!

Now it’s higher than WW2! Source: Heyokha Research

Source: Heyokha Research