Yogyakarta

Admin heyokha

Share

Yogyakarta

Admin heyokha

Share

Yogyakarta

Share

Yogyakarta

Share

East Java

Share

East Java

Share

Sulawesi

Share

Sulawesi

Share

The early miles were filled with the sound of tires crunching on gravel and the chatter of fellow cyclists, all sharing the same ambitious goal. The terrain quickly becomes demanding, with steep climbs and sharp descents testing your legs and bike handling skills. The landscape stretches endlessly before you, offering breathtaking views of rolling hills, vast prairies, and the occasional wild animal companion.

As the miles accumulate, fatigue sets in. The sun beats down mercilessly, and the wind, sometimes a gentle nudge, other times a relentless force, adds to the challenge.

The loneliness of the open road is both daunting and liberating, giving you space to reflect on why you chose this challenge. The scenery, ever-changing yet consistently harsh, becomes a silent companion in your journey.

This is a common experience that extreme cyclists are all too familiar with.

In a world captivated by the grandeur of the Olympics and the Tour de France, it’s easy to overlook the extraordinary feats of endurance and resilience happening right in our backyard. Enter John Boemihardjo, an Indonesian cyclist whose journey embodies the indomitable human spirit. His story isn’t just a testament to perseverance; it’s a powerful parallel to the world of investments, where grit and strategy are key.

Then vs Now: John’s amazing health transformation

Initially weighing 103 kg, John dropped 28kg since starting to cycle

John’s journey into cycling began in 2013, under circumstances that would have deterred many. Diagnosed with a herniated disk and weighing 103 kg, he was advised by his chiropractor to take up cycling. What began as a health recommendation quickly morphed into a life-altering passion. John shed 28 kg, competed in his first race, and discovered a new zest for life. He has been unstoppable ever since.

With countless races under his belt, John’s recent feat in the East Java Journey this past March, an ultra-cycling event covering 1,500 km with a staggering 16,000 meters of elevation with a time limit of 156 hours stands out. He accomplished the course in just 101 hours, encompassing 4 full days and he shows no signs of stopping anytime soon.

East Java Journey, one of the hardest races John has ever done

The route spans across 4 cities of Surabaya, Madiun, Blitar, and Banyuwangi covering a total of 1500 km

Picture 1 (left): John with the backdrop of Mount Semeru

Picture 2 (right): full map course of the East Java Journey 1500

The Unbound Gravel race in America, one of the toughest gravel cycling events tested John. For context, it has a 43% DNF (Did Not Finish) rate given how difficult it is and John faced the challenge not once, but twice in 2021 and 2022!

Facing dehydration, mud, and the grueling task of hauling his bike through sludge, John’s relentless spirit shone through all 200 miles (320 km). He finished his 2022 race in just 13 hours and 34 minutes. Fast mortals typically finish in 12-16 hours and the majority nearly 20 hours long. On top of beating his previous year’s record of 16 hours and 13 minutes, he finished before sundown receiving the “Race the Sun” award. Talk about incredible growth!

Snapshots from the Unbound Gravel race in Kansas, United States

Bikers haul through the 200 mile route facing inclement weather, gravel, and dirt roads that can become mud roads

Image credits: Unbound Gravel website and Life Time

As of last week – John has also completed the Bentang Java race which encompasses the whole of Java island. This race is a more challenging route that is entirely self-navigated and unsupported, meaning no help or assistance from third parties including friends, relatives, family, acquaintances or even the local residents in any form. Cyclists have to rely on themselves and bring their own necessities including clothes, spare equipment, water, food, and medicine from the start of the race or purchase along the day.

John finished in just 4 days 12 hours 16 minutes, placing 5th! His journey for this recent race is one for the books. Facing stomach pains mid-way that led to a fever, John had to make the tough decision to take longer rest times to keep going. On top of that, he also had instances where he got lost due to surprising dead-ends and lack of road infrastructure. “At one point, there was no road or another instance where there was one but it was totally covered in banana trees!”, John recounted. Despite not surpassing his target of less than 4 days, John was all smiles by the end citing his spirit to keep pushing and the valuable lesson to have a plan B and C if plan A doesn’t work out.

Bentang Java, an unsupported and unguided tour across Java

Participants depart from the westernmost province of Banten all the way east ending at Banyuwangi

John finishing 5th place wearing his custom jersey with our Heyokha logo!

When asked about his most challenging moments, John’s response was telling. “The body wants to stop, but the mind wants to keep going,” he said. This battle between mind and body is not just a cycling challenge—it’s a metaphor for the investment world. In the face of market volatility or business setbacks, the ability to push forward and keep a long-term perspective is crucial.

John’s cycling adventures offer profound lessons for investments and business. The negative split strategy in cycling—pacing oneself in the first half and accelerating in the second—mirrors the patience needed in investing. It’s about staying calm during market lows and seizing opportunities during the highs.

His adaptability in the Unbound Gravel races and Bentang Java, switching between offensive and defensive tactics, echoes the dynamic decision-making required in investment management. Knowing when to take risks and when to hold back is a skill that translates directly from the track to the boardroom.

All smiles galore at the finish line

John and fellow cyclist Edo Bawono finishing Unbound Gravel 2022 beating the sunrise under 14 hours

John’s mantra, “Buang pikiran menyerah, dan biasakan finish what you have started”, which translates to “Discard thoughts of giving up and always finish what you start”, encapsulates a mindset that resonates deeply with us. The patience, persistence, and pain resistance that make John a phenomenal cyclist are the same traits that define successful investors. Challenges are inevitable, but a resilient spirit makes all the difference. At Heyokha Brothers, we embody this spirit—constantly challenging conventional thinking and adapting to change to provide unparalleled investment perspectives and solutions.

In our fast-paced digital age, it’s easy to become overly focused on outcomes, overlooking the intrinsic beauty of the process. John Boemihardjo’s journey offers a refreshing counterbalance—a return to real experiences and the great outdoors, which aligns closely with Heyokha’s investment philosophy. We’re committed to harmonizing the digital and physical realms, fostering a sense of togetherness through shared experiences. Whether it’s a local cycling club or a family hike, these activities bring people together, much like a well-played game of Monopoly—minus the inevitable family feud over who gets to be the banker.

John’s mantra isn’t just a slogan; it’s a way of life that resonates with us. His journey embodies the resilience of the human spirit—the ability to persevere, adapt, and thrive amidst challenges. This resilience is crucial not only in sports or investments but in all aspects of life. Investing without a sense of adventure is like cycling without a bike: you’re not going far! So, when you find yourself lost in the digital abyss, remember that there’s a whole world out there waiting to be explored. The best investments are often those that bring you back to what truly matters—living, laughing, and loving the journey.

Tara Mulia and Chloe Yu

Share

The early miles were filled with the sound of tires crunching on gravel and the chatter of fellow cyclists, all sharing the same ambitious goal. The terrain quickly becomes demanding, with steep climbs and sharp descents testing your legs and bike handling skills. The landscape stretches endlessly before you, offering breathtaking views of rolling hills, vast prairies, and the occasional wild animal companion.

As the miles accumulate, fatigue sets in. The sun beats down mercilessly, and the wind, sometimes a gentle nudge, other times a relentless force, adds to the challenge.

The loneliness of the open road is both daunting and liberating, giving you space to reflect on why you chose this challenge. The scenery, ever-changing yet consistently harsh, becomes a silent companion in your journey.

This is a common experience that extreme cyclists are all too familiar with.

In a world captivated by the grandeur of the Olympics and the Tour de France, it’s easy to overlook the extraordinary feats of endurance and resilience happening right in our backyard. Enter John Boemihardjo, an Indonesian cyclist whose journey embodies the indomitable human spirit. His story isn’t just a testament to perseverance; it’s a powerful parallel to the world of investments, where grit and strategy are key.

Then vs Now: John’s amazing health transformation

Initially weighing 103 kg, John dropped 28kg since starting to cycle

John’s journey into cycling began in 2013, under circumstances that would have deterred many. Diagnosed with a herniated disk and weighing 103 kg, he was advised by his chiropractor to take up cycling. What began as a health recommendation quickly morphed into a life-altering passion. John shed 28 kg, competed in his first race, and discovered a new zest for life. He has been unstoppable ever since.

With countless races under his belt, John’s recent feat in the East Java Journey this past March, an ultra-cycling event covering 1,500 km with a staggering 16,000 meters of elevation with a time limit of 156 hours stands out. He accomplished the course in just 101 hours, encompassing 4 full days and he shows no signs of stopping anytime soon.

East Java Journey, one of the hardest races John has ever done

The route spans across 4 cities of Surabaya, Madiun, Blitar, and Banyuwangi covering a total of 1500 km

Picture 1 (left): John with the backdrop of Mount Semeru

Picture 2 (right): full map course of the East Java Journey 1500

The Unbound Gravel race in America, one of the toughest gravel cycling events tested John. For context, it has a 43% DNF (Did Not Finish) rate given how difficult it is and John faced the challenge not once, but twice in 2021 and 2022!

Facing dehydration, mud, and the grueling task of hauling his bike through sludge, John’s relentless spirit shone through all 200 miles (320 km). He finished his 2022 race in just 13 hours and 34 minutes. Fast mortals typically finish in 12-16 hours and the majority nearly 20 hours long. On top of beating his previous year’s record of 16 hours and 13 minutes, he finished before sundown receiving the “Race the Sun” award. Talk about incredible growth!

Snapshots from the Unbound Gravel race in Kansas, United States

Bikers haul through the 200 mile route facing inclement weather, gravel, and dirt roads that can become mud roads

Image credits: Unbound Gravel website and Life Time

As of last week – John has also completed the Bentang Java race which encompasses the whole of Java island. This race is a more challenging route that is entirely self-navigated and unsupported, meaning no help or assistance from third parties including friends, relatives, family, acquaintances or even the local residents in any form. Cyclists have to rely on themselves and bring their own necessities including clothes, spare equipment, water, food, and medicine from the start of the race or purchase along the day.

John finished in just 4 days 12 hours 16 minutes, placing 5th! His journey for this recent race is one for the books. Facing stomach pains mid-way that led to a fever, John had to make the tough decision to take longer rest times to keep going. On top of that, he also had instances where he got lost due to surprising dead-ends and lack of road infrastructure. “At one point, there was no road or another instance where there was one but it was totally covered in banana trees!”, John recounted. Despite not surpassing his target of less than 4 days, John was all smiles by the end citing his spirit to keep pushing and the valuable lesson to have a plan B and C if plan A doesn’t work out.

Bentang Java, an unsupported and unguided tour across Java

Participants depart from the westernmost province of Banten all the way east ending at Banyuwangi

John finishing 5th place wearing his custom jersey with our Heyokha logo!

When asked about his most challenging moments, John’s response was telling. “The body wants to stop, but the mind wants to keep going,” he said. This battle between mind and body is not just a cycling challenge—it’s a metaphor for the investment world. In the face of market volatility or business setbacks, the ability to push forward and keep a long-term perspective is crucial.

John’s cycling adventures offer profound lessons for investments and business. The negative split strategy in cycling—pacing oneself in the first half and accelerating in the second—mirrors the patience needed in investing. It’s about staying calm during market lows and seizing opportunities during the highs.

His adaptability in the Unbound Gravel races and Bentang Java, switching between offensive and defensive tactics, echoes the dynamic decision-making required in investment management. Knowing when to take risks and when to hold back is a skill that translates directly from the track to the boardroom.

All smiles galore at the finish line

John and fellow cyclist Edo Bawono finishing Unbound Gravel 2022 beating the sunrise under 14 hours

John’s mantra, “Buang pikiran menyerah, dan biasakan finish what you have started”, which translates to “Discard thoughts of giving up and always finish what you start”, encapsulates a mindset that resonates deeply with us. The patience, persistence, and pain resistance that make John a phenomenal cyclist are the same traits that define successful investors. Challenges are inevitable, but a resilient spirit makes all the difference. At Heyokha Brothers, we embody this spirit—constantly challenging conventional thinking and adapting to change to provide unparalleled investment perspectives and solutions.

In our fast-paced digital age, it’s easy to become overly focused on outcomes, overlooking the intrinsic beauty of the process. John Boemihardjo’s journey offers a refreshing counterbalance—a return to real experiences and the great outdoors, which aligns closely with Heyokha’s investment philosophy. We’re committed to harmonizing the digital and physical realms, fostering a sense of togetherness through shared experiences. Whether it’s a local cycling club or a family hike, these activities bring people together, much like a well-played game of Monopoly—minus the inevitable family feud over who gets to be the banker.

John’s mantra isn’t just a slogan; it’s a way of life that resonates with us. His journey embodies the resilience of the human spirit—the ability to persevere, adapt, and thrive amidst challenges. This resilience is crucial not only in sports or investments but in all aspects of life. Investing without a sense of adventure is like cycling without a bike: you’re not going far! So, when you find yourself lost in the digital abyss, remember that there’s a whole world out there waiting to be explored. The best investments are often those that bring you back to what truly matters—living, laughing, and loving the journey.

Tara Mulia and Chloe Yu

Share

Amidst a surge of negative headlines in the Western press, Indonesia’s nickel revolution is transforming the global EV supply chain. This comprehensive report delves into whether these criticisms hold any truth or if they are simply tactics by competitors to undermine Indonesia’s growth. By examining advanced technologies like High-Pressure Acid Leach (HPAL) and highlighting significant investments from both Chinese and Western companies, we uncover the real story of how Indonesia is not only meeting global nickel demand but leading in sustainable mining practices. Dive in to explore the facts and debunk the myths surrounding this pivotal industry shift.

Share

Amidst a surge of negative headlines in the Western press, Indonesia’s nickel revolution is transforming the global EV supply chain. This comprehensive report delves into whether these criticisms hold any truth or if they are simply tactics by competitors to undermine Indonesia’s growth. By examining advanced technologies like High-Pressure Acid Leach (HPAL) and highlighting significant investments from both Chinese and Western companies, we uncover the real story of how Indonesia is not only meeting global nickel demand but leading in sustainable mining practices. Dive in to explore the facts and debunk the myths surrounding this pivotal industry shift.

Share

How do we 16x our wealth? Easy. Invest in a fund that returns 20% YoY, for 20 years.

How do we 1000x our wealth? Surprisingly, as easy. Invest in the same fund, but for 50 years.

Then the ultimate question is: How do we increase our lifespan by 30 years? Very. Simple.

At our office, the concept of longevity has become a hot topic of conversation. Inspired by Peter Attia’s “Outlive: The Science and Art of Longevity” and Dave Asprey’s “Superhuman: The Bulletproof Plan to Age Backward and Maybe Even Live Forever,” we have embarked on a journey to enhance our health and extend our lives. One key takeaway from our research has been the importance of probiotics, which led us to the world of kombucha brewing. Interestingly, we discovered that the principles behind kombucha and investing are strikingly similar, especially regarding the power of compounding.

Kombucha, the fermented tea known for its health benefits, undergoes a transformation during fermentation, similar to how investments grow through compounding. The process begins with tea, sugar, and a SCOBY (Symbiotic Culture Of Bacteria and Yeast). As the microorganisms break down the sugar, they produce organic acids, vitamins, and probiotics, enhancing the drink’s flavour and nutritional profile over time. The longer the fermentation, the richer the flavour, mirroring how investments grow over time.

In investing, compounding involves reinvesting earnings to generate more earnings. Small initial investments can grow substantially as returns are reinvested, much like how a snowball gathers more snow as it rolls downhill. The key to both successful kombucha brewing and investing is patience and consistency. Regular additions of sugar fuel kombucha’s fermentation, just as regular contributions maximize investment growth. Finding “The Compounders”, companies that grow and reallocate their capital to grow the company even bigger, is key to investment success over time.

A unique aspect of kombucha brewing is the exponential multiplication of the SCOBY, which produces new layers with each batch, doubling brewing capacity. This mirrors reinvested earnings in a portfolio, leading to exponential growth. Both processes require careful monitoring and adjustments. In kombucha brewing, you adjust fermentation time and ingredients; in investing, you review and rebalance your portfolio – or we can do it for you anyways.

The principles of patience, consistency, and careful management in kombucha brewing and investing lead to rewarding outcomes. Embracing these principles can result in both a delightful beverage and a robust financial future, illustrating that the most satisfying results come from time, care, and thoughtful effort.

p.s. come by our office and try our delightful kombucha!

Long Live,

Danzel Aryo Soerjohadi

Share

How do we 16x our wealth? Easy. Invest in a fund that returns 20% YoY, for 20 years.

How do we 1000x our wealth? Surprisingly, as easy. Invest in the same fund, but for 50 years.

Then the ultimate question is: How do we increase our lifespan by 30 years? Very. Simple.

At our office, the concept of longevity has become a hot topic of conversation. Inspired by Peter Attia’s “Outlive: The Science and Art of Longevity” and Dave Asprey’s “Superhuman: The Bulletproof Plan to Age Backward and Maybe Even Live Forever,” we have embarked on a journey to enhance our health and extend our lives. One key takeaway from our research has been the importance of probiotics, which led us to the world of kombucha brewing. Interestingly, we discovered that the principles behind kombucha and investing are strikingly similar, especially regarding the power of compounding.

Kombucha, the fermented tea known for its health benefits, undergoes a transformation during fermentation, similar to how investments grow through compounding. The process begins with tea, sugar, and a SCOBY (Symbiotic Culture Of Bacteria and Yeast). As the microorganisms break down the sugar, they produce organic acids, vitamins, and probiotics, enhancing the drink’s flavour and nutritional profile over time. The longer the fermentation, the richer the flavour, mirroring how investments grow over time.

In investing, compounding involves reinvesting earnings to generate more earnings. Small initial investments can grow substantially as returns are reinvested, much like how a snowball gathers more snow as it rolls downhill. The key to both successful kombucha brewing and investing is patience and consistency. Regular additions of sugar fuel kombucha’s fermentation, just as regular contributions maximize investment growth. Finding “The Compounders”, companies that grow and reallocate their capital to grow the company even bigger, is key to investment success over time.

A unique aspect of kombucha brewing is the exponential multiplication of the SCOBY, which produces new layers with each batch, doubling brewing capacity. This mirrors reinvested earnings in a portfolio, leading to exponential growth. Both processes require careful monitoring and adjustments. In kombucha brewing, you adjust fermentation time and ingredients; in investing, you review and rebalance your portfolio – or we can do it for you anyways.

The principles of patience, consistency, and careful management in kombucha brewing and investing lead to rewarding outcomes. Embracing these principles can result in both a delightful beverage and a robust financial future, illustrating that the most satisfying results come from time, care, and thoughtful effort.

p.s. come by our office and try our delightful kombucha!

Long Live,

Danzel Aryo Soerjohadi

Share

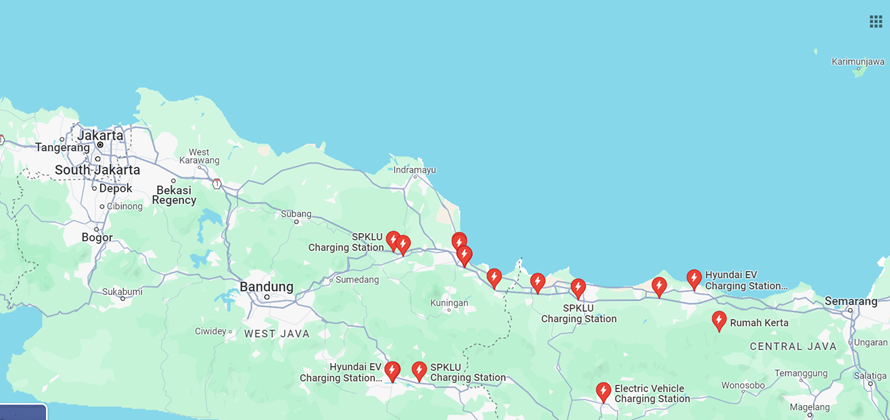

Indonesia’s journey towards an energy transition, particularly with the adoption of electric vehicles (EVs), has been met with a fair share of skepticism. Concerns about the availability of charging stations, the cost-efficiency of EVs, and the overall practicality of long-distance travel in an EV have loomed large. However, our recent road round trip from Jakarta to Semarang which is around 400km one way pleasantly surprised us, casting away many of those doubts. Here’s a recount of our electrifying adventure that proved the naysayers wrong.

Charging stations aplenty from Jakarta to Semarang

Bird eye view of several charging stations by the National Electric Company along the toll roads

Starting at 5:30am from our office with a fully charged battery and a sense of adventure, we were ready to begin. Mind you, this was our first time taking our EV, a Hyundai Ioniq 5, to a trip this far and long so we were cautiously optimistic. Leaving at the break of dawn has its perks namely avoiding the notorious Jakarta traffic jam. Whizzing past several rest areas, we were able to spot almost if not all had the electric sign logos on their billboards showing EV charging station availability. Fortune was on our side.

With rest areas aplenty by the toll roads, our first leg of the journey took us to the midpoint at the KM 228A rest area. We covered 243 km in under 3 hours at 80-110 km/h with a battery life of 50% remaining. Upon first glance, the charging stations were clear to locate and readily available with no lines. We charged 35,77 kWh for Rp 96,000 in just 54 minutes – the perfect amount of time for a leisurely breakfast.

Jakarta to our first charging station rest area

Location: SPKLU KM 228A rest area

By 10am, we were back on the road and reached Semarang by 12pm. This leg of the trip covered 201 km and took around 2 hours and 14 minutes. Traffic thinned out at this point and we were able to speed up to 140 km/h in the hot weather, leaving the battery at 41%.

Our next pit stop was at the PLN office in Semarang, where we juiced up 47,80 kWh for Rp 130,000 in 59 minutes. This charging station went above and beyond with its offerings including a lounge with full air conditioning, television, lounge chairs, and a coffee vending machine. With free amenities such as these, road tripping has never felt so easy.

Luxury at its finest in an EV charging station out of all places

Location: SPKLU PLN UID Central Java & DIY

All recharged both body and vehicle, we headed to the Padma Hotel to situate for the night. When parking, the hotel lot itself offered 2-3 AC type charging stations and several other EV cars were also at the ready to charge. It appears that EV cars are continuing to grow its interest even all the way in Semarang.

We spent the next day exploring the city. For readers who have never been, Semarang is the capital and largest city of Central Java, rich with history of being a major port during the Dutch colonial era. Walking around Old Town, well-preserved Dutch colonial buildings and antique shops lined the streets transporting you back in time. Its historical port has made Semarang to be a melting pot of Chinese, Indian Arab, and European culture as well, lending an abundant variety of charm and heritage on every street corner.

Gorgeous historical charm of Semarang

Photo credits: IG @sutanto.harsono and Wuddy Warsono

We headed to the city center for lunch and were greeted with a plethora of delicious local cuisine at the D’Kambodja Heritage restaurant. With its location being a cultural heritage building, we found that the interior blended Indonesian Dutch Chinese architecture lended a refreshing revitalized modern twist. Javanese ornaments and colorful flowers dripped from the ceiling, bringing a vibrant atmosphere to complement the “buffet style” of local dishes that will leave your mouth watering.

A feast of colors for the eyes and stomach

The D’Kambodja Heritage restaurant was opened by Anne Avantie, famed fashion designer who modernized the kebaya (traditional Indonesian long sleeve garment).

Our hunger for local eats and thirst for history appeased, we headed to meet with local businesses. Having spoken with those in various sectors, we found that businesses in Central Java is thriving. This is largely due to the relocations of many factories from West Java into the central region, driven mainly from a desire to capitalize on the region’s lower wages. We had the opportunity to also visit the Grand Batang City, the new industrial park for infrastructure development. Although the area is still under construction, the potential for growth is evident. Tangible growth can be seen in Central Java through these new businesses and initiatives, promising an exciting economic boom.

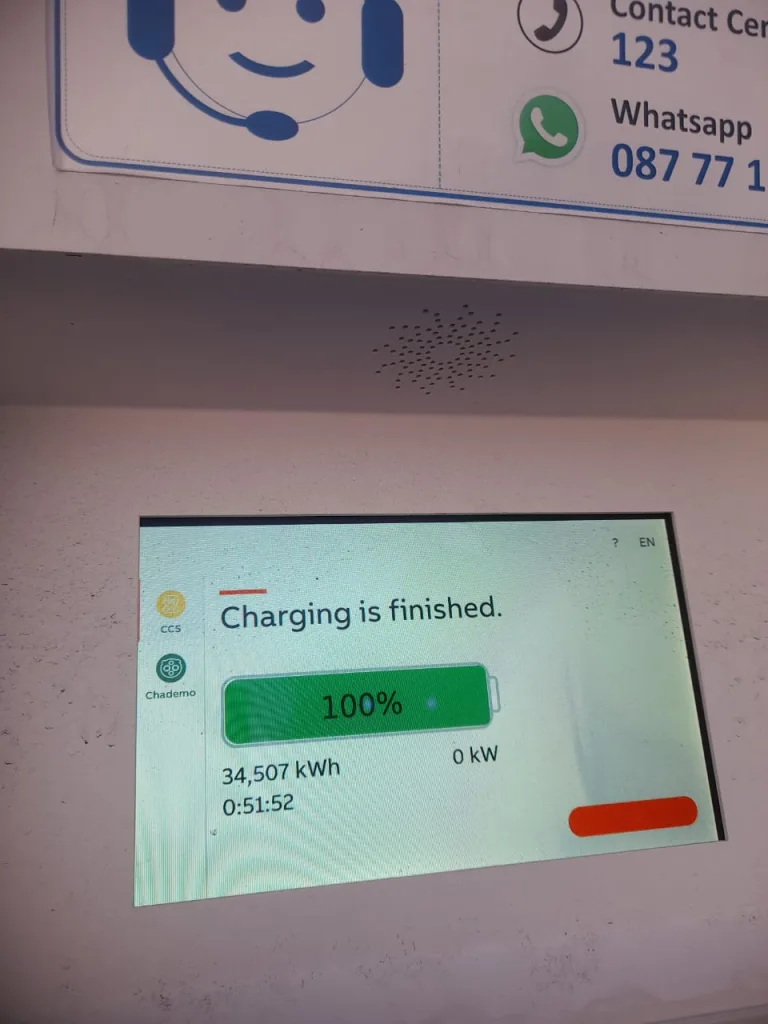

It was with this exciting sentiment that we made our way to one last charging station before starting our journey back to Jakarta. This rest area costing Rp 95,000 for 34.5 kWh and took 53 minutes to fully charge. Once again, easy to find and locate with no lines to wait behind. The premises themselves are clean and charging features easy to navigate ourselves.

Laying the groundwork: new industrial structures in the making

First picture: Alderon Factory (IMPC group)

Second and third picture: ongoing structures being built

It was with this exciting sentiment that we made our way to one last charging station before starting our journey back to Jakarta. This rest area costing Rp 95,000 for 34.5 kWh and took 53 minutes to fully charge. Once again, easy to find and locate with no lines to wait behind. The premises themselves are clean and charging features easy to navigate ourselves.

Our last pit stop before heading back home

Location: SPKLU KM 360 B Toll Batang – Semarang rest area

The total trip from Jakarta to Semarang and back roughly covered 900 km, which only needed 3 pit stops to charge the car and were a breeze to locate. At an average cost of Rp 2,727 per kWh, we spent a total of Rp 321,966 to and back. Compared to a gas car, we estimate it would have roughly costed around a whopping Rp 1,106,250 for the same distance. Our wallets were crying in relief.

Electric cars are a win for your wallet

Semarang offered convenient charging options, including the Padma Hotel’s AC stations and numerous AC and DC stations along the toll roads. We counted around 9-10 EV charging stations between Jakarta and Semarang, none of which were crowded. Should EV interest surge, we do think there would be a growing need for more charging stations. This trip is also a testament proving that EVs are not only cost-effective but also comparable in travel time to gasoline cars. EVs are not only kind to the planet but also to the pocket, matching gasoline cars in travel time while delivering significant savings. With this electrifying adventure, the future of travel is bright, efficient, and definitely more affordable.

Drive electric, save green: both the planet and your wallet will thank you!

Tara Mulia

Share

Indonesia’s journey towards an energy transition, particularly with the adoption of electric vehicles (EVs), has been met with a fair share of skepticism. Concerns about the availability of charging stations, the cost-efficiency of EVs, and the overall practicality of long-distance travel in an EV have loomed large. However, our recent road round trip from Jakarta to Semarang which is around 400km one way pleasantly surprised us, casting away many of those doubts. Here’s a recount of our electrifying adventure that proved the naysayers wrong.

Charging stations aplenty from Jakarta to Semarang

Bird eye view of several charging stations by the National Electric Company along the toll roads

Starting at 5:30am from our office with a fully charged battery and a sense of adventure, we were ready to begin. Mind you, this was our first time taking our EV, a Hyundai Ioniq 5, to a trip this far and long so we were cautiously optimistic. Leaving at the break of dawn has its perks namely avoiding the notorious Jakarta traffic jam. Whizzing past several rest areas, we were able to spot almost if not all had the electric sign logos on their billboards showing EV charging station availability. Fortune was on our side.

With rest areas aplenty by the toll roads, our first leg of the journey took us to the midpoint at the KM 228A rest area. We covered 243 km in under 3 hours at 80-110 km/h with a battery life of 50% remaining. Upon first glance, the charging stations were clear to locate and readily available with no lines. We charged 35,77 kWh for Rp 96,000 in just 54 minutes – the perfect amount of time for a leisurely breakfast.

Jakarta to our first charging station rest area

Location: SPKLU KM 228A rest area

By 10am, we were back on the road and reached Semarang by 12pm. This leg of the trip covered 201 km and took around 2 hours and 14 minutes. Traffic thinned out at this point and we were able to speed up to 140 km/h in the hot weather, leaving the battery at 41%.

Our next pit stop was at the PLN office in Semarang, where we juiced up 47,80 kWh for Rp 130,000 in 59 minutes. This charging station went above and beyond with its offerings including a lounge with full air conditioning, television, lounge chairs, and a coffee vending machine. With free amenities such as these, road tripping has never felt so easy.

Luxury at its finest in an EV charging station out of all places

Location: SPKLU PLN UID Central Java & DIY

All recharged both body and vehicle, we headed to the Padma Hotel to situate for the night. When parking, the hotel lot itself offered 2-3 AC type charging stations and several other EV cars were also at the ready to charge. It appears that EV cars are continuing to grow its interest even all the way in Semarang.

We spent the next day exploring the city. For readers who have never been, Semarang is the capital and largest city of Central Java, rich with history of being a major port during the Dutch colonial era. Walking around Old Town, well-preserved Dutch colonial buildings and antique shops lined the streets transporting you back in time. Its historical port has made Semarang to be a melting pot of Chinese, Indian Arab, and European culture as well, lending an abundant variety of charm and heritage on every street corner.

Gorgeous historical charm of Semarang

Photo credits: IG @sutanto.harsono and Wuddy Warsono

We headed to the city center for lunch and were greeted with a plethora of delicious local cuisine at the D’Kambodja Heritage restaurant. With its location being a cultural heritage building, we found that the interior blended Indonesian Dutch Chinese architecture lended a refreshing revitalized modern twist. Javanese ornaments and colorful flowers dripped from the ceiling, bringing a vibrant atmosphere to complement the “buffet style” of local dishes that will leave your mouth watering.

A feast of colors for the eyes and stomach

The D’Kambodja Heritage restaurant was opened by Anne Avantie, famed fashion designer who modernized the kebaya (traditional Indonesian long sleeve garment).

Our hunger for local eats and thirst for history appeased, we headed to meet with local businesses. Having spoken with those in various sectors, we found that businesses in Central Java is thriving. This is largely due to the relocations of many factories from West Java into the central region, driven mainly from a desire to capitalize on the region’s lower wages. We had the opportunity to also visit the Grand Batang City, the new industrial park for infrastructure development. Although the area is still under construction, the potential for growth is evident. Tangible growth can be seen in Central Java through these new businesses and initiatives, promising an exciting economic boom.

It was with this exciting sentiment that we made our way to one last charging station before starting our journey back to Jakarta. This rest area costing Rp 95,000 for 34.5 kWh and took 53 minutes to fully charge. Once again, easy to find and locate with no lines to wait behind. The premises themselves are clean and charging features easy to navigate ourselves.

Laying the groundwork: new industrial structures in the making

First picture: Alderon Factory (IMPC group)

Second and third picture: ongoing structures being built

It was with this exciting sentiment that we made our way to one last charging station before starting our journey back to Jakarta. This rest area costing Rp 95,000 for 34.5 kWh and took 53 minutes to fully charge. Once again, easy to find and locate with no lines to wait behind. The premises themselves are clean and charging features easy to navigate ourselves.

Our last pit stop before heading back home

Location: SPKLU KM 360 B Toll Batang – Semarang rest area

The total trip from Jakarta to Semarang and back roughly covered 900 km, which only needed 3 pit stops to charge the car and were a breeze to locate. At an average cost of Rp 2,727 per kWh, we spent a total of Rp 321,966 to and back. Compared to a gas car, we estimate it would have roughly costed around a whopping Rp 1,106,250 for the same distance. Our wallets were crying in relief.

Electric cars are a win for your wallet

Semarang offered convenient charging options, including the Padma Hotel’s AC stations and numerous AC and DC stations along the toll roads. We counted around 9-10 EV charging stations between Jakarta and Semarang, none of which were crowded. Should EV interest surge, we do think there would be a growing need for more charging stations. This trip is also a testament proving that EVs are not only cost-effective but also comparable in travel time to gasoline cars. EVs are not only kind to the planet but also to the pocket, matching gasoline cars in travel time while delivering significant savings. With this electrifying adventure, the future of travel is bright, efficient, and definitely more affordable.

Drive electric, save green: both the planet and your wallet will thank you!

Tara Mulia

Share

“Investing in EMs in the past decade is like preparing for a firework show that ends with a single sparkler—underwhelming and disappointing.”

We’re all familiar with the conversations above, albeit in different forms. Just mention “EM (Emerging Market) equity” at a cocktail party, and you’ll see people quickly finishing their drinks and changing the subject to US market investing. Could this be a classic example of Peter Lynch’s cocktail party theory, indicating that the market is bottoming out?

Beyond the liquor

In “One Up on Wall Street,” Peter Lynch identified cocktail party conversations as a significant contrarian market indicator. When people avoid discussing certain investments, it’s often a sign that the market is bottoming, presenting an opportunity to find undervalued stocks. Conversely, when such gatherings are filled with investment tips and general euphoria, it typically signals that the market is peaking and a downturn may be imminent.

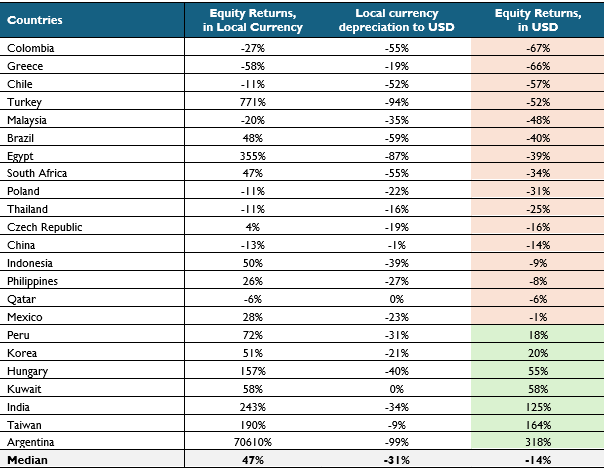

The following table below showcases why people have been quickly jumping to avoid topics linked to anything with EM investing.

Discussing EM equity returns in the past decade is a conversation-stopper

Equity returns and currencies performance of EM between 2013 to Q1 2024

Note: The equity market return of each country is represented by its respective MSCI country index, rounded.

Source: Bloomberg

EM equity returns over the past decade have indeed been dismal, particularly in USD terms. Of the 23 emerging markets tracked by MSCI, fifteen recorded positive returns in local currency terms. However, only six recorded positive returns when local currency depreciation is taken into account.

Focusing on our Southeast Asia market, none have been positive in USD terms. It’s no wonder it feels like a rollercoaster that has never left the ground.

Take Indonesia, for instance: Indonesian equities, as represented by MSCI Indonesia, achieved a cumulative return of 50 percent over the past decade. However, when we consider the 39 percent depreciation of the Rupiah during this period, the return plunged to a negative 9 percent.

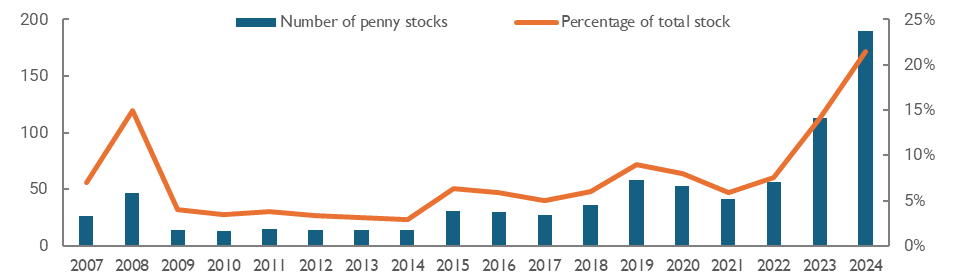

Another perspective, as illustrated in the table below, is that no less than 22 percent of Indonesian stocks are currently trading at or below IDR 50, which used to be the floor price until recent changes. This represents a record high, more than three times the figures seen during the COVID era. To make matters worse, trading volume has significantly decreased. Public expectations for future returns from equity investing are very low or nonexistent.

Penny stocks make up a fifth of Indonesian stocks

# of stocks traded at Rp 50 per share, the lowest possible price in JCI

Source: Bloomberg

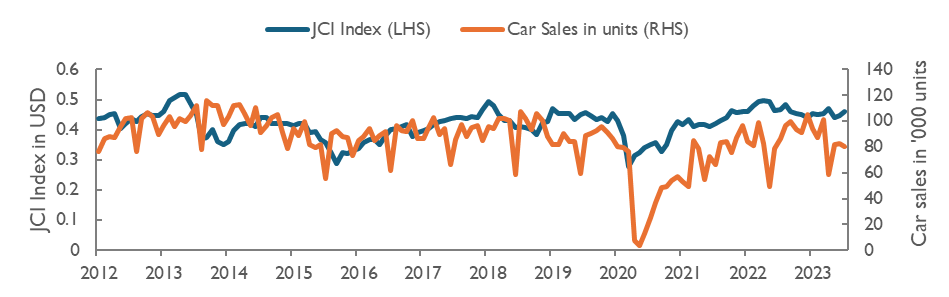

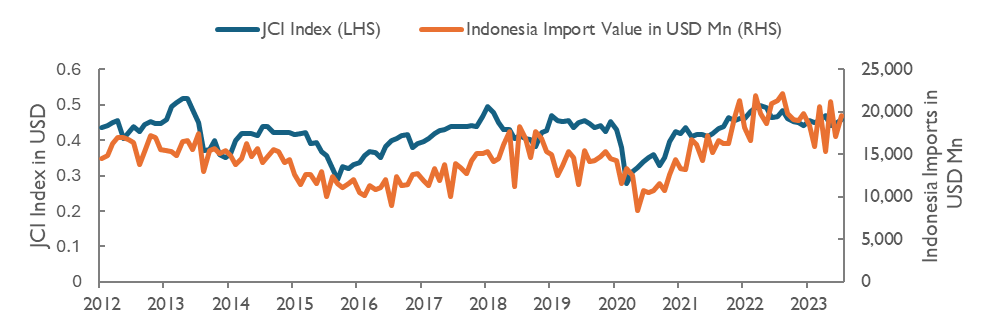

Moving on to the real sectors, the situation is not any better. Key economic indicators of middle-class prosperity, such as auto sales, have been going nowhere for the past 14 years since 2010, despite a 39.4% GDP per capita growth. Are things really that bad? Yes, they are.

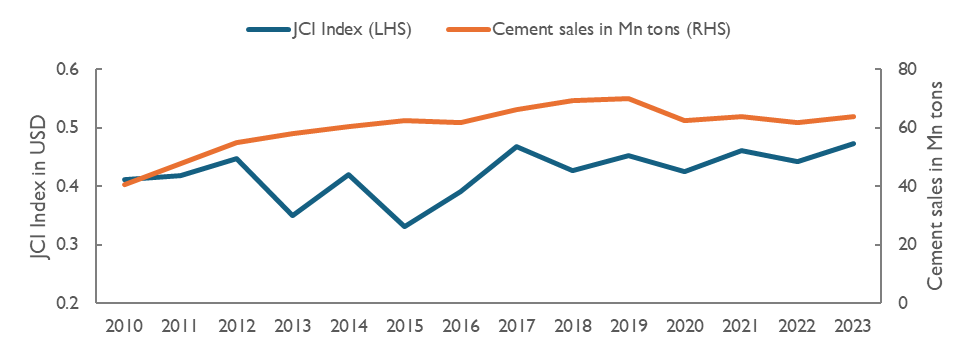

Jakarta Composite Index (“JCI”) in USD echoes coincidence indicators

Indonesia 4W car sales, imports, and cement sales are flat

Source: Bloomberg, Gaikindo (Ministry of Industry)

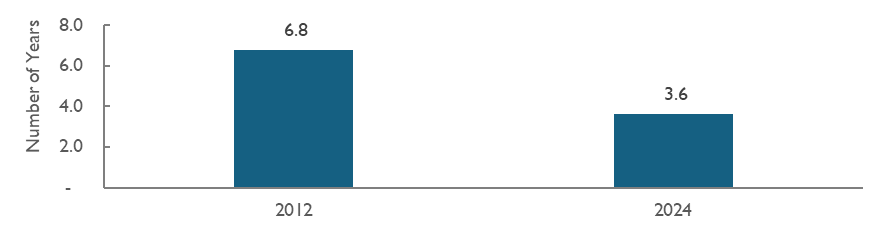

Oddly enough, the number of years it takes to afford the go to car on minimum wage has decreased. What is missing here?

Note: Annualized average minimum wage in Indonesia divided by Toyota Avanza1.3 E M/T car price of the respective year

Source: Auto2000, Kemnaker (Ministry of Manpower).

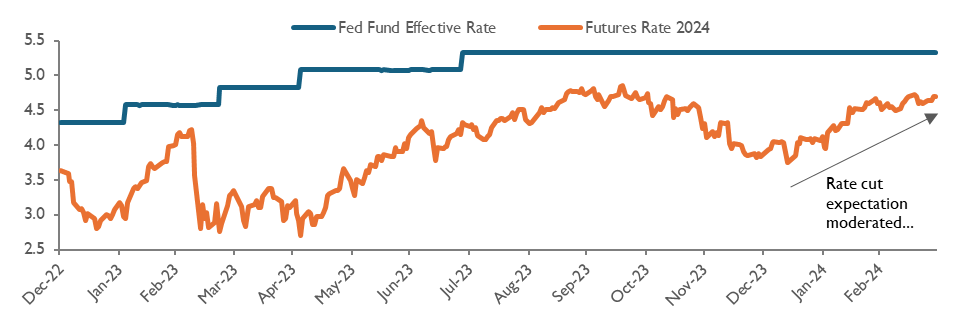

Stockbrokers, struggling with the decreasing revenue pool, have hoped on prophecies of rate cuts. The only difference in their forecasts was which month the rate cuts were going to be delivered. We know what happened next. Until today, the coaster is still stuck on the ground and the greenback has been mighty. This has been weighing down on the EM equities.

Rate cut expectation fades?

The Fed futures rate (%) and effective fund rate

Source: Bloomberg

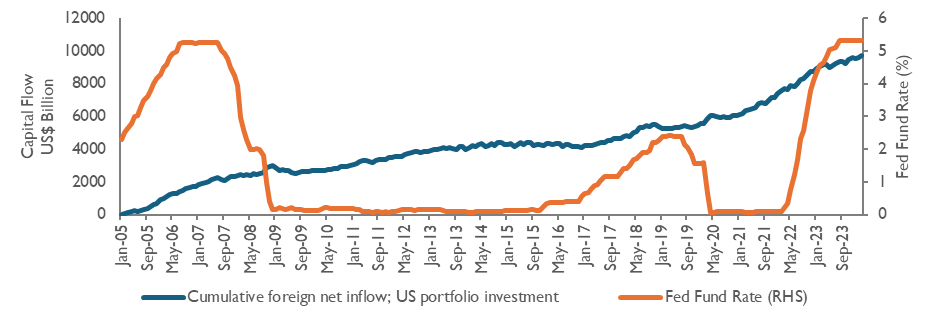

High interest rates draws back capital back to the US

Cumulative foreign net inflow of US portfolio (US$ Bn, since 2005) vs. Fed Fund Rate

Source: Bloomberg

In order for EMs to start performing, the prayer list includes: (1) tamed inflation, (2) recession, and (3) rate cuts as a result of the previous two. Some of these prayers are materializing, but not yet fully granted.

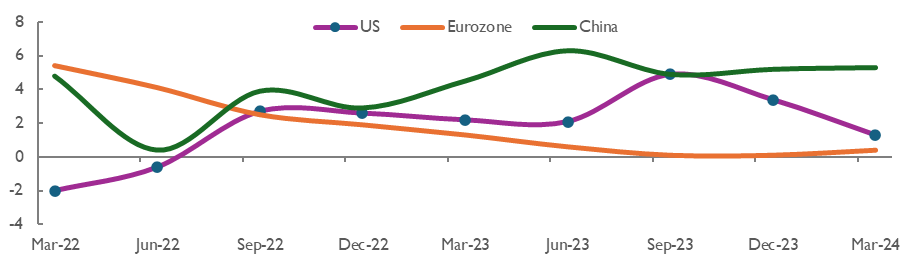

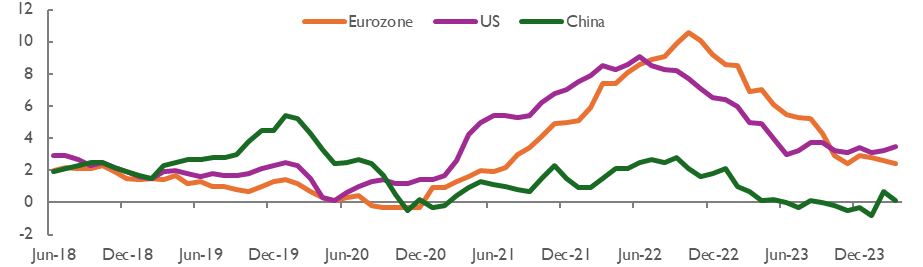

Moderating inflation and weak US economics are precursors for rate cuts

Real GDP growth (YoY) stagnated in Europe, slowed in the US, and was modest in China

CPI inflation (%, YoY) moderating into a new higher-normal

Source: Bloomberg

With all the negativity, it’s easy to fall into the gloom and doom camp about everything. However, much like a dense forest where sunlight occasionally breaks through the canopy, pockets of strength can still be found outside the US market. These bright spots offer hope and opportunity, reminding us that even amidst widespread challenges, there are areas where growth and resilience continue to thrive.

Now imagine a flat bowl balanced on a bamboo tower, filled with water. If everything were static, the water would overflow equally everywhere. But the market isn’t static; it’s a wild circus with elephants (market players) pushing the bowl, spilling water mostly where they prefer, leaving other places dry.

Some get the flow, Some do not

Similarly in emerging markets, some regions are left parched, while others are flourishing with liquidity. Take Argentina, for example. Thanks to radical changes like a smaller government and dollarization, its stock market is bubbling up nicely.

Sure, some might say Argentina’s market is just a tiny puddle in the vast ocean of global capital, with only a USD 53 billion market size. But this goes to show that even in a topsy-turvy market, there are still pockets of opportunity.

So, is it just a periphery market phenomenon in the EM space? We think not. Enter India.

Modi’s administration introduced game-changing economic reforms that transformed India into one of the world’s leading economies. In this case, the game changers are: (1) pro-investment policies and (2) savvy and effective approach to attract Western investments averting from China.

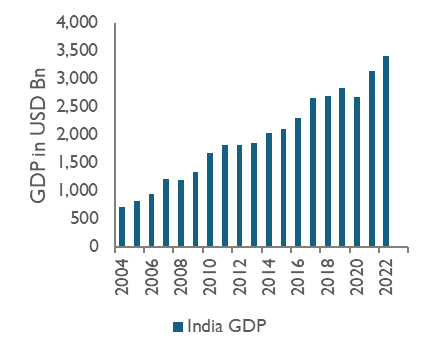

Indonesia’s trade surplus with India – potential commodity supercycle is on the horizon

India GDP (left), in bn USD. Indonesia – India trade balance (right). In USD bn

Source: Bloomberg, Government of Indonesia

Currently, India’s per capita income stands at a modest USD 2,400. However, using the rule of 72, we can make an optimistic projection. Assuming a 6% GDP per capita growth year over year, Indians will be twice as rich in just 12 years.

When incomes rise, consumption patterns change. The first things people tend to buy with their newfound wealth are goods. And when we talk about goods, we’re talking about commodities—lots of them. Increased demand for commodities translates into a thriving market for producers and exporters. Enter Indonesia, which happens to be rich in natural resources and commodities.

Indonesia stands to gain significantly from this economic evolution in India. With its vast reserves of minerals, agricultural products, and energy resources, Indonesia is perfectly positioned to supply the growing Indian appetite for commodities. As India’s middle class expands and consumption increases, Indonesian exports to India are likely to surge, benefiting both economies.

So, while India’s per capita income growth signals a brighter future for its citizens, it also opens up lucrative opportunities for Indonesia. This symbiotic relationship highlights the interconnected nature of global economies, where the prosperity of one nation can ripple out to benefit others.

Still on the subject of Indonesia, recent negative headlines have highlighted the potential for public debt to GDP to reach 50% from the current 39%. Simple arithmetic suggests that this reported figure does not add up.

Leveraging up to 50% would entail significant ramifications, including: (1) interest expenses to revenue reaching 30%, worse than Bangladesh, (2) implying a fiscal deficit of over 5%, well above the 3% limit stipulated by current law, (3) changing this law being improbable given the current parliamentary composition, (4) a significant sovereign downgrade, problematic given that the capital and current account remain negative, and (5) the crowding-out effect, where higher interest rates and an influx of government bonds discourage private sector investments.

All of the above does not seem to be a sensible move for the new Indonesian government.

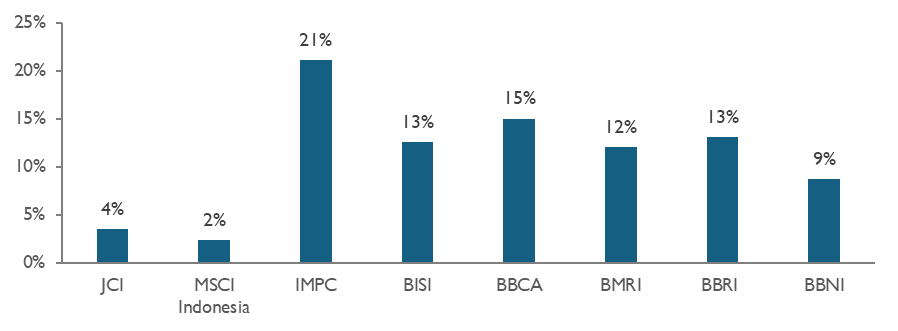

Case in point: finding Pocket of performance in Indonesia

Most investors are already familiar with the success stories of Indonesia’s big four banks. However, despite the prevalent bearish sentiment in the small to mid-cap space in Indonesia, there are noteworthy fast-growing companies in this category. These companies often fly under the radar of many investors, yet they offer significant growth potential. Bisi International (BISI IJ) and Impack Pratama (IMPC IJ) are prime examples of such hidden gems. BISI IJ is a major player in agricultural solutions, providing a wide range of products and services to enhance agricultural productivity. IMPC IJ specializes in alternative building materials, offering innovative and sustainable solutions for construction projects.

What sets these companies apart is their exceptional execution in relatively niche markets that are typically unappealing to larger conglomerates. BISI IJ excels in its specialized agricultural market, leveraging its expertise to drive growth and innovation. Similarly, IMPC IJ focuses on alternative building materials, a sector often overlooked by bigger players. This focus allows both companies to carve out strong market positions and achieve impressive growth rates. Their success stories underscore the potential that exists in Indonesia’s small to mid-cap space, offering investors attractive opportunities beyond the well-known large-cap stocks.

There are gems in muddy water

CAGR (%) on TTM EPS in USD (2014-2024)

CAGR (%) on Total Net Return with Dividends in USD (2014-2024)

Source: Bloomberg

Another topic we have seen people turn away from in a cocktail party until very recently is precious metals. Gold and its poor cousin silver may seem like the dinosaurs of the investment world—static, unexciting, and about as useful as a paperweight in the digital age. It doesn’t generate dividends, won’t give you the thrill of tech stocks, and can sit there for ages without making a splash.

Here’s the kicker: investors should still keep an eye on it. Despite its old-school charm, precious metals have a knack for shining when things get rough. It’s the financial world’s version of a trusty old sweater, offering warmth and comfort when the economic weather turns chilly. So, while it might not be the flashiest asset in your portfolio, it’s definitely one asset class worth allocating into.

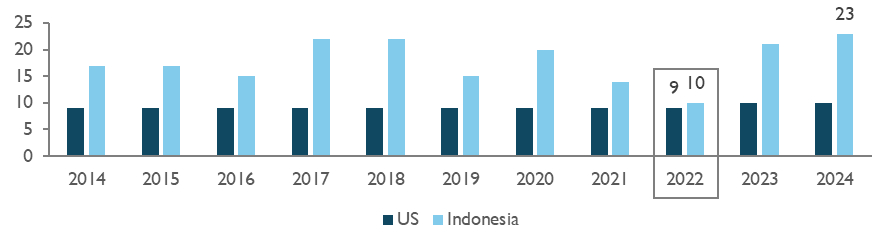

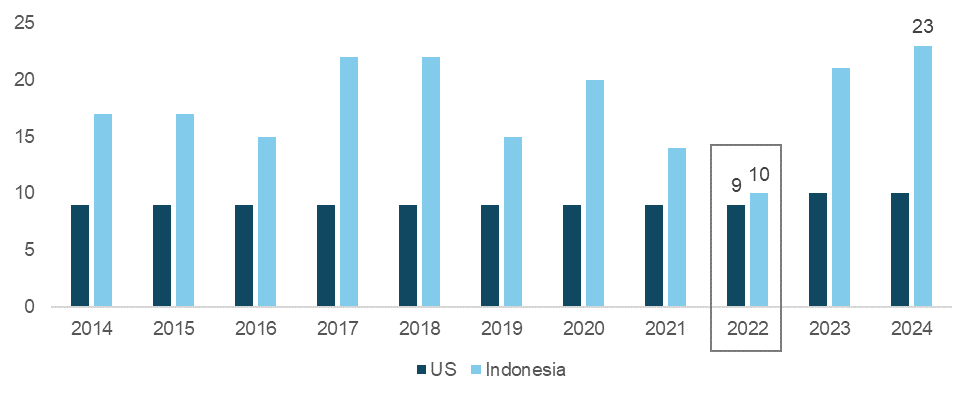

Indonesia is breaking records, but it’s not for the hottest chili or longest dance marathon—it’s for

holidays, racking up a whopping 23 days off this year. Meanwhile, the US sticks to a lean average of 9

days. For investors, it’s been a rough ride in emerging markets, with US stocks often leaving Indonesian

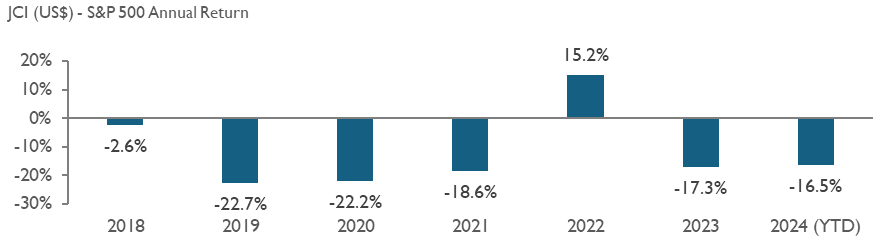

ones eating dust. Interestingly in 2022, Indonesia’s Jakarta Composite Index (JCI) outshined the

S&P 500 with a dazzling 15% gain. Coincidentally, Indonesia only took 10 holidays that year, almost

mirroring the US. Could fewer holidays be the secret sauce for market success? Something to chew on

as we plan our next beach getaway!

Indonesia’s JCI outperformed S&P500 when its holidays were the lowest

Number of stock market holidays of the US vs Indonesia (in days)

Source: Bloomberg

Share

“Investing in EMs in the past decade is like preparing for a firework show that ends with a single sparkler—underwhelming and disappointing.”

We’re all familiar with the conversations above, albeit in different forms. Just mention “EM (Emerging Market) equity” at a cocktail party, and you’ll see people quickly finishing their drinks and changing the subject to US market investing. Could this be a classic example of Peter Lynch’s cocktail party theory, indicating that the market is bottoming out?

Beyond the liquor

In “One Up on Wall Street,” Peter Lynch identified cocktail party conversations as a significant contrarian market indicator. When people avoid discussing certain investments, it’s often a sign that the market is bottoming, presenting an opportunity to find undervalued stocks. Conversely, when such gatherings are filled with investment tips and general euphoria, it typically signals that the market is peaking and a downturn may be imminent.

The following table below showcases why people have been quickly jumping to avoid topics linked to anything with EM investing.

Discussing EM equity returns in the past decade is a conversation-stopper

Equity returns and currencies performance of EM between 2013 to Q1 2024

Note: The equity market return of each country is represented by its respective MSCI country index, rounded.

Source: Bloomberg

EM equity returns over the past decade have indeed been dismal, particularly in USD terms. Of the 23 emerging markets tracked by MSCI, fifteen recorded positive returns in local currency terms. However, only six recorded positive returns when local currency depreciation is taken into account.

Focusing on our Southeast Asia market, none have been positive in USD terms. It’s no wonder it feels like a rollercoaster that has never left the ground.

Take Indonesia, for instance: Indonesian equities, as represented by MSCI Indonesia, achieved a cumulative return of 50 percent over the past decade. However, when we consider the 39 percent depreciation of the Rupiah during this period, the return plunged to a negative 9 percent.

Another perspective, as illustrated in the table below, is that no less than 22 percent of Indonesian stocks are currently trading at or below IDR 50, which used to be the floor price until recent changes. This represents a record high, more than three times the figures seen during the COVID era. To make matters worse, trading volume has significantly decreased. Public expectations for future returns from equity investing are very low or nonexistent.

Penny stocks make up a fifth of Indonesian stocks

# of stocks traded at Rp 50 per share, the lowest possible price in JCI

Source: Bloomberg

Moving on to the real sectors, the situation is not any better. Key economic indicators of middle-class prosperity, such as auto sales, have been going nowhere for the past 14 years since 2010, despite a 39.4% GDP per capita growth. Are things really that bad? Yes, they are.

Jakarta Composite Index (“JCI”) in USD echoes coincidence indicators

Indonesia 4W car sales, imports, and cement sales are flat

Source: Bloomberg, Gaikindo (Ministry of Industry)

Oddly enough, the number of years it takes to afford the go to car on minimum wage has decreased. What is missing here?

Note: Annualized average minimum wage in Indonesia divided by Toyota Avanza1.3 E M/T car price of the respective year

Source: Auto2000, Kemnaker (Ministry of Manpower).

Stockbrokers, struggling with the decreasing revenue pool, have hoped on prophecies of rate cuts. The only difference in their forecasts was which month the rate cuts were going to be delivered. We know what happened next. Until today, the coaster is still stuck on the ground and the greenback has been mighty. This has been weighing down on the EM equities.

Rate cut expectation fades?

The Fed futures rate (%) and effective fund rate

Source: Bloomberg

High interest rates draws back capital back to the US

Cumulative foreign net inflow of US portfolio (US$ Bn, since 2005) vs. Fed Fund Rate

Source: Bloomberg

In order for EMs to start performing, the prayer list includes: (1) tamed inflation, (2) recession, and (3) rate cuts as a result of the previous two. Some of these prayers are materializing, but not yet fully granted.

Moderating inflation and weak US economics are precursors for rate cuts

Real GDP growth (YoY) stagnated in Europe, slowed in the US, and was modest in China

CPI inflation (%, YoY) moderating into a new higher-normal

Source: Bloomberg

With all the negativity, it’s easy to fall into the gloom and doom camp about everything. However, much like a dense forest where sunlight occasionally breaks through the canopy, pockets of strength can still be found outside the US market. These bright spots offer hope and opportunity, reminding us that even amidst widespread challenges, there are areas where growth and resilience continue to thrive.

Now imagine a flat bowl balanced on a bamboo tower, filled with water. If everything were static, the water would overflow equally everywhere. But the market isn’t static; it’s a wild circus with elephants (market players) pushing the bowl, spilling water mostly where they prefer, leaving other places dry.

Some get the flow, Some do not

Similarly in emerging markets, some regions are left parched, while others are flourishing with liquidity. Take Argentina, for example. Thanks to radical changes like a smaller government and dollarization, its stock market is bubbling up nicely.

Sure, some might say Argentina’s market is just a tiny puddle in the vast ocean of global capital, with only a USD 53 billion market size. But this goes to show that even in a topsy-turvy market, there are still pockets of opportunity.

So, is it just a periphery market phenomenon in the EM space? We think not. Enter India.

Modi’s administration introduced game-changing economic reforms that transformed India into one of the world’s leading economies. In this case, the game changers are: (1) pro-investment policies and (2) savvy and effective approach to attract Western investments averting from China.

Indonesia’s trade surplus with India – potential commodity supercycle is on the horizon

India GDP (left), in bn USD. Indonesia – India trade balance (right). In USD bn

Source: Bloomberg, Government of Indonesia

Currently, India’s per capita income stands at a modest USD 2,400. However, using the rule of 72, we can make an optimistic projection. Assuming a 6% GDP per capita growth year over year, Indians will be twice as rich in just 12 years.

When incomes rise, consumption patterns change. The first things people tend to buy with their newfound wealth are goods. And when we talk about goods, we’re talking about commodities—lots of them. Increased demand for commodities translates into a thriving market for producers and exporters. Enter Indonesia, which happens to be rich in natural resources and commodities.

Indonesia stands to gain significantly from this economic evolution in India. With its vast reserves of minerals, agricultural products, and energy resources, Indonesia is perfectly positioned to supply the growing Indian appetite for commodities. As India’s middle class expands and consumption increases, Indonesian exports to India are likely to surge, benefiting both economies.

So, while India’s per capita income growth signals a brighter future for its citizens, it also opens up lucrative opportunities for Indonesia. This symbiotic relationship highlights the interconnected nature of global economies, where the prosperity of one nation can ripple out to benefit others.

Still on the subject of Indonesia, recent negative headlines have highlighted the potential for public debt to GDP to reach 50% from the current 39%. Simple arithmetic suggests that this reported figure does not add up.

Leveraging up to 50% would entail significant ramifications, including: (1) interest expenses to revenue reaching 30%, worse than Bangladesh, (2) implying a fiscal deficit of over 5%, well above the 3% limit stipulated by current law, (3) changing this law being improbable given the current parliamentary composition, (4) a significant sovereign downgrade, problematic given that the capital and current account remain negative, and (5) the crowding-out effect, where higher interest rates and an influx of government bonds discourage private sector investments.

All of the above does not seem to be a sensible move for the new Indonesian government.

Case in point: finding Pocket of performance in Indonesia

Most investors are already familiar with the success stories of Indonesia’s big four banks. However, despite the prevalent bearish sentiment in the small to mid-cap space in Indonesia, there are noteworthy fast-growing companies in this category. These companies often fly under the radar of many investors, yet they offer significant growth potential. Bisi International (BISI IJ) and Impack Pratama (IMPC IJ) are prime examples of such hidden gems. BISI IJ is a major player in agricultural solutions, providing a wide range of products and services to enhance agricultural productivity. IMPC IJ specializes in alternative building materials, offering innovative and sustainable solutions for construction projects.

What sets these companies apart is their exceptional execution in relatively niche markets that are typically unappealing to larger conglomerates. BISI IJ excels in its specialized agricultural market, leveraging its expertise to drive growth and innovation. Similarly, IMPC IJ focuses on alternative building materials, a sector often overlooked by bigger players. This focus allows both companies to carve out strong market positions and achieve impressive growth rates. Their success stories underscore the potential that exists in Indonesia’s small to mid-cap space, offering investors attractive opportunities beyond the well-known large-cap stocks.

There are gems in muddy water

CAGR (%) on TTM EPS in USD (2014-2024)

CAGR (%) on Total Net Return with Dividends in USD (2014-2024)

Source: Bloomberg

Another topic we have seen people turn away from in a cocktail party until very recently is precious metals. Gold and its poor cousin silver may seem like the dinosaurs of the investment world—static, unexciting, and about as useful as a paperweight in the digital age. It doesn’t generate dividends, won’t give you the thrill of tech stocks, and can sit there for ages without making a splash.

Here’s the kicker: investors should still keep an eye on it. Despite its old-school charm, precious metals have a knack for shining when things get rough. It’s the financial world’s version of a trusty old sweater, offering warmth and comfort when the economic weather turns chilly. So, while it might not be the flashiest asset in your portfolio, it’s definitely one asset class worth allocating into.

Indonesia is breaking records, but it’s not for the hottest chili or longest dance marathon—it’s for

holidays, racking up a whopping 23 days off this year. Meanwhile, the US sticks to a lean average of 9

days. For investors, it’s been a rough ride in emerging markets, with US stocks often leaving Indonesian

ones eating dust. Interestingly in 2022, Indonesia’s Jakarta Composite Index (JCI) outshined the

S&P 500 with a dazzling 15% gain. Coincidentally, Indonesia only took 10 holidays that year, almost

mirroring the US. Could fewer holidays be the secret sauce for market success? Something to chew on

as we plan our next beach getaway!

Indonesia’s JCI outperformed S&P500 when its holidays were the lowest

Number of stock market holidays of the US vs Indonesia (in days)

Source: Bloomberg

Share

Indonesia is breaking records, but not in the way you might think. It’s not about the hottest chili or the longest dance marathon—no, Indonesia has increased its number of holidays to the most it’s ever had in a year, clocking in at a whopping 23 days.

Now let’s toss that number next to the US stock market’s holiday calendar and the difference between are quite stark. The US has maintained its days off at an average of 9 days whereas Indonesia averages at 17.

Indonesia has more holidays than the US

Number of stock market holidays of the US vs Indonesia (in days)

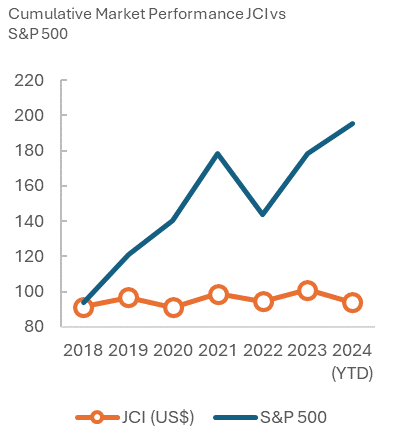

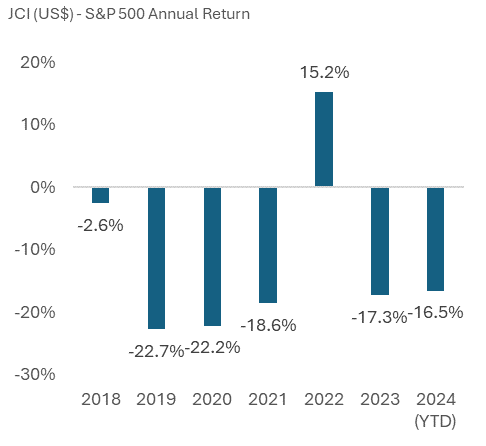

The last half decade has been a tough time for investors in emerging markets, with the US equities returns often leaving Indonesia’s in its trail. But there was a glimmer of light in the dark tunnel: In 2022, Indonesia’s Jakarta Composite Index (JCI) outperformed the S&P 500 index with an impressive gain of over 15%.

Indonesia’s JCI outperformed S&P500 when its holidays were the lowest

Source: Bloomberg

Coincidentally, 2022 was also the year where Indonesia had its lowest number of holidays, almost matching the US’s calendar with 10 and 9 days off respectively.

Perhaps holidays might not be the main driver for market’s outperformance and underperformance, but it does make you ponder: might the market’s ups and downs be tied to how many days traders get to kick back and relax?

Could decreasing the number of holidays be the low hanging fruit ready to be reaped to improve market performance?

Let’s ponder that as we plan our next holiday!

Tara Mulia

Share

Indonesia is breaking records, but not in the way you might think. It’s not about the hottest chili or the longest dance marathon—no, Indonesia has increased its number of holidays to the most it’s ever had in a year, clocking in at a whopping 23 days.

Now let’s toss that number next to the US stock market’s holiday calendar and the difference between are quite stark. The US has maintained its days off at an average of 9 days whereas Indonesia averages at 17.

Indonesia has more holidays than the US

Number of stock market holidays of the US vs Indonesia (in days)

The last half decade has been a tough time for investors in emerging markets, with the US equities returns often leaving Indonesia’s in its trail. But there was a glimmer of light in the dark tunnel: In 2022, Indonesia’s Jakarta Composite Index (JCI) outperformed the S&P 500 index with an impressive gain of over 15%.

Indonesia’s JCI outperformed S&P500 when its holidays were the lowest

Source: Bloomberg

Coincidentally, 2022 was also the year where Indonesia had its lowest number of holidays, almost matching the US’s calendar with 10 and 9 days off respectively.

Perhaps holidays might not be the main driver for market’s outperformance and underperformance, but it does make you ponder: might the market’s ups and downs be tied to how many days traders get to kick back and relax?

Could decreasing the number of holidays be the low hanging fruit ready to be reaped to improve market performance?

Let’s ponder that as we plan our next holiday!

Tara Mulia

Share

In the span of a decade, the world has undergone transformative changes, some visible in the palm of our hand. The touchscreen technology that allows this blog to be accessed was not nearly as pervasive in 2014. Back then, many of us clung to our BlackBerrys—a brand that has since exited the smartphone market. Reflect on the 2014 FIFA World Cup, where Germany’s stunning 7-1 victory over host Brazil left fans around the globe in disbelief. These moments from ten years ago set the stage for another significant beginning: the presidency of Joko Widodo.

A lot can happen in ten years—technologies evolve, champions are crowned, and nations can be reshaped. Among these, the downstreaming project stands out as a monumental legacy, propelling substantial economic and industrial shifts across Indonesia. Today I look back at my trip to Morowali, a hub of the nickel down streaming project.

What I’ve witnessed firsthand compels belief, yet it surpasses imagination. Join me as we delve into the incredible progress of Indonesia within these 10 years, to help us imagine what the decades to come may hold.

Morowali, March 2024.

Jakarta – Morowali sky: a flight buddy

“Waiting for your turn to board the plane, Morowali style”

Despite rapid development in the past few years, Morowali is still not for the faint-hearted. Plane for example was pretty basic, a propeller plane. In particular, the air conditioning was not properly working, except for a brief few minutes during this 45-minute flight. Nonetheless, the opportunity for an interesting conversation with fellow passengers was more than enough to compensate for the lack of comfort during the flight.

Nandar

ZTE employee, travels to Morowali three times a year, witnessed the rapid economic development since the beginning

I met Nandar, who is originally from the city of Makassar, 400km from Morowali, connected by that 45-minute three times-a-day flight. He works for a Chinese telco network company ZTE and travels to Morowali three times a year. I learned from him that the mobile company Telkomsel (TLKM IJ) generates the biggest revenues in Sulawesi from their Morowali operation. Business-wise, Morowali is already bigger than the largest city in Sulawesi, Makassar. In Morowali, Telkomsel’s biggest competitor is XL Axiata (EXCL IJ).

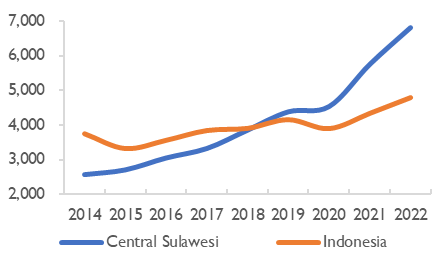

Burgeoning wealth

Nandar shares his enthusiasm for the progress in Morowali. He said that a decade ago, everyone was poor. Even the head of the village. Nowadays, it is quite a norm for the head of the village to own and drive a Toyota Fortuner (costs c. US$ 35k, equal to 7.4x of Indonesia’s GDP per capita).

Wealth creation breeds a lot of wheelers

Number of cars in Central Sulawesi (thousands)

No. of motorcycles in Central Sulawesi (k units)

Central Sulawesi province GDP per Capita vs. Indonesia’s (US$)

Source: Government data

He said that boarding is not cheap, as the competition for a boarding room is intense. The population in Morowali has gone up from 167k last year to 176k in 2022, a 5% increase compared to 3% increase the year before. A simple room with a plywood wall will set him back by Rp700k (USD 50) per month. A more decent room with a concrete wall costs twice as much. This price matches Jakarta’s price despite the per capita income in Jakarta is quadruple Morowali’s level.

In terms of income, Nandar told us the monthly salary of Morowali workers was at least IDR 6 to 8 mn (US$ 387 to 516) with a median is somewhere between IDR 10 to 15 mn (US$ 645 to 967). This is much higher compared to Jakarta and Makassar’s minimum wage of IDR 4.9 mn (US$ 316) and IDR 3.6 mn (US$ 232) respectively.

But, with high income comes great demand for productivity:

Table: Typical working scheme at IMIP

| Category | Working scheme |

| Locals | Rp 13 mn (US$ 838) monthly salary 5 working days, 2 days leave\ Rp 15 – 18 mn (US$ 967 to 1,161) monthly salary 8 working days, 2 days leave |

| Chinese expats | Salary Unknown 6 months working days (straight), 12 days leave |

Nandar told me how the population of Morowali has grown by leaps and bounds.

The aircon was suddenly turned on and Nandar told me that it meant the plane was about to land. Cool air was flowing like the sounds of smooth jazz from a Basin Street bar. Suddenly I did not take the aircon for granted anymore and started to think that aircon was one of the best inventions of the human race. Nandar took it as a cue to end our conversation and got ready for landing. He planned to stay for a week in Morowali.

I used the opportunity before landing to ask him if he had any complaints about Morowali. He said everything was great. He wants his kids to do well in life, going to university and learning Chinese. Oh, actually one complaint, he added.

The food is great in the accommodation provided (the Wisma) in Morowali. Unfortunately, he could not really use chopsticks to eat. As a result, he typically loses quite a bit of weight during a business trip to Morowali. Other than that, for him, Morowali offers a great deal of opportunities. Nandar’s transport and meal allowance in Morowali is Rp100k (US$6.45)/day, twice his usual rate. That certainly incentivises him to love Morowali even more.

“Morowali Airport: somewhat chaotic but works”.

“The simple 10 years to build Morowali Airport”

The scorching heat of the Morowali plain was in complete contrast to the gorgeous sight in front of us. The new Morowali airport (budget was allocated in 2007, but only completed a decade later in 2017, not everything in Morowali is magical) failed to provide much sanctuary from the heat, as most air conditioners in the airport seemed to be already exhausted. Passengers’ bags were stuck in the airport, somewhat chaotic but overall, the airport miraculously worked.

The road to Morowali, the boom town

Next step was a four-hour car trip from Morowali airport to IMIP (Indonesia Morowali Industrial Park), an industrial park with a total area of 4,000 ha and 100,000 workers. To put it into context, the total number of employees was 75,000 when we visited the park in August 2022. The park boasts 54 NPI RKEFs line (8 of which are under construction) with 5 mtpa capacity. These RKEF facilities represent over 55% of such capacities in Indonesia! Not to mention new energy battery materials, 2 HPAL plants; one under construction.

Embarking on this 4-hour journey has unfolded a tapestry of gorgeous views, each moment was brushstroke painting memory of shared conversations. Entering Morowali boom town, the dusty roads echoed tales of frenetic energy, lined with hastily erected structures. The community is vibrant, with a heartbeat of its own. Shops open 24- hours, catering to the newfound prosperity. Not even in Jakarta we see such a crucible of ambition and industry.

“Petrol distribution, BRI Agent, and Smartphone shops open 24/7 hours mean serious business”

We also witnessed many small shops selling gasoline. In fact, it was like every 20 meters we would come across shops selling gasoline. The presence of numerous small shops selling gasoline may indicate a scarcity or distribution challenge in the supply chain. It could be a response to logistical disruption. The official system was somewhat broken.

A resting place for the weary

Before we knew it, we arrived at the famous Wisma IMIP, a five-star facility to host high-level management and IMIP investors.

Nestled in the heart of a remote location, our accommodation facility stands as a beacon of comfort amidst rugged terrain. The combination of comfortable rooms and hearty meals in the spacious dining halls caters to both relaxation and the unique needs of those working in the challenging environment. Thanks to the serene retreat, I was forgetting that I was in Morowali.

The luxury crafted in this guest house seems to reflect their sign of commitment.

Wisma IMIP’s Lobby – a “humble” welcoming

Backyard view: facing the port

Spacious and well-designed meeting room

Dining hall and delicate meals

Comfortable room. Everything inside is “Made in China”, except TOTO sanitary – sign of moat?

Visiting the powerhouse

We also had the opportunity to visit SCM nickel mining site, 40 km away from IMIP. This mining asset is 51% owned by Merdeka Battery (MBMA IJ). The remaining stake is held by Tsingshan.

“Inside Morowali Industirial Park – a testament to the power of perseverance and hard work”

What’s really striking is the high-quality 40-km hauling road connecting industrial estate IMIP and mining site SCM. This road is clearly the crucial lifeline for efficient operations, unlocking value for the mining assets. Constructed with durability in mind, this road is designed to withstand the heavy road for a very long time. Its robust design incorporates advanced engineering techniques to ensure resilience against the challenging conditions of the mining environment. This road facilitates the smooth movement of heavy machinery and oreladen trucks.

“SCM Hauling Road – an engineering marvel

”The lush forest and the pristine environment is gentle reminder to practice sustainability”

Remarks from the trip

Reflecting on our journey to Morowali’s nickel processing hub, we witness a transformation fueled by perseverance and dedication. The pioneers of this industry, including the vibrant community and dedicated workers of IMIP, exemplify how dedication does not betray the effort invested. The development of infrastructure, like the hauling road and Wisma IMIP, alongside Nandar’s story, highlight growth and resilience. This story epitomizes the transformation of a remote area into an industrial hub. Morowali’s evolution signifies national progress and global market influence. It emphasizes the impact of visionary leadership and industry on growth and prosperity. Hard work betrays none, but dreams betray many…

Share

In the span of a decade, the world has undergone transformative changes, some visible in the palm of our hand. The touchscreen technology that allows this blog to be accessed was not nearly as pervasive in 2014. Back then, many of us clung to our BlackBerrys—a brand that has since exited the smartphone market. Reflect on the 2014 FIFA World Cup, where Germany’s stunning 7-1 victory over host Brazil left fans around the globe in disbelief. These moments from ten years ago set the stage for another significant beginning: the presidency of Joko Widodo.

A lot can happen in ten years—technologies evolve, champions are crowned, and nations can be reshaped. Among these, the downstreaming project stands out as a monumental legacy, propelling substantial economic and industrial shifts across Indonesia. Today I look back at my trip to Morowali, a hub of the nickel down streaming project.

What I’ve witnessed firsthand compels belief, yet it surpasses imagination. Join me as we delve into the incredible progress of Indonesia within these 10 years, to help us imagine what the decades to come may hold.

Morowali, March 2024.

Jakarta – Morowali sky: a flight buddy

“Waiting for your turn to board the plane, Morowali style”

Despite rapid development in the past few years, Morowali is still not for the faint-hearted. Plane for example was pretty basic, a propeller plane. In particular, the air conditioning was not properly working, except for a brief few minutes during this 45-minute flight. Nonetheless, the opportunity for an interesting conversation with fellow passengers was more than enough to compensate for the lack of comfort during the flight.

Nandar

ZTE employee, travels to Morowali three times a year, witnessed the rapid economic development since the beginning

I met Nandar, who is originally from the city of Makassar, 400km from Morowali, connected by that 45-minute three times-a-day flight. He works for a Chinese telco network company ZTE and travels to Morowali three times a year. I learned from him that the mobile company Telkomsel (TLKM IJ) generates the biggest revenues in Sulawesi from their Morowali operation. Business-wise, Morowali is already bigger than the largest city in Sulawesi, Makassar. In Morowali, Telkomsel’s biggest competitor is XL Axiata (EXCL IJ).

Burgeoning wealth

Nandar shares his enthusiasm for the progress in Morowali. He said that a decade ago, everyone was poor. Even the head of the village. Nowadays, it is quite a norm for the head of the village to own and drive a Toyota Fortuner (costs c. US$ 35k, equal to 7.4x of Indonesia’s GDP per capita).

Wealth creation breeds a lot of wheelers

Number of cars in Central Sulawesi (thousands)

No. of motorcycles in Central Sulawesi (k units)

Central Sulawesi province GDP per Capita vs. Indonesia’s (US$)

Source: Government data

He said that boarding is not cheap, as the competition for a boarding room is intense. The population in Morowali has gone up from 167k last year to 176k in 2022, a 5% increase compared to 3% increase the year before. A simple room with a plywood wall will set him back by Rp700k (USD 50) per month. A more decent room with a concrete wall costs twice as much. This price matches Jakarta’s price despite the per capita income in Jakarta is quadruple Morowali’s level.

In terms of income, Nandar told us the monthly salary of Morowali workers was at least IDR 6 to 8 mn (US$ 387 to 516) with a median is somewhere between IDR 10 to 15 mn (US$ 645 to 967). This is much higher compared to Jakarta and Makassar’s minimum wage of IDR 4.9 mn (US$ 316) and IDR 3.6 mn (US$ 232) respectively.

But, with high income comes great demand for productivity:

Table: Typical working scheme at IMIP

| Category | Working scheme |

| Locals | Rp 13 mn (US$ 838) monthly salary 5 working days, 2 days leave\ Rp 15 – 18 mn (US$ 967 to 1,161) monthly salary 8 working days, 2 days leave |

| Chinese expats | Salary Unknown 6 months working days (straight), 12 days leave |

Nandar told me how the population of Morowali has grown by leaps and bounds.

The aircon was suddenly turned on and Nandar told me that it meant the plane was about to land. Cool air was flowing like the sounds of smooth jazz from a Basin Street bar. Suddenly I did not take the aircon for granted anymore and started to think that aircon was one of the best inventions of the human race. Nandar took it as a cue to end our conversation and got ready for landing. He planned to stay for a week in Morowali.