Have you ever wondered how the 2% inflation target got to 2%?

Picture a television studio in New Zealand, 1988. Big hair, boxy suits, the works. The country has spent two decades getting mugged by inflation, which tore through the 1970s and early 1980s and refused to fully sit down even after a painful round of reforms.

The finance minister, Roger Douglas, is on air trying to convince a skeptical public that the central bank will not quietly tolerate rising prices forever. Pressed on what he is actually aiming for, he says he’d like to see inflation somewhere around zero to one percent.

There was no model behind the number, no white paper, no committee. It was the central-banking equivalent of being asked your goal weight and answering, “I dunno, abs?”

Don Brash, the kiwifruit farmer turned central banker who had just taken over the Reserve Bank of New Zealand, later put it plainly: “It was almost a chance remark. The figure was plucked out of the air to influence the public’s expectations.”

1988 comic ridiculing the Reserve Bank of New Zealand’s inflation prediction

1988 comic ridiculing the Reserve Bank of New Zealand’s inflation prediction

Source: Malcolm Walker, Reserve Bank of New Zealand

Brash, as it happens, had personal reasons to loathe inflation. He liked to tell the story of an uncle who sold his apple orchard in 1971, parked the proceeds in long-term government bonds to fund his retirement, and then watched inflation incinerate 90 percent of his life savings by the time those bonds matured. Keep that uncle in mind.

The Reserve Bank Act of 1989 turned the chance remark into a job description. It ordered the finance minister and the central bank to agree on a formal inflation target, handed the bank independence to chase it, and made the goal enforceable by allowing the governor to be fired for missing.

Brash and the finance minister of the day, David Caygill, took Douglas’s zero-to-one, widened it a touch for breathing room, and settled on a band of zero to 2 percent. The law passed in a quick, near-unanimous vote by parliamentarians keen to get home for Christmas.

Here is the punchline: it worked. Inflation was 7.6 percent when the law passed in 1989. By the end of 1991 it was 2 percent. Simply by announcing a number and meaning it, New Zealand talked wages and prices into behaving.

Brash evangelized to fellow central bankers at Jackson Hole, and the converts piled in: Canada in 1991, then Sweden, then Britain. Today roughly 45 countries plus the Euro Area run on an inflation target, and 2 percent has become, in the New York Times’s lovely phrase, “virtually an economic religion.”

The religion, live on air. First thing that appeared on our Bloomberg TV

The religion, live on air. First thing that appeared on our Bloomberg TV

We mention all this not to dunk on New Zealand, which also gave us excellent lamb and the cinematic “Lord of the Rings”, but because a figure plucked from the air on a Wellington TV set now governs the value of your savings. When a target is arbitrary, it is also negotiable. And the people most exposed to that negotiation are savers.

New Zealand started it first and others began to follow suit

New Zealand started it first and others began to follow suit

Sources: NYT; World Bank

The Federal Reserve was a late and reluctant convert. Behind the oversized doors of its boardroom in 1995 and 1996, officials argued about whether to copy the Kiwis at all, and if so, what the number should be. Heavyweights like Paul Volcker and Alan Greenspan leaned toward zero, on the logic that a dollar today should buy roughly what a dollar buys in twenty years.

The governor who argued hardest for a positive target of around 2 percent was a woman named Janet Yellen. Her case was the grease-the-wheels argument: a little inflation lets employers quietly trim real wages without the misery of cutting nominal pay, and, crucially, it lets real interest rates go negative when a recession demands it.

“A little inflation permits real interest rates to become negative on the rare occasions when required to counter a recession,” she told the room in 1996. “This could be important.” She had no idea how important.

Yellen won. The Fed privately settled on 2 percent in 1996 and only said so out loud in 2012. And yes, this is the same Janet Yellen from our “Welcome to the Banana Republic,” piece, the one who later ran the Treasury and issued the mountain of debt now straining against that very target.

A Hawk Walks In, and Says Almost Nothing

Which brings us to this week. On June 17, the Federal Reserve held its benchmark rate at 3.5% to 3.75%, the first meeting chaired by Kevin Warsh. No cut. The committee dropped its earlier forecast of a cut this year.

The appointment of a new chairman does matter here as each person leading carries different philosophies which can impact how the Fed will move forward. Kevin Warsh sat on the Fed’s Board of Governors from 2006 to 2011, through the heart of the financial crisis, then spent the years since as one of the institution’s sharpest critics. He argued the Fed had grown too talkative, too wedded to its models, and too comfortable with easy money. That is the tell.

Where Janet Yellen built the machinery of an explicit target, and Jerome Powell leaned into ever more detailed forward guidance, Warsh seems to want the opposite: fewer promises and more discretion. His appointment matters because it hands the keys of the post-2008 transparency project to a man who never quite believed in it.

The median official now pencils in a fed funds rate of 3.8 percent by December, which is to say a hike, with PCE inflation projected at 3.6 percent for the year, nearly double the target. The policy statement was stripped to what Warsh called “a bit shorter, a bit simpler,” and shorn of the “so-called forward guidance” he judged “not well-suited to the current policy conjuncture.”

Source: Fortune

Source: Fortune

But the real news was what Warsh would not say. While he encouraged his colleagues to keep submitting their forecasts to the famous dot plot, he refused to submit his own. “I have refrained from offering any projections of my own,” he announced, “consistent with my long-held views on the SEP.”

No dot, no roadmap, no breadcrumbs. This is a genuine break. For more than a decade the Fed has practically narrated its own intentions in advance; Warsh prefers what he admires about the Greenspan era, the deliberate fog, the man-behind-the-curtain mystique.

And tucked into the same meeting was the part that should make every saver sit up. Among five new task forces Warsh announced was one charged with re-examining the Fed’s “inflation frameworks” from “first principles,” weighing “the full range of ideas for delivering price stability.”

Why would a central bank want to be less clear about its target just as that target turns inconvenient? Maybe it is humility. Or maybe it has nothing to do with inflation, and everything to do with the size of the bill.

To be clear, none of this means the Fed has decided to raise its inflation target; reviewing a framework is not the same as loosening one, and a review could just as easily change nothing. But history is fairly blunt about the pattern: heavily indebted governments tend, sooner or later, to find reasons to tolerate a little more inflation than they once promised.

The Trillion-Dollar Tenant Nobody Voted For

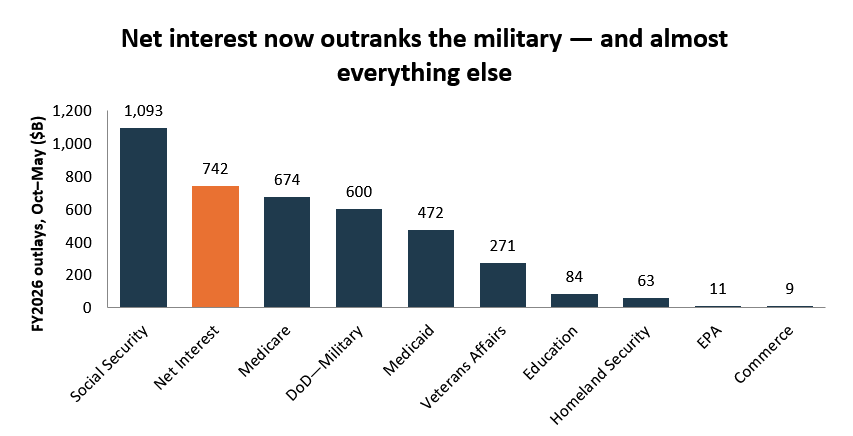

Here is the number that should be keeping policymakers up at night. The US government is on track to spend roughly $1 trillion on interest payments this fiscal year. That is more than the entire defense budget, which runs around $947 billion, and net interest already overtook defense spending in the first quarter.

Put another way: for every dollar Washington collects in taxes, about 19 cents now goes straight to bondholders before a single road is paved or fighter jet is fueled. Interest costs are running near 3.2% of GDP, eclipsing a record set back in 1991.

The chart below covers only the first eight months of this fiscal year, and even on that partial tally net interest ($742 billion) has already overtaken the military ($600 billion); annualized, it crosses $1 trillion.

Source: Congressional Budget Office

Source: Congressional Budget Office

The cruel mechanics are simple: the higher the Fed keeps rates to fight inflation, the more expensive that trillion-dollar tenant becomes. A government this indebted cannot actually afford honestly high interest rates for long. Something has to give, and “raise taxes” and “cut spending” are about as popular as a durian in a crowded elevator. So what’s left?

The option nobody campaigns on: let inflation run a little hot, keep rates a little too low, and let the gap quietly erode the real value of the debt. Economists have a polite name for this. They call it financial repression.

If an arbitrary target really is back on the table, it is at least worth asking which direction a government drowning in interest payments would quietly prefer it to move.

In fairness, this is a lens, not a verdict, and the other side deserves its hearing. There is a serious case for the 2%. A little inflation greases the labor market as Yellen argued for, letting real wages drift down without the bruising fight of cutting paychecks, and it keeps a safe distance from the deflationary trap that a zero target invites. Plenty of thoughtful people argue central banks prize flexibility for reasons that have nothing to do with debt.

We simply find it an interesting and underappreciated way to read the moment, one that happens to matter a great deal if you turn out to be the saver on the other side of the trade. Treat it as a question worth sitting with.

Remember war bonds? The generation that lived through the war certainly does

Remember Brash’s uncle, the one whose retirement bonds got vaporized? He had company, decades earlier and an ocean away as seen in war bonds.

If “captive demand for government debt” sounds abstract, it once had a friendlier face and a patriotic poster campaign. During the Second World War, more than 85 million Americans, over half the population, bought war bonds, lending the government some $185 billion at an implied return of under 3%. A Series E bond cost $18.75 and promised $25 a decade later. It was framed as a duty, and it was one: the bonds helped win the war. But it was also the purest financial repression ever run at scale.

Here is the part the posters left out. The Federal Reserve deliberately capped bond yields near 2.5% from 1942 until the 1951 Treasury-Fed Accord, which is why the bonds could pay so little in the first place. Savers were locked into a fixed yield of under 3%, and with that ceiling in place they had no way to roll into anything higher.

Then, once wartime price controls were lifted, post-war inflation ran into the teens. The saver who answered the call was repaid every promised dollar, but in money that bought meaningfully less than the sum first lent. Over the bond’s ten-year life, a nominal gain of a third was more than erased by inflation, leaving a real loss.

They funded the state at a loss and called it patriotism.

War bonds ads in the New York city subway back in the 1940s

War bonds ads in the New York city subway back in the 1940s

Source: New York Transit Museum.

The Poster Just Changed Fonts

The difference today is one of marketing, not mechanism. Nobody is printing technicolor posters of Uncle Sam asking you to do your duty. Instead the captivity is engineered through plumbing.

Basel rules, the global rulebook that sets how much capital banks must hold, nudge banks to hold government bonds as “safe” assets. Pension and insurance mandates force institutions to park trillions in sovereign debt regardless of yield. Someone’s retirement fund is a war-bond buyer who never saw a poster and never got asked.

The mechanism is identical to 1942: a captive pool of demand for government debt, held at yields that conveniently sit below the rate at which money loses value. The saver still pays. They just don’t get a lapel pin for it. Which is also why we wrote “Invisible Inflation”: if the yardstick that defines “2%” is itself flexible, the repression runs deeper than the headline ever admits.

Know Which Side of the Ledger You’re On

Which brings us back to that television studio in 1988. The lesson isn’t that central bankers are villains. Roger Douglas and Don Brash were trying to tame a genuinely vicious inflation, and the experiment worked. The lesson is humbler and more useful: the rules that govern your savings are not laws of physics handed down from a mountain.

They are human choices, sometimes improvised on live TV, always serving someone’s balance sheet. New Zealand’s gift to the world was visibility about the number. The unsettling thing about this week is a Fed that has stopped telling you what it is thinking, at the exact moment the math gives it every reason to wish for a little more inflation than it would ever admit out loud.

You don’t get a vote in that redistribution. But you do get a choice about what you own. That is the whole reason we keep coming back to real assets: things that can’t be printed, pegged, or talked down on a television interview. Brash’s uncle and the war-bond savers answered the call and were repaid in shrunken dollars. They didn’t have the playbook. You do. The poster has changed fonts, but it is still asking you for the same thing. The only question is whether you read the fine print this time.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share

Have you ever wondered how the 2% inflation target got to 2%?

Picture a television studio in New Zealand, 1988. Big hair, boxy suits, the works. The country has spent two decades getting mugged by inflation, which tore through the 1970s and early 1980s and refused to fully sit down even after a painful round of reforms.

The finance minister, Roger Douglas, is on air trying to convince a skeptical public that the central bank will not quietly tolerate rising prices forever. Pressed on what he is actually aiming for, he says he’d like to see inflation somewhere around zero to one percent.

There was no model behind the number, no white paper, no committee. It was the central-banking equivalent of being asked your goal weight and answering, “I dunno, abs?”

Don Brash, the kiwifruit farmer turned central banker who had just taken over the Reserve Bank of New Zealand, later put it plainly: “It was almost a chance remark. The figure was plucked out of the air to influence the public’s expectations.”

1988 comic ridiculing the Reserve Bank of New Zealand’s inflation prediction

Source: Malcolm Walker, Reserve Bank of New Zealand

Brash, as it happens, had personal reasons to loathe inflation. He liked to tell the story of an uncle who sold his apple orchard in 1971, parked the proceeds in long-term government bonds to fund his retirement, and then watched inflation incinerate 90 percent of his life savings by the time those bonds matured. Keep that uncle in mind.

The Reserve Bank Act of 1989 turned the chance remark into a job description. It ordered the finance minister and the central bank to agree on a formal inflation target, handed the bank independence to chase it, and made the goal enforceable by allowing the governor to be fired for missing.

Brash and the finance minister of the day, David Caygill, took Douglas’s zero-to-one, widened it a touch for breathing room, and settled on a band of zero to 2 percent. The law passed in a quick, near-unanimous vote by parliamentarians keen to get home for Christmas.

Here is the punchline: it worked. Inflation was 7.6 percent when the law passed in 1989. By the end of 1991 it was 2 percent. Simply by announcing a number and meaning it, New Zealand talked wages and prices into behaving.

Brash evangelized to fellow central bankers at Jackson Hole, and the converts piled in: Canada in 1991, then Sweden, then Britain. Today roughly 45 countries plus the Euro Area run on an inflation target, and 2 percent has become, in the New York Times’s lovely phrase, “virtually an economic religion.”

The religion, live on air. First thing that appeared on our Bloomberg TV

We mention all this not to dunk on New Zealand, which also gave us excellent lamb and the cinematic “Lord of the Rings”, but because a figure plucked from the air on a Wellington TV set now governs the value of your savings. When a target is arbitrary, it is also negotiable. And the people most exposed to that negotiation are savers.

New Zealand started it first and others began to follow suit

Sources: NYT; World Bank

The Federal Reserve was a late and reluctant convert. Behind the oversized doors of its boardroom in 1995 and 1996, officials argued about whether to copy the Kiwis at all, and if so, what the number should be. Heavyweights like Paul Volcker and Alan Greenspan leaned toward zero, on the logic that a dollar today should buy roughly what a dollar buys in twenty years.

The governor who argued hardest for a positive target of around 2 percent was a woman named Janet Yellen. Her case was the grease-the-wheels argument: a little inflation lets employers quietly trim real wages without the misery of cutting nominal pay, and, crucially, it lets real interest rates go negative when a recession demands it.

“A little inflation permits real interest rates to become negative on the rare occasions when required to counter a recession,” she told the room in 1996. “This could be important.” She had no idea how important.

Yellen won. The Fed privately settled on 2 percent in 1996 and only said so out loud in 2012. And yes, this is the same Janet Yellen from our “Welcome to the Banana Republic,” piece, the one who later ran the Treasury and issued the mountain of debt now straining against that very target.

A Hawk Walks In, and Says Almost Nothing

Which brings us to this week. On June 17, the Federal Reserve held its benchmark rate at 3.5% to 3.75%, the first meeting chaired by Kevin Warsh. No cut. The committee dropped its earlier forecast of a cut this year.

The appointment of a new chairman does matter here as each person leading carries different philosophies which can impact how the Fed will move forward. Kevin Warsh sat on the Fed’s Board of Governors from 2006 to 2011, through the heart of the financial crisis, then spent the years since as one of the institution’s sharpest critics. He argued the Fed had grown too talkative, too wedded to its models, and too comfortable with easy money. That is the tell.

Where Janet Yellen built the machinery of an explicit target, and Jerome Powell leaned into ever more detailed forward guidance, Warsh seems to want the opposite: fewer promises and more discretion. His appointment matters because it hands the keys of the post-2008 transparency project to a man who never quite believed in it.

The median official now pencils in a fed funds rate of 3.8 percent by December, which is to say a hike, with PCE inflation projected at 3.6 percent for the year, nearly double the target. The policy statement was stripped to what Warsh called “a bit shorter, a bit simpler,” and shorn of the “so-called forward guidance” he judged “not well-suited to the current policy conjuncture.”

Source: Fortune

But the real news was what Warsh would not say. While he encouraged his colleagues to keep submitting their forecasts to the famous dot plot, he refused to submit his own. “I have refrained from offering any projections of my own,” he announced, “consistent with my long-held views on the SEP.”

No dot, no roadmap, no breadcrumbs. This is a genuine break. For more than a decade the Fed has practically narrated its own intentions in advance; Warsh prefers what he admires about the Greenspan era, the deliberate fog, the man-behind-the-curtain mystique.

And tucked into the same meeting was the part that should make every saver sit up. Among five new task forces Warsh announced was one charged with re-examining the Fed’s “inflation frameworks” from “first principles,” weighing “the full range of ideas for delivering price stability.”

Why would a central bank want to be less clear about its target just as that target turns inconvenient? Maybe it is humility. Or maybe it has nothing to do with inflation, and everything to do with the size of the bill.

To be clear, none of this means the Fed has decided to raise its inflation target; reviewing a framework is not the same as loosening one, and a review could just as easily change nothing. But history is fairly blunt about the pattern: heavily indebted governments tend, sooner or later, to find reasons to tolerate a little more inflation than they once promised.

The Trillion-Dollar Tenant Nobody Voted For

Here is the number that should be keeping policymakers up at night. The US government is on track to spend roughly $1 trillion on interest payments this fiscal year. That is more than the entire defense budget, which runs around $947 billion, and net interest already overtook defense spending in the first quarter.

Put another way: for every dollar Washington collects in taxes, about 19 cents now goes straight to bondholders before a single road is paved or fighter jet is fueled. Interest costs are running near 3.2% of GDP, eclipsing a record set back in 1991.

The chart below covers only the first eight months of this fiscal year, and even on that partial tally net interest ($742 billion) has already overtaken the military ($600 billion); annualized, it crosses $1 trillion.

Source: Congressional Budget Office

The cruel mechanics are simple: the higher the Fed keeps rates to fight inflation, the more expensive that trillion-dollar tenant becomes. A government this indebted cannot actually afford honestly high interest rates for long. Something has to give, and “raise taxes” and “cut spending” are about as popular as a durian in a crowded elevator. So what’s left?

The option nobody campaigns on: let inflation run a little hot, keep rates a little too low, and let the gap quietly erode the real value of the debt. Economists have a polite name for this. They call it financial repression.

If an arbitrary target really is back on the table, it is at least worth asking which direction a government drowning in interest payments would quietly prefer it to move.

In fairness, this is a lens, not a verdict, and the other side deserves its hearing. There is a serious case for the 2%. A little inflation greases the labor market as Yellen argued for, letting real wages drift down without the bruising fight of cutting paychecks, and it keeps a safe distance from the deflationary trap that a zero target invites. Plenty of thoughtful people argue central banks prize flexibility for reasons that have nothing to do with debt.

We simply find it an interesting and underappreciated way to read the moment, one that happens to matter a great deal if you turn out to be the saver on the other side of the trade. Treat it as a question worth sitting with.

Remember war bonds? The generation that lived through the war certainly does

Remember Brash’s uncle, the one whose retirement bonds got vaporized? He had company, decades earlier and an ocean away as seen in war bonds.

If “captive demand for government debt” sounds abstract, it once had a friendlier face and a patriotic poster campaign. During the Second World War, more than 85 million Americans, over half the population, bought war bonds, lending the government some $185 billion at an implied return of under 3%. A Series E bond cost $18.75 and promised $25 a decade later. It was framed as a duty, and it was one: the bonds helped win the war. But it was also the purest financial repression ever run at scale.

Here is the part the posters left out. The Federal Reserve deliberately capped bond yields near 2.5% from 1942 until the 1951 Treasury-Fed Accord, which is why the bonds could pay so little in the first place. Savers were locked into a fixed yield of under 3%, and with that ceiling in place they had no way to roll into anything higher.

Then, once wartime price controls were lifted, post-war inflation ran into the teens. The saver who answered the call was repaid every promised dollar, but in money that bought meaningfully less than the sum first lent. Over the bond’s ten-year life, a nominal gain of a third was more than erased by inflation, leaving a real loss.

They funded the state at a loss and called it patriotism.

War bonds ads in the New York city subway back in the 1940s

Source: New York Transit Museum.

The Poster Just Changed Fonts

The difference today is one of marketing, not mechanism. Nobody is printing technicolor posters of Uncle Sam asking you to do your duty. Instead the captivity is engineered through plumbing.

Basel rules, the global rulebook that sets how much capital banks must hold, nudge banks to hold government bonds as “safe” assets. Pension and insurance mandates force institutions to park trillions in sovereign debt regardless of yield. Someone’s retirement fund is a war-bond buyer who never saw a poster and never got asked.

The mechanism is identical to 1942: a captive pool of demand for government debt, held at yields that conveniently sit below the rate at which money loses value. The saver still pays. They just don’t get a lapel pin for it. Which is also why we wrote “Invisible Inflation”: if the yardstick that defines “2%” is itself flexible, the repression runs deeper than the headline ever admits.

Know Which Side of the Ledger You’re On

Which brings us back to that television studio in 1988. The lesson isn’t that central bankers are villains. Roger Douglas and Don Brash were trying to tame a genuinely vicious inflation, and the experiment worked. The lesson is humbler and more useful: the rules that govern your savings are not laws of physics handed down from a mountain.

They are human choices, sometimes improvised on live TV, always serving someone’s balance sheet. New Zealand’s gift to the world was visibility about the number. The unsettling thing about this week is a Fed that has stopped telling you what it is thinking, at the exact moment the math gives it every reason to wish for a little more inflation than it would ever admit out loud.

You don’t get a vote in that redistribution. But you do get a choice about what you own. That is the whole reason we keep coming back to real assets: things that can’t be printed, pegged, or talked down on a television interview. Brash’s uncle and the war-bond savers answered the call and were repaid in shrunken dollars. They didn’t have the playbook. You do. The poster has changed fonts, but it is still asking you for the same thing. The only question is whether you read the fine print this time.

Tara Mulia

For more blogs like these, subscribe to our newsletter here!

Admin heyokha

Share